- United States

- /

- Consumer Durables

- /

- NYSE:ETD

Ethan Allen Interiors Inc. Recorded A 13% Miss On Revenue: Analysts Are Revisiting Their Models

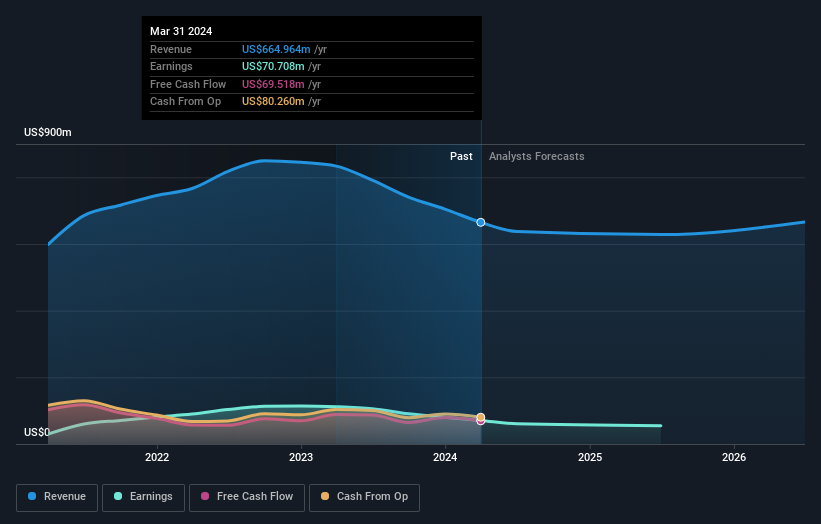

Ethan Allen Interiors Inc. (NYSE:ETD) shareholders are probably feeling a little disappointed, since its shares fell 7.0% to US$29.06 in the week after its latest quarterly results. Revenues were US$146m, 13% below analyst expectations, although losses didn't appear to worsen significantly, with a statutory per-share loss of US$4.13 being in line with what the analysts anticipated. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for Ethan Allen Interiors

After the latest results, the consensus from Ethan Allen Interiors' dual analysts is for revenues of US$628.2m in 2025, which would reflect a noticeable 5.5% decline in revenue compared to the last year of performance. Statutory earnings per share are expected to tumble 21% to US$2.20 in the same period. In the lead-up to this report, the analysts had been modelling revenues of US$691.0m and earnings per share (EPS) of US$3.00 in 2025. The analysts seem less optimistic after the recent results, reducing their revenue forecasts and making a pretty serious reduction to earnings per share numbers.

It'll come as no surprise then, to learn that the analysts have cut their price target 9.1% to US$30.00.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Ethan Allen Interiors' past performance and to peers in the same industry. We would highlight that revenue is expected to reverse, with a forecast 4.5% annualised decline to the end of 2025. That is a notable change from historical growth of 2.6% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.1% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Ethan Allen Interiors is expected to lag the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Ethan Allen Interiors. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2026, which can be seen for free on our platform here.

Plus, you should also learn about the 2 warning signs we've spotted with Ethan Allen Interiors (including 1 which can't be ignored) .

Valuation is complex, but we're here to simplify it.

Discover if Ethan Allen Interiors might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ETD

Ethan Allen Interiors

Operates as an interior design company, and manufacturer and retailer of home furnishings in the United States and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives