Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqCM:VUZI

Bearish: Analysts Just Cut Their Vuzix Corporation (NASDAQ:VUZI) Revenue and EPS estimates

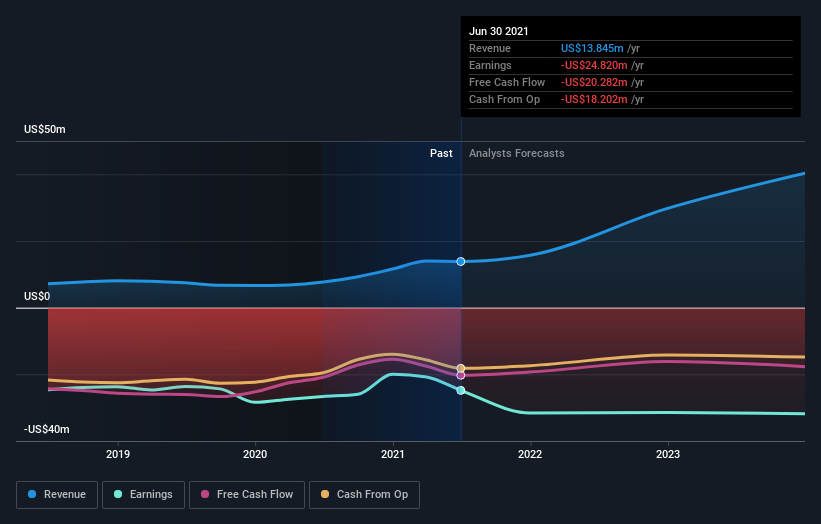

The latest analyst coverage could presage a bad day for Vuzix Corporation (NASDAQ:VUZI), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) estimates were cut sharply as analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

After this downgrade, Vuzix's three analysts are now forecasting revenues of US$16m in 2021. This would be a notable 14% improvement in sales compared to the last 12 months. Per-share losses are expected to creep up to US$0.51. However, before this estimates update, the consensus had been expecting revenues of US$22m and US$0.39 per share in losses. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

See our latest analysis for Vuzix

The consensus price target fell 8.3% to US$27.50, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Vuzix analyst has a price target of US$30.00 per share, while the most pessimistic values it at US$25.00. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Vuzix is an easy business to forecast or the underlying assumptions are obvious.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. The period to the end of 2021 brings more of the same, according to the analysts, with revenue forecast to display 29% growth on an annualised basis. That is in line with its 29% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 9.2% per year. So although Vuzix is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that analysts increased their loss per share estimates for this year. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. With a serious cut to this year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of Vuzix.

There might be good reason for analyst bearishness towards Vuzix, like major dilution from new stock issuance in the past year. For more information, you can click here to discover this and the 2 other warning signs we've identified.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade Vuzix, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:VUZI

Vuzix

Designs, manufactures, and markets artificial intelligence (AI)-powered smart glasses, waveguides, and augmented reality (AR) technologies in North America, Europe, the Asia Pacific, and internationally.

Flawless balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor