Advertisement

- United States

- /

- Consumer Durables

- /

- NasdaqGS:SONO

There's Been No Shortage Of Growth Recently For Sonos' (NASDAQ:SONO) Returns On Capital

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. With that in mind, we've noticed some promising trends at Sonos (NASDAQ:SONO) so let's look a bit deeper.

Return On Capital Employed (ROCE): What is it?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Sonos is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

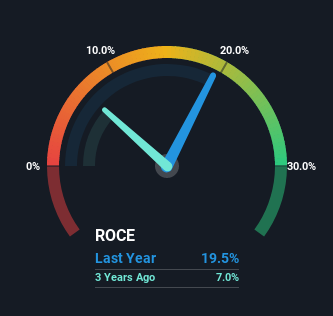

0.19 = US$149m ÷ (US$1.2b - US$464m) (Based on the trailing twelve months to April 2022).

So, Sonos has an ROCE of 19%. On its own, that's a standard return, however it's much better than the 16% generated by the Consumer Durables industry.

See our latest analysis for Sonos

Above you can see how the current ROCE for Sonos compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

The Trend Of ROCE

The fact that Sonos is now generating some pre-tax profits from its prior investments is very encouraging. The company was generating losses five years ago, but now it's earning 19% which is a sight for sore eyes. In addition to that, Sonos is employing 401% more capital than previously which is expected of a company that's trying to break into profitability. We like this trend, because it tells us the company has profitable reinvestment opportunities available to it, and if it continues going forward that can lead to a multi-bagger performance.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 38%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. This tells us that Sonos has grown its returns without a reliance on increasing their current liabilities, which we're very happy with.

The Key Takeaway

Long story short, we're delighted to see that Sonos' reinvestment activities have paid off and the company is now profitable. Since the stock has returned a staggering 118% to shareholders over the last three years, it looks like investors are recognizing these changes. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

Like most companies, Sonos does come with some risks, and we've found 2 warning signs that you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SONO

Sonos

Designs, develops, manufactures, and sells audio products and services in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor