Advertisement

- United States

- /

- Leisure

- /

- NasdaqGS:PTON

Is Peloton Interactive (PTON) Pricing Reflect A Potential Opportunity After Prolonged Share Price Declines

Reviewed by Bailey Pemberton

- If you are wondering whether Peloton Interactive at around US$3.84 is a bargain or a value trap, starting with a clear look at what the current share price actually reflects can help sharpen your view.

- The stock has recently returned 3.5% over 7 days, while the 30 day, year to date and 1 year returns sit at an 11.1% decline, 37.3% decline and 44.8% decline respectively, so recent moves may say as much about changing risk perception as they do about the underlying business.

- Recent headlines around Peloton have continued to focus on the company’s transition from hyper growth expectations to a more mature fitness platform and hardware business, and on how the brand fits into a competitive at home and gym based fitness market. Together, this context helps frame whether the current share price reflects lingering caution or an attempt to re rate the stock.

- Peloton’s valuation score stands at 5/6, which suggests most of our checks point to the shares screening as undervalued, and the rest of this article will compare different valuation approaches before circling back to an even richer way to think about what the market might be pricing in.

Find out why Peloton Interactive's -44.8% return over the last year is lagging behind its peers.

Approach 1: Peloton Interactive Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company could be worth today by projecting its future cash flows and discounting them back to a present value using a required rate of return.

For Peloton Interactive, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow sits at about $336.5 million, and analysts provide explicit projections out to 2030, with Simply Wall St extrapolating further years. By 2035, projected free cash flow is $485.1 million, with each year between 2026 and 2035 contributing an estimated discounted value to the total equity valuation.

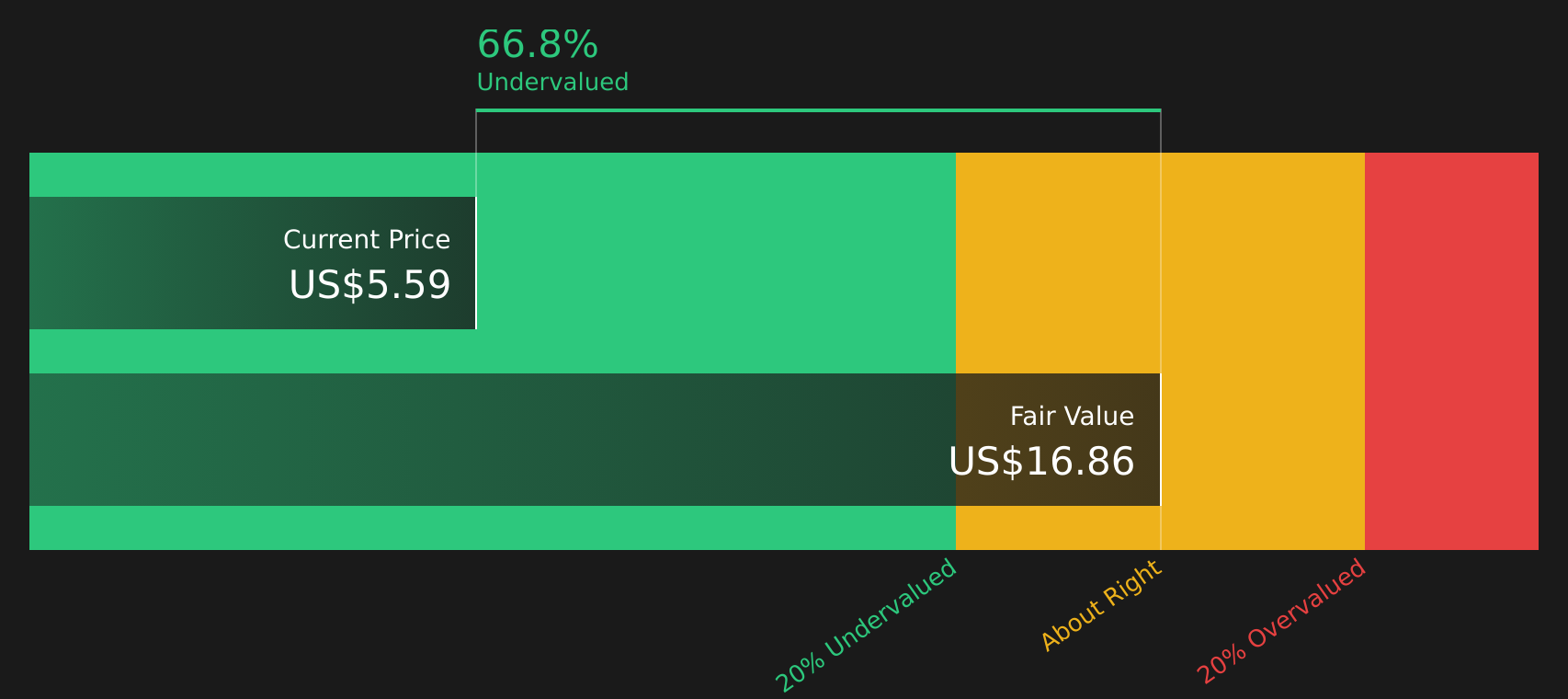

Aggregating those discounted projections results in an estimated intrinsic value of US$14.77 per share. Compared with the recent share price of about US$3.84, the DCF output implies the shares trade at a 74.0% discount to this intrinsic estimate, which screens as materially undervalued on this metric.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Peloton Interactive is undervalued by 74.0%. Track this in your watchlist or portfolio, or discover 52 more high quality undervalued stocks.

Approach 2: Peloton Interactive Price vs Sales

For companies where earnings are limited or volatile, the P/S ratio is often a useful way to gauge what the market is paying for each dollar of revenue. It sidesteps short term swings in profit and focuses on the top line, which can be more stable for businesses still working toward consistent profitability.

Growth expectations and perceived risk still matter, because investors usually accept a higher P/S ratio when they expect stronger revenue growth or see less risk, and look for a lower multiple when the outlook is more uncertain. Peloton Interactive currently trades on a P/S of 0.67x, compared with the Leisure industry average of 0.94x and a peer average of 1.05x.

Simply Wall St’s Fair Ratio for Peloton Interactive stands at 0.91x. This proprietary metric estimates the P/S multiple that could be reasonable, given factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it blends these inputs, it can give a more tailored reference point than a simple peer or industry comparison. With the current 0.67x P/S sitting below the 0.91x Fair Ratio by more than 0.10x, the shares appear undervalued on this measure.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Peloton Interactive Narrative

Earlier it was mentioned that there is an even better way to understand valuation, and on Simply Wall St this takes the form of Narratives, which let you attach a clear story about Peloton Interactive to the numbers behind your own fair value, revenue, earnings and margin assumptions.

A Narrative is your view of how the business could play out, linked directly to a forecast and a fair value. Instead of only looking at ratios in isolation, you see how a company story, a set of financial estimates and a valuation all line up.

On the Simply Wall St Community page, Narratives are presented as an easy tool that many investors already use. They help you compare your assumed fair value with the current share price to decide whether Peloton looks closer to a buy, a hold or a sell for your personal framework, without needing to build a spreadsheet from scratch.

Because Narratives update when new information such as earnings, guidance or news is added, you can quickly see how a cautious view that ties to a US$5.00 fair value and a more optimistic view that ties to a US$16.64 fair value interpret the same Peloton data very differently. You can then choose which story fits your own expectations best.

Do you think there's more to the story for Peloton Interactive? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PTON

Peloton Interactive

Provides fitness and wellness products and services in North America and internationally.

Reasonable growth potential with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7065.0% undervalued

42 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.2% undervalued

46 followersusers have followed this narrative

8 commentsusers have commented on this narrative

16 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0541.3% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.0% undervalued

91 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on Macbee Planet ·

Approaching an inflection point

Fair Value:JP¥1.08k7.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

XX

xxlfm on NVIDIA ·

Are you worrying about Michael Burry’s Short?!

Fair Value:CA$532.5991.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LY

Lyra on Giftify ·

What is Giftify (GIFT) Really Worth? An Honest Risk-Discount Valuation

Fair Value:US$0.653.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.4% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.5% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1931.2% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative