Advertisement

- United States

- /

- Leisure

- /

- NasdaqGS:PTON

A Look At Peloton Interactive (PTON) Valuation After Workforce Cuts And Cost Saving Plans

Peloton Interactive (PTON) has announced an 11% workforce reduction, concentrated in engineering roles, just ahead of its upcoming quarterly earnings. This move signals management’s focus on cost savings and operational changes as financial pressures persist.

See our latest analysis for Peloton Interactive.

At a share price of US$5.76, Peloton’s 90 day share price return of an 18.53% decline and 1 year total shareholder return of a 21.31% loss suggest sentiment has weakened over time, even with a recent 3.04% 1 day share price gain around the latest cost cutting news and upcoming earnings update.

If Peloton’s reset has you reassessing opportunities in connected fitness and digital platforms, it could be a good time to look across high growth tech and AI stocks for other possibilities in this space.

With Peloton now trading at a steep discount to its analyst price target and still working through a tough reset, you have to ask: Is the downside already reflected in the share price, or is the market skeptical about future growth?

Most Popular Narrative: 44.8% Undervalued

With Peloton Interactive’s fair value narrative sitting at $10.43 against the last close of $5.76, the story hinges on whether execution can close that gap.

Ongoing operational improvements, including cost reduction efforts, optimizing indirect spend, and a strategic shift toward higher margin, asset light models, are expected to drive continued gross and net margin expansion, as reflected in recent and forecasted improvements in adjusted EBITDA and free cash flow.

Want to see what kind of revenue mix, margin profile, and earnings ramp are built into that valuation gap? The core assumptions tie steady top line expectations to a sharp profitability swing and a premium future earnings multiple. Curious how those pieces fit together into a $10 plus fair value when today’s price is almost half that level?

Result: Fair Value of $10.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that fair value gap still depends on Peloton reversing subscription declines and managing higher churn while also holding the line on ongoing cost and margin pressures.

Find out about the key risks to this Peloton Interactive narrative.

Another View On Peloton’s Price

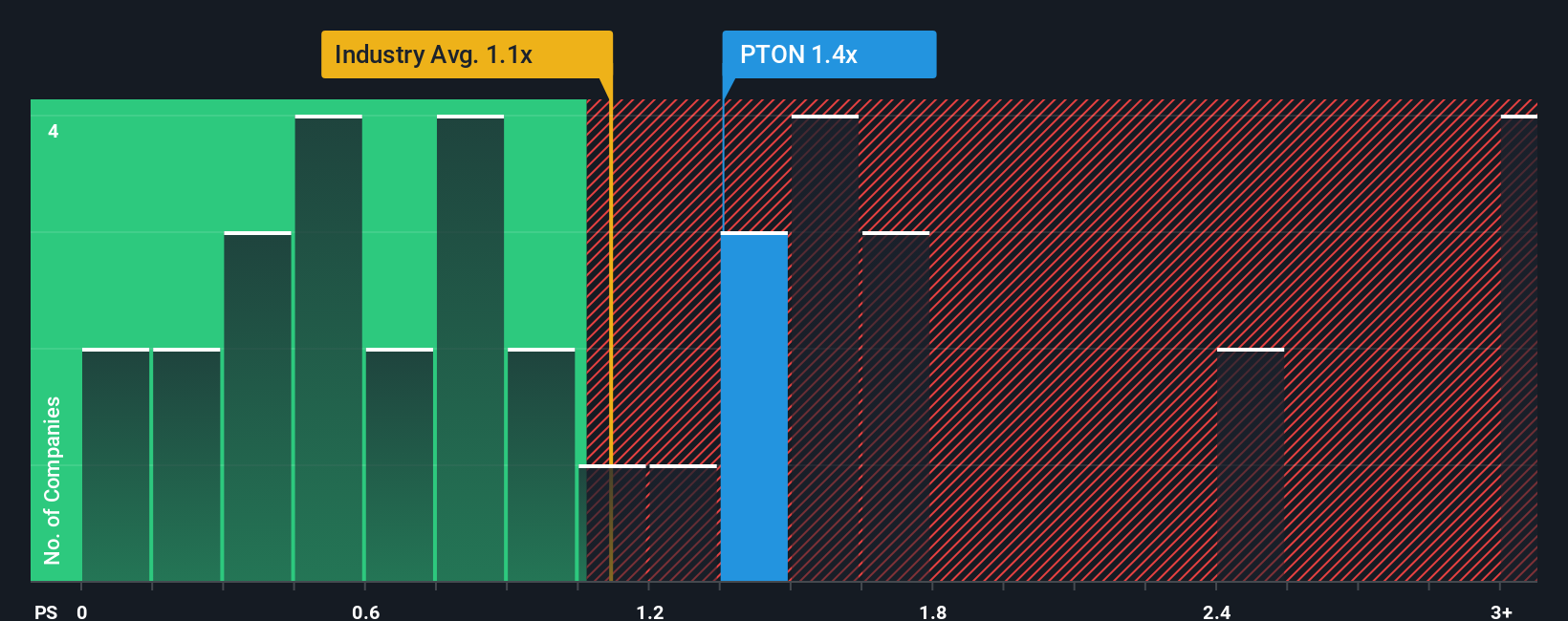

So far, the story leans on fair value estimates that suggest Peloton is undervalued, with our model pointing to a discount of about 69.5% versus fair value and a future P/E assumption above the current industry level. That can look appealing, but it also raises a question about how much optimism is built into those assumptions.

While Peloton screens as good value on its current P/S of 1x against both peers at 1x and a fair ratio of 1x, there is not a clear margin of safety on this simple yardstick. If the story relies mainly on growth and margin improvement, how comfortable are you with paying in line with the sector while waiting for the thesis to play out?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Peloton Interactive Narrative

If this framework does not match how you see Peloton, or you would rather dig through the numbers yourself, you can build a custom thesis in just a few minutes with Do it your way.

A great starting point for your Peloton Interactive research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Do not stop your research with a single stock. You can quickly widen your watchlist using focused screens that highlight different types of opportunities across the market.

- Spot potential turnaround opportunities by scanning these 874 undervalued stocks based on cash flows that appear cheaply priced relative to their underlying cash flows.

- Follow powerful tech themes by checking out these 24 AI penny stocks that are building their business around artificial intelligence.

- Strengthen your income watchlist by reviewing these 13 dividend stocks with yields > 3% that offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PTON

Peloton Interactive

Provides fitness and wellness products and services in North America and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.675.4% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.2538.0% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2690.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3410.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DI

DinTang on Bumitama Agri ·

Expectations focused on stable output, disciplined costs, and continued cash returns to shareholders

Fair Value:S$2.4622.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$5809.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

Martimmfonseca on Meta Platforms ·

Meta Could Reach $653–$792 Over the Next Five Years

Fair Value:US$6532.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3952.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

38 followersusers have followed this narrative

11 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3134.6% undervalued

1355 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

MS

msd on Life Insurance Corporation of India ·

HOwmuch ever attractive , no one buying LIC shares, dont know why.

0

|0