Advertisement

- United States

- /

- Luxury

- /

- NasdaqGS:LULU

Is Slowing Comp Sales and Tariff Risks Shifting the Growth Narrative for Lululemon (LULU)?

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, Lululemon Athletica has drawn mixed analyst sentiment after reporting fiscal Q2 2025 results with 7% revenue growth and modest comparable sales gains, all against a backdrop of heightened competition and operational pressures.

- This news also coincided with a Federal Reserve interest rate cut, raising questions about how easing monetary policy, along with ongoing tariff and global growth issues, could impact the retailer's outlook.

- We'll explore how concerns about Lululemon's international growth and tariff headwinds now influence its overall investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

lululemon athletica Investment Narrative Recap

To be a shareholder in Lululemon Athletica right now, you need to believe that the company’s product reset, innovation, and long-term international strategy can offset headwinds from tariffs and tough US sales trends. The most important short-term catalyst remains the rollout of new product lines and higher international growth, while the biggest risk continues to be margin pressure from increased tariffs. Recent news around modest sales growth and competition reinforces these pressures, but does not materially change the central questions investors must consider.

The company’s September 2025 update to its full-year guidance specifically addressed tariff impacts, with Lululemon now expecting a US$240 million reduction in gross profit due to higher import costs. This directly connects to the foremost risk facing the company: the effect of tariffs on margins and growth prospects. In this context, the product reset and international expansion become even more critical as potential offsets to these financial challenges.

Yet, against this backdrop, investors should pay close attention to how ongoing tariff changes might affect future earnings, as...

Read the full narrative on lululemon athletica (it's free!)

lululemon athletica's narrative projects $12.8 billion revenue and $1.9 billion earnings by 2028. This requires 5.4% yearly revenue growth and a $0.1 billion earnings increase from $1.8 billion today.

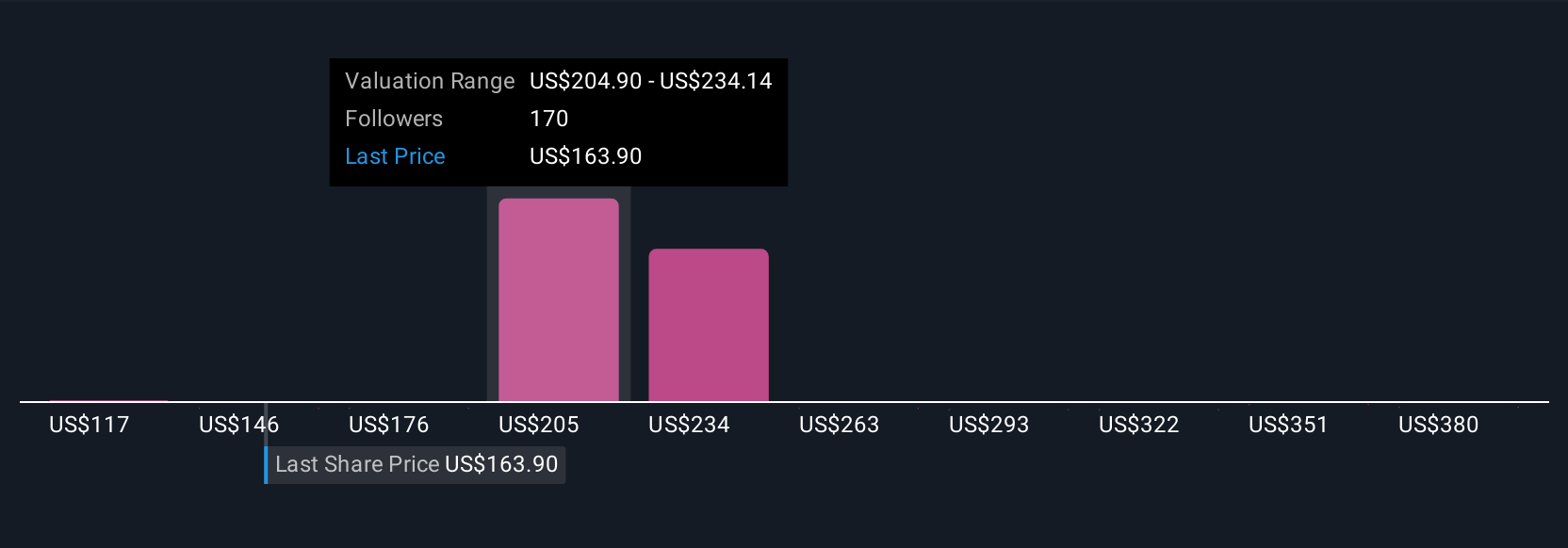

Uncover how lululemon athletica's forecasts yield a $198.36 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Across 56 Simply Wall St Community estimates, fair value targets for Lululemon swing from US$117 to US$410 per share. As margin pressure from higher tariffs weighs on recent results, consider how much these community views anticipate future earnings resilience.

Explore 56 other fair value estimates on lululemon athletica - why the stock might be worth 33% less than the current price!

Build Your Own lululemon athletica Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your lululemon athletica research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if lululemon athletica might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LULU

lululemon athletica

Designs, distributes, and retails technical athletic apparel, footwear, and accessories for women and men under the lululemon brand in the United States, Canada, Mexico, China Mainland, Hong Kong, Taiwan, Macau, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor