Advertisement

- United States

- /

- Luxury

- /

- NasdaqGM:LAKE

Lakeland Industries, Inc. Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Predictions

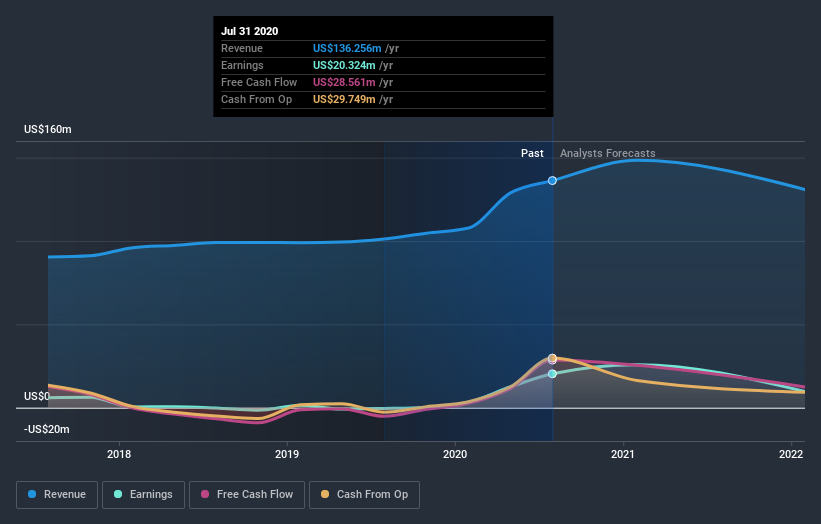

Lakeland Industries, Inc. (NASDAQ:LAKE) just released its quarterly report and things are looking bullish. It was a solid earnings report, with revenues and statutory earnings per share (EPS) both coming in strong. Revenues were 15% higher than the analysts had forecast, at US$35m, while EPS were US$1.16 beating analyst models by 274%. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Lakeland Industries after the latest results.

View our latest analysis for Lakeland Industries

Following the latest results, Lakeland Industries' dual analysts are now forecasting revenues of US$148.4m in 2021. This would be a decent 8.9% improvement in sales compared to the last 12 months. Per-share earnings are expected to shoot up 26% to US$3.20. Before this earnings report, the analysts had been forecasting revenues of US$149.1m and earnings per share (EPS) of US$2.02 in 2021. Although the revenue estimates have not really changed, we can see there's been a great increase in earnings per share expectations, suggesting that the analysts have become more bullish after the latest result.

There's been no major changes to the consensus price target of US$27.50, suggesting that the improved earnings per share outlook is not enough to have a long-term positive impact on the stock's valuation.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's clear from the latest estimates that Lakeland Industries' rate of growth is expected to accelerate meaningfully, with the forecast 8.9% revenue growth noticeably faster than its historical growth of 4.8%p.a. over the past five years. Other similar companies in the industry (with analyst coverage) are also forecast to grow their revenue at 9.7% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Lakeland Industries is expected to grow at about the same rate as the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Lakeland Industries following these results. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have analyst estimates for Lakeland Industries going out as far as 2022, and you can see them free on our platform here.

Plus, you should also learn about the 3 warning signs we've spotted with Lakeland Industries (including 1 which is concerning) .

If you’re looking to trade Lakeland Industries, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGM:LAKE

Lakeland Industries

Manufactures and sells industrial protective clothing and accessories for the industrial and public protective clothing market worldwide.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor