- United States

- /

- Professional Services

- /

- NYSE:WNS

WNS (Holdings) (NYSE:WNS) Leverages AI and Analytics for Growth Despite Revenue Challenges

Reviewed by Simply Wall St

WNS (Holdings) (NYSE:WNS) showcases resilience through strategic investments and a favorable valuation, with a Price-To-Earnings Ratio of 19.4x and an impressive earnings growth forecast of 16.7% per year. Despite a recent 4.4% revenue drop due to the loss of a major healthcare client, WNS is actively pursuing over 20 large deals and expanding its focus on AI and digital transformation. The company report will explore these strategic initiatives, financial challenges, and potential growth opportunities.

Click here to discover the nuances of WNS (Holdings) with our detailed analytical report.

Innovative Factors Supporting WNS (Holdings)

WNS demonstrates resilience through its strategic investments and performance metrics. The company's Price-To-Earnings Ratio of 19.4x, which is lower than both the industry average of 25.6x and the peer average of 21.8x, indicates a favorable valuation. This is further supported by its earnings growth forecast of 16.7% per year, surpassing the US market average of 15.4%. Keshav Murugesh, CEO, highlighted that WNS added 9 new logos and expanded 41 existing relationships, reflecting strong client trust. Additionally, the company's strategic focus on analytics and AI has positioned it as a leader in these domains, as recognized by industry analysts.

Challenges Constraining WNS (Holdings)'s Potential

WNS faces some hurdles. The company reported a 4.4% year-over-year revenue decrease to $310.7 million, driven by the loss of a major healthcare client and reduced online travel revenues. This highlights areas of vulnerability. Arijit Sengupta, CFO, noted a decrease in adjusted operating margins to 18.6% from 21.5% last year, attributed to increased investments and higher SG&A levels. Furthermore, WNS's revenue growth forecast of 5.8% per year is below the US market's 8.9%, suggesting potential challenges in matching broader industry growth rates.

Areas for Expansion and Innovation for WNS (Holdings)

Opportunities abound for WNS, particularly in expanding its large deal pipeline. The company is pursuing over 20 large deals, representing more than $500 million in annual contract value across various verticals and geographies. This could significantly boost future growth. The focus on AI and digital transformation is another promising avenue, with expectations to derive 5% of revenue from Gen AI initiatives this year. These strategic investments in proprietary technology tools and platforms are likely to enhance WNS's market position and capitalize on emerging opportunities.

External Factors Threatening WNS (Holdings)

However, external challenges persist. The timing of large deal signings remains unpredictable, potentially affecting revenue projections and growth expectations. Keshav Murugesh has acknowledged this uncertainty, which could impact investor confidence. Additionally, the ongoing reduction in online travel volumes continues to pose a risk to revenue stability and diversification efforts. Economic fluctuations and market condition changes further compound these threats, potentially impacting WNS's performance and growth prospects in the longer term.

Conclusion

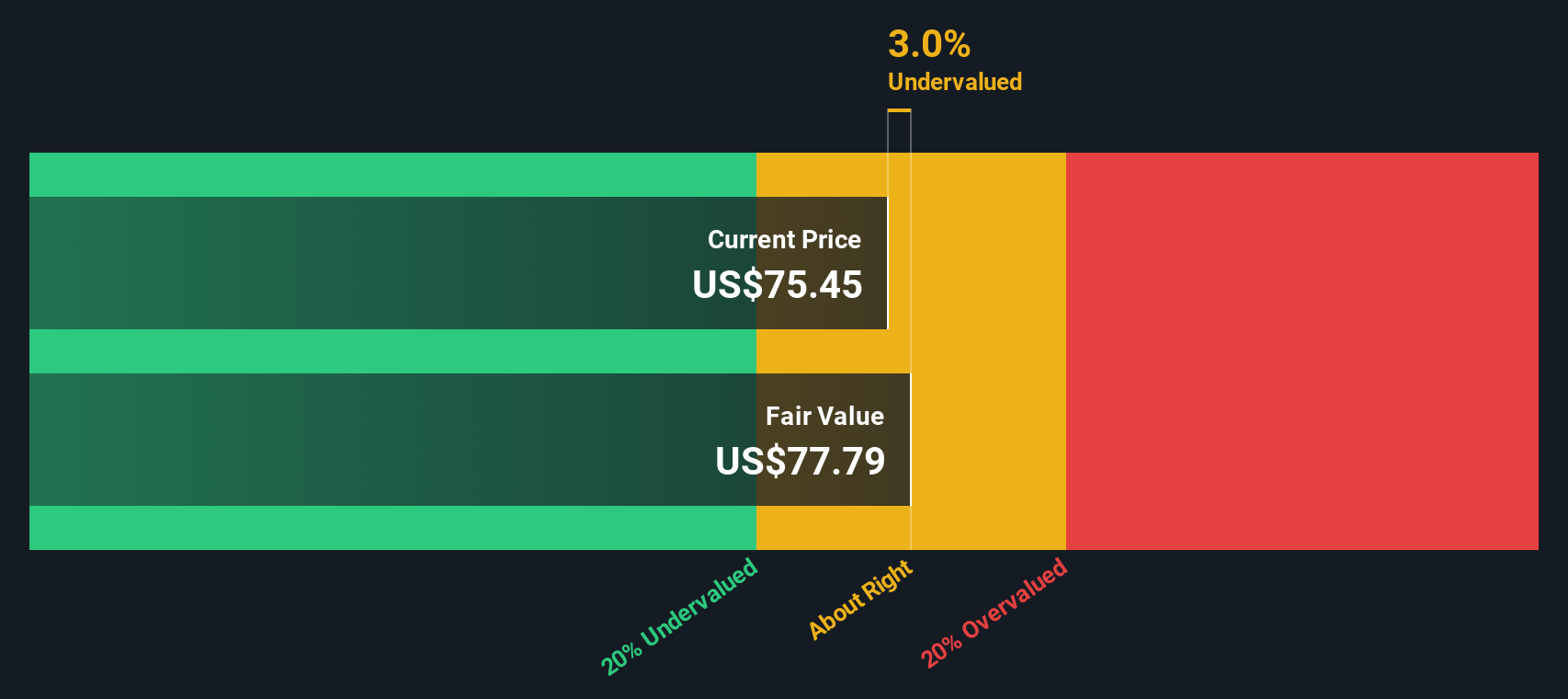

WNS demonstrates resilience through strategic investments and a favorable Price-To-Earnings Ratio of 19.4x, which is lower than both the industry and peer averages, indicating good value as it trades below its estimated fair value of $64.72. Facing challenges such as a revenue decline and margin compression, the company's focus on analytics and AI, along with its pursuit of over 20 large deals, positions it well for future growth. However, uncertainties in deal timings and external economic conditions may impact revenue stability and growth prospects. Overall, WNS's strategic initiatives and strong client trust provide a solid foundation for capitalizing on emerging opportunities, though vigilance is required to navigate potential market fluctuations.

Make It Happen

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

If you're looking to trade WNS (Holdings), open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if WNS (Holdings) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About NYSE:WNS

WNS (Holdings)

A business process management (BPM) company, provides data, voice, analytical, and business transformation services worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Community Narratives