- United States

- /

- Professional Services

- /

- NYSE:RHI

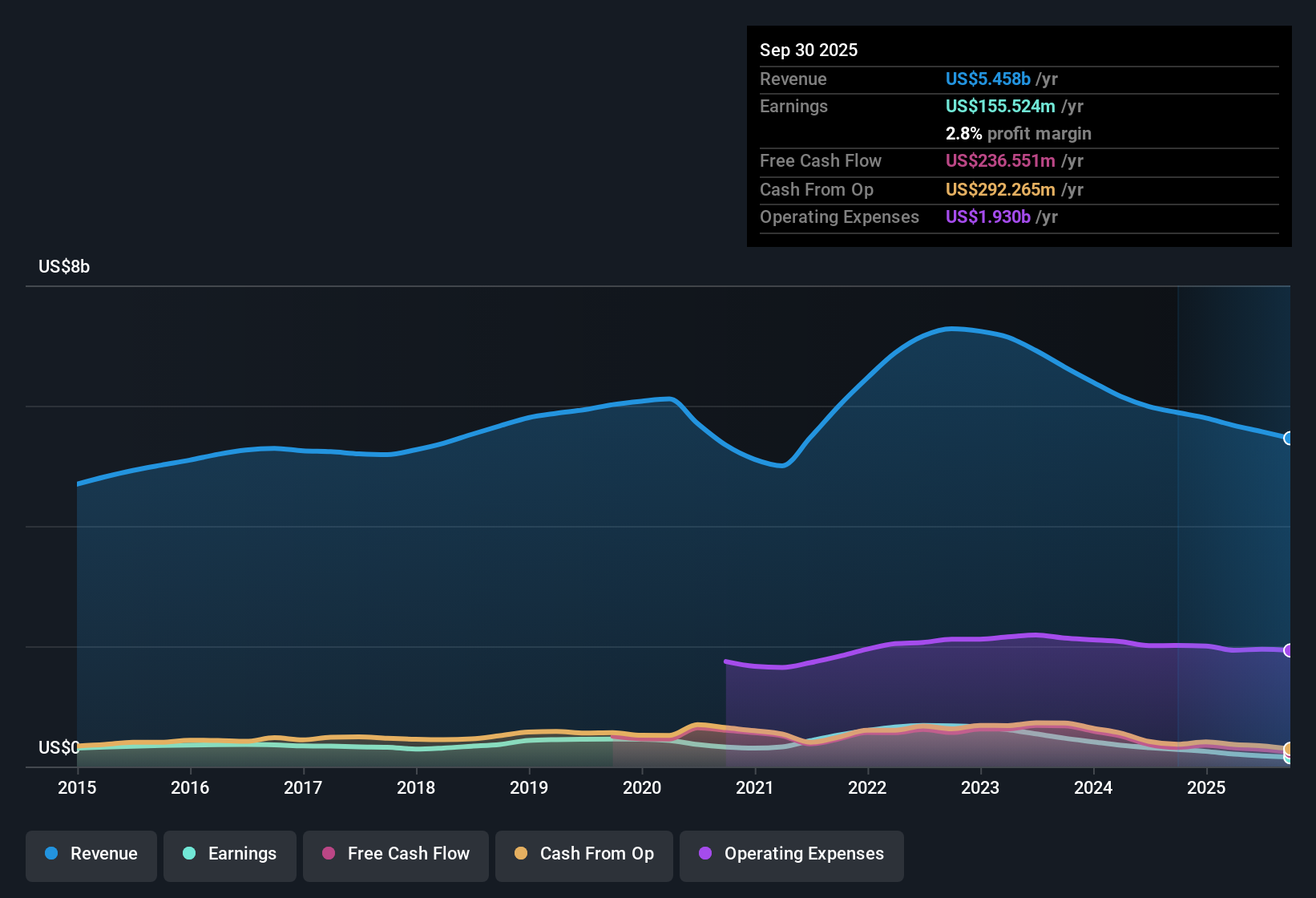

Robert Half (RHI) Net Margin Decline Reinforces Bearish Margin Pressure Concerns

Reviewed by Simply Wall St

Robert Half (RHI) reported net profit margins of 2.8%, which is a decline from last year’s 4.8%, and earnings have fallen by 12.8% per year over the past five years. The company’s net profit margin slipped further this year, continuing a negative earnings trend. However, forward-looking projections now call for annual EPS growth of 25.1% in the next few years. With the possibility of stronger profits ahead, investors have reasons to watch the stock closely as sentiment could shift if the company delivers on these forecasts.

See our full analysis for Robert Half.Next, let’s see how these reported numbers compare to the prevailing market narratives and whether any long-held views might need a rethink.

See what the community is saying about Robert Half

SG&A Costs Climb as Operating Pressures Mount

- SG&A expenses rose to 37.1% of revenue, up from 34% a year ago, eating into operating margins even as Talent Solutions SG&A climbed to 49.2% from 43.1% year over year.

- When tested against the consensus narrative, these rising costs highlight the tension between the company's investment in technology, such as AI-driven recruitment platforms, and the bearish worry that margin pressure could offset future growth.

- Consensus notes that investments are positioning Robert Half for efficiency and market share gains. However, persistent cost growth means robust execution is required to see margin rebound.

- The contrast between margin compression and tech-led productivity improvements will be crucial to watch as regulatory demands and digital competition both increase cost pressures.

Persistent Segment Declines Signal Growth Hurdles

- Talent Solutions revenues were down 11% year over year in Q2 2025, and third-quarter guidance projects another 8% decline at the midpoint, with flat or falling Protiviti revenues also weighing on overall momentum.

- Bears argue these figures reinforce structural headwinds, as sharper declines in administrative and permanent placement lines expose vulnerabilities to automation and industry shifts.

- Bearish concerns are underscored by weak demand trends and slower Protiviti growth, suggesting overreliance on legacy services may hinder recovery potential.

- Sustained revenue drops could challenge the narrative that demand for skilled talent and consulting will be enough to offset pressures from digital-native competitors.

Valuation Opportunity Despite Industry Premium

- With shares trading at $29.27 and the analyst price target at $36.44, Robert Half appears undervalued relative to consensus estimates. Its projected future PE ratio of 16.3x (2028) is below the US Professional Services industry’s current 26.3x.

- Analysts' consensus view emphasizes that while growing regulatory and digitization trends open up a larger addressable market, any expected upside relies on Robert Half’s ability to regain growth momentum and expand margins in the face of competitive and structural risks.

- The forecast jump in earnings per share from $3.04 by 2028, alongside ongoing share buybacks, is expected to drive value, but only if revenue and margin improvements materialize as projected.

- Subdued hiring activity and prolonged decision cycles could delay realization of that upside, underscoring the need for investors to continually reassess the valuation gap as new data emerges.

Strong catalysts and persistent risks make analyst expectations a moving target. See how the consensus perspective aligns with these figures in their latest narrative. 📊 Read the full Robert Half Consensus Narrative.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Robert Half on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have your own take on the numbers? Shape your outlook and build your narrative in just a few minutes. Do it your way

A great starting point for your Robert Half research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Ongoing revenue declines, shrinking margins, and cloudy growth prospects point to volatility. This may unsettle investors looking for reliability.

If consistent performance matters to you, use our stable growth stocks screener (2090 results) to focus on companies with a proven record of steady revenue and earnings through all market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:RHI

Robert Half

Provides talent solutions and business consulting services in the United States and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion