Advertisement

- United States

- /

- Professional Services

- /

- NYSE:PAYC

Is Paycom Software a Bargain After Its Recent 10% Slide in Early 2025?

Reviewed by Bailey Pemberton

If you are staring at Paycom Software’s ticker and wondering whether this is a moment to buy, hold, or move on, you are not alone. This stock has kept investors guessing with some wild rides and intriguing signals. Over the last week, Paycom’s stock crept up by 0.5%, suggesting a bit of life in an otherwise hesitant market. Zoom out to the past month and there is a shakeup, with shares sliding 9.6%. The story gets even more interesting when you pull back further, as the stock has jumped 23.0% in the past year. Looking out to three or five years, however, reveals larger slides, with declines of 35.1% and 46.5% respectively.

These swings can be attributed to shifting investor attitudes about the tech sector and evolving market dynamics, where confidence can change quickly. There has been no groundbreaking company-specific news to jolt the needle. However, broader market developments, such as renewed interest in workplace software and AI-driven productivity tools, have periodically boosted enthusiasm for stocks like Paycom’s. What does all of this say about the current value you are getting if you decide to own Paycom at today’s price of $201.3?

By the numbers, Paycom earns a value score of 4 out of 6 on a rigorous valuation check. This indicates that it is scoring as undervalued in most, but not quite all, of the typical ways that matter to investors. In the next section, I will break down exactly which methods point to an undervaluation and why, but I will also show you why a fuller picture matters more than any one approach alone.

Approach 1: Paycom Software Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and then discounting those back to today’s dollars. This approach helps investors judge whether a stock trades above or below its long-term earning potential, making it a popular tool to identify undervalued opportunities.

For Paycom Software, the latest reported Free Cash Flow stands at $350 million. Analysts forecast ongoing growth, with projections climbing to $779 million by the end of 2029. These forecasts suggest a steady path for Paycom’s cash generation over the next decade. Beyond the near term, additional growth estimates have been extrapolated based on industry trends and the company’s historical performance data.

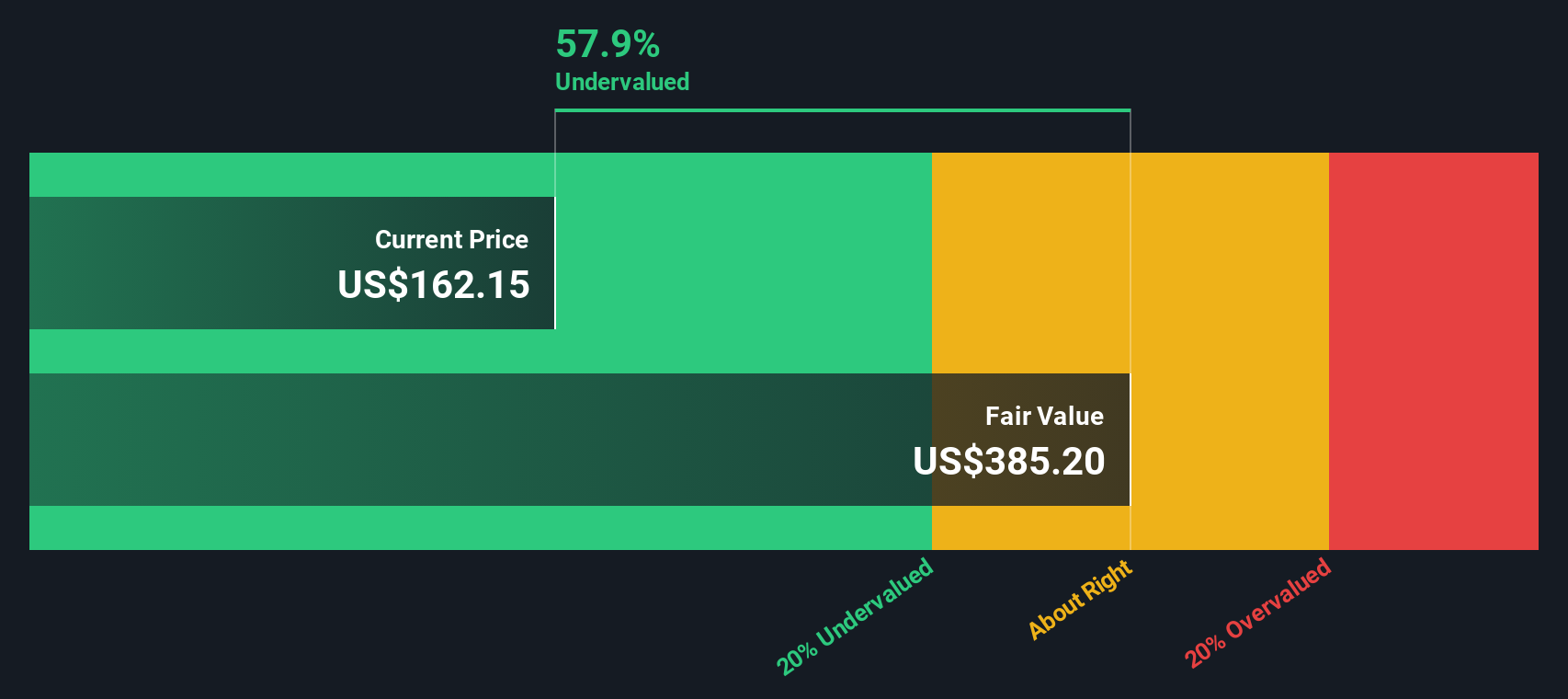

Based on these projections, the DCF model values Paycom Software at an intrinsic price of $390.72 per share. Compared to the recent share price of $201.3, this equates to a discount of about 48.5%. According to this method, Paycom’s current price is well below its long-term intrinsic value, signaling a significant undervaluation from the perspective of its future cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Paycom Software is undervalued by 48.5%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

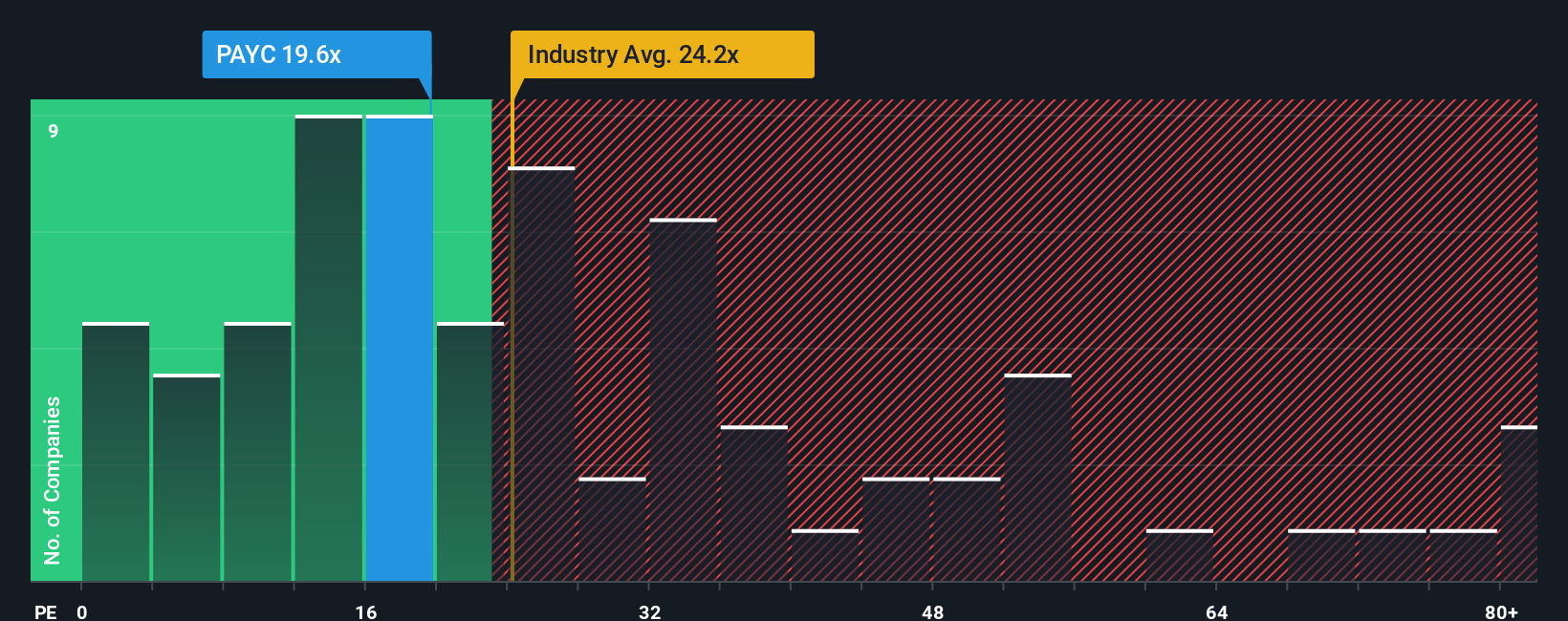

Approach 2: Paycom Software Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a widely accepted valuation method for profitable companies because it directly relates a company’s share price to its current earnings. For investors, it provides a straightforward way to gauge how much the market is willing to pay for a dollar of earnings. This is especially meaningful for tech firms like Paycom Software, which have steady profits and future growth potential.

However, what makes a “normal” or “fair” PE ratio can vary. Factors such as future growth prospects, business risks, and broader market sentiment all influence what ratio is considered reasonable. Generally, companies with higher expected earnings growth or lower risk profiles justify higher PE ratios. In contrast, slower growth or elevated risks typically lead investors to expect a discount.

Paycom Software’s current PE ratio stands at 27.2x. This is just below the average among its listed peers (28.7x) and a little above the broader Professional Services industry average (25.9x). However, direct comparisons might miss the nuances that matter most to long-term investors.

Simply Wall St’s Fair Ratio addresses this issue. For Paycom, the Fair PE Ratio is calculated at 27.1x. This tailored estimate weighs Paycom’s earnings growth outlook, market cap, profitability, and industry risks, offering a more individualized benchmark than a broad industry average. By adjusting for company-specific strengths and challenges, the Fair Ratio provides investors with a more complete sense of value.

With Paycom’s current PE of 27.2x and the Fair Ratio at 27.1x, the stock appears priced about right based on earnings power, risk, and growth potential.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Paycom Software Narrative

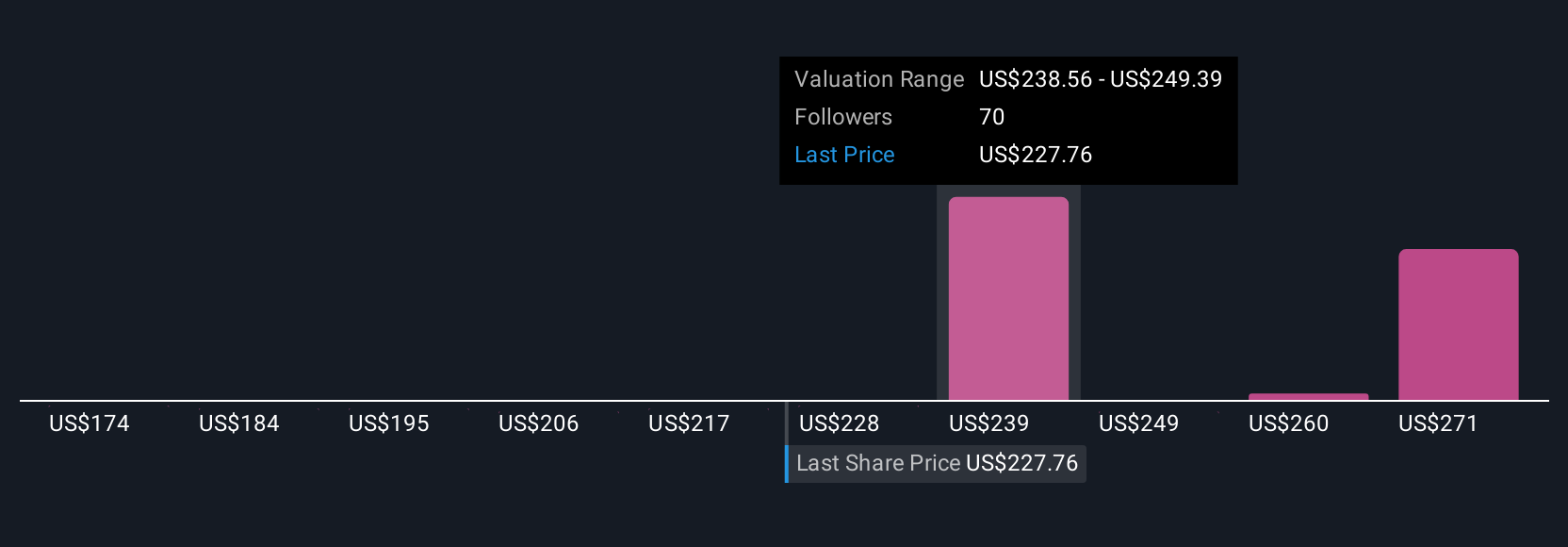

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is a simple, personalized story that connects your perspective on Paycom Software, including your assumptions about its future revenue, margins, and fair value, to its business outlook and turns raw data into a meaningful investment decision. Unlike a static ratio or a single forecast, a Narrative links what you believe will drive Paycom’s performance to a dynamic financial model that responds as actual news and updates arrive.

This approach is available and easy to use for everyone on Simply Wall St’s Community page, where millions of investors track, refine, and compare their own Narratives. Narratives help you make clear buy or sell decisions by letting you compare your Fair Value estimate, rooted in your personal story for the stock, directly to the latest market price. They stay relevant because whenever important news such as quarterly earnings or major announcements hits, your Narrative updates automatically to keep your forecast and valuation current without manual work.

For example, one investor’s Narrative may predict Paycom’s fair value as high as $311 based on rapid AI adoption and market share gains. Another might set it closer to $208 if they believe margin pressure and industry headwinds will prevail. Narratives let you invest in alignment with your own informed outlook, not someone else’s headline.

Do you think there's more to the story for Paycom Software? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PAYC

Paycom Software

Provides cloud-based human capital management (HCM) solution delivered as software-as-a-service for small to mid-sized companies in the United States.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.562.2% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.9% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.6% overvalued

42 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.9% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

ST

StoxEurope on Sipef ·

Why I Invest in SIPEF?

Fair Value:€12125.5% undervalued

13 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on Kucingko Berhad ·

Kucingko Berhad: Fundamentals Show Early Recovery as Creative Content Expansion Gains Traction

Fair Value:RM 0.012733.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

Blagget on BP Silver ·

“valer un Potosí” GOOGLE IT. Now you’re should be kinda locked in. Educate yourself, Read the rest.

Fair Value:CA$685.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.5% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

AN

andre_k1tsg on Companhia de Saneamento de Minas Gerais ·

Eu André José Julião digo o caminho da melhorar a toda população esta entrando no trilhos.

0

|0