Advertisement

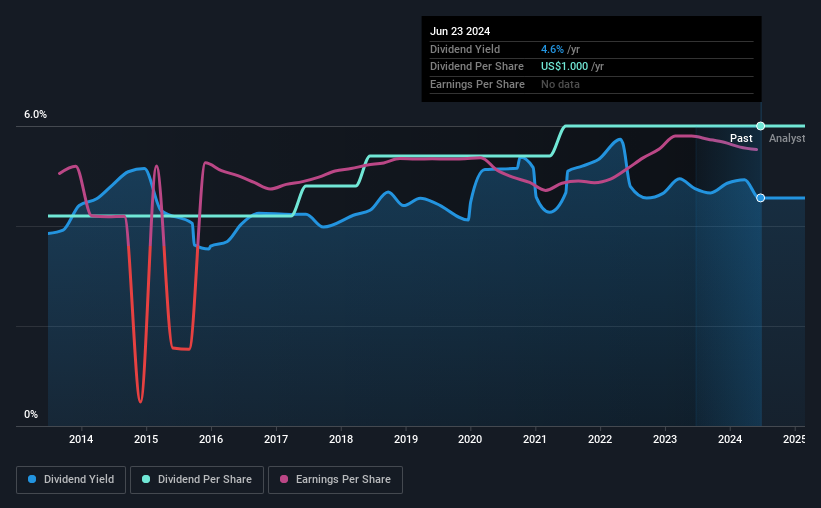

Ennis, Inc.'s (NYSE:EBF) investors are due to receive a payment of $0.25 per share on 5th of August. This means the annual payment is 4.6% of the current stock price, which is above the average for the industry.

View our latest analysis for Ennis

Ennis' Payment Has Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. The last dividend was quite easily covered by Ennis' earnings. This means that a large portion of its earnings are being retained to grow the business.

If the trend of the last few years continues, EPS will grow by 2.0% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio will be 64%, which is in the range that makes us comfortable with the sustainability of the dividend.

Ennis Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. Since 2014, the annual payment back then was $0.70, compared to the most recent full-year payment of $1.00. This works out to be a compound annual growth rate (CAGR) of approximately 3.6% a year over that time. Dividends have grown relatively slowly, which is not great, but some investors may value the relative consistency of the dividend.

Ennis May Find It Hard To Grow The Dividend

Investors could be attracted to the stock based on the quality of its payment history. Unfortunately, Ennis' earnings per share has been essentially flat over the past five years, which means the dividend may not be increased each year. Growth of 2.0% per annum is not particularly high, which might explain why the company is paying out a higher proportion of earnings. This isn't necessarily bad, but we wouldn't expect rapid dividend growth in the future.

We Really Like Ennis' Dividend

In summary, it is good to see that the dividend is staying consistent, and we don't think there is any reason to suspect this might change over the medium term. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All of these factors considered, we think this has solid potential as a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. You can also discover whether shareholders are aligned with insider interests by checking our visualisation of insider shareholdings and trades in Ennis stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Ennis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EBF

Ennis

Produces and sells business forms and other printed products in the United States.

Flawless balance sheet 6 star dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor