Advertisement

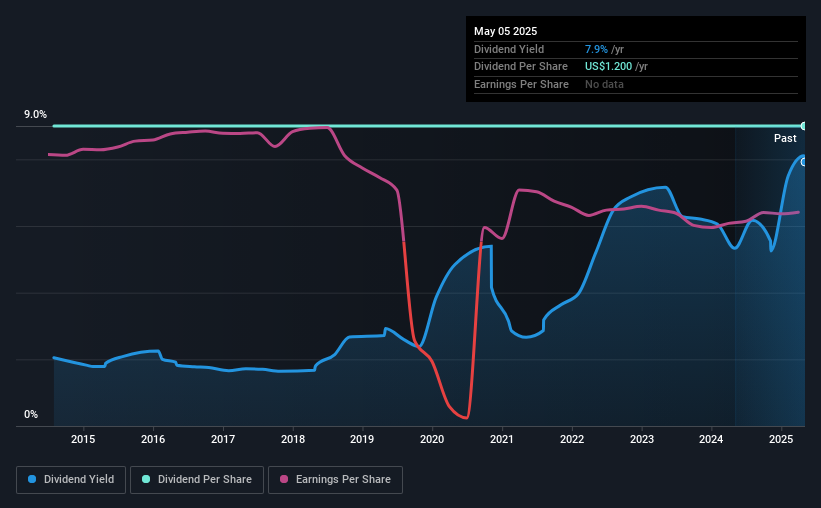

Deluxe Corporation (NYSE:DLX) will pay a dividend of $0.30 on the 2nd of June. This means the annual payment is 7.9% of the current stock price, which is above the average for the industry.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Deluxe's stock price has reduced by 34% in the last 3 months, which is not ideal for investors and can explain a sharp increase in the dividend yield.

Deluxe's Payment Could Potentially Have Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. The last payment made up 95% of earnings, but cash flows were much higher. This leaves plenty of cash for reinvestment into the business.

Earnings per share is forecast to rise by 21.8% over the next year. Assuming the dividend continues along recent trends, our estimates say the payout ratio could reach 79% - on the higher side, but we wouldn't necessarily say this is unsustainable.

See our latest analysis for Deluxe

Deluxe Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. The last annual payment of $1.20 was flat on the annual payment from10 years ago. Although we can't deny that the dividend has been remarkably stable in the past, the growth has been pretty muted.

Deluxe's Dividend Might Lack Growth

Investors could be attracted to the stock based on the quality of its payment history. We are encouraged to see that Deluxe has grown earnings per share at 44% per year over the past five years. Fast growing earnings are great, but this can rarely be sustained without some reinvestment into the business, which Deluxe hasn't been doing.

Our Thoughts On Deluxe's Dividend

Overall, a consistent dividend is a good thing, and we think that Deluxe has the ability to continue this into the future. The payments look pretty sustainable with good earnings coverage and a reasonable track record. This looks like it could be a good dividend stock going forward, but we would note that the payout ratio has been at higher levels in the past so it could happen again.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, Deluxe has 3 warning signs (and 1 which doesn't sit too well with us) we think you should know about. Is Deluxe not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:DLX

Deluxe

Provides technology-enabled solutions to small and medium-sized businesses, and financial institutions in the United States and Canada.

Undervalued with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.2% undervalued

TO

Community Contributor