Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGM:WLDN

Willdan Group (WLDN) Valuation After E3’s Amazon-Funded Data Center Power Study Elevates Its Energy Planning Role

Willdan Group (WLDN) is back on investors radar after its E3 subsidiary released an independent study for Amazon on how utilities should price and manage surging data center driven electric load.

See our latest analysis for Willdan Group.

That Amazon backed study is landing at a time when Willdan’s 1 month share price return of 8.2 percent builds on a powerful year to date run of 175.4 percent. Its 3 year total shareholder return of 478.8 percent underlines how long term momentum has steadily compounded.

If this kind of demand side story has your attention, it could be worth exploring fast growing stocks with high insider ownership as a way to spot other fast moving opportunities before they become crowded trades.

Yet with the shares already up sharply and still trading at a sizeable discount to analyst targets and some intrinsic value estimates, is Willdan Group quietly undervalued here, or is the market already baking in years of growth?

Most Popular Narrative: 21.7% Undervalued

With Willdan Group last closing at $103.77 versus a most popular narrative fair value of $132.50, the story implies further upside driven by long term growth.

Ongoing investments and planning for grid modernization, combined with the company's strong reputation with utility commissions and government agencies, position Willdan to benefit disproportionately from federal/state decarbonization mandates and infrastructure modernization initiatives, supporting sustained revenue and EBITDA growth over the long term.

Want to see what is baked into that optimism? The narrative leans on accelerating revenue, rising margins, and a premium future earnings multiple. Curious how bold those assumptions really are? Read on to unpack the full valuation logic behind that target price.

Result: Fair Value of $132.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, a higher effective tax rate and heavy reliance on policy-driven utility spending could quickly squeeze margins and derail those upbeat growth assumptions.

Find out about the key risks to this Willdan Group narrative.

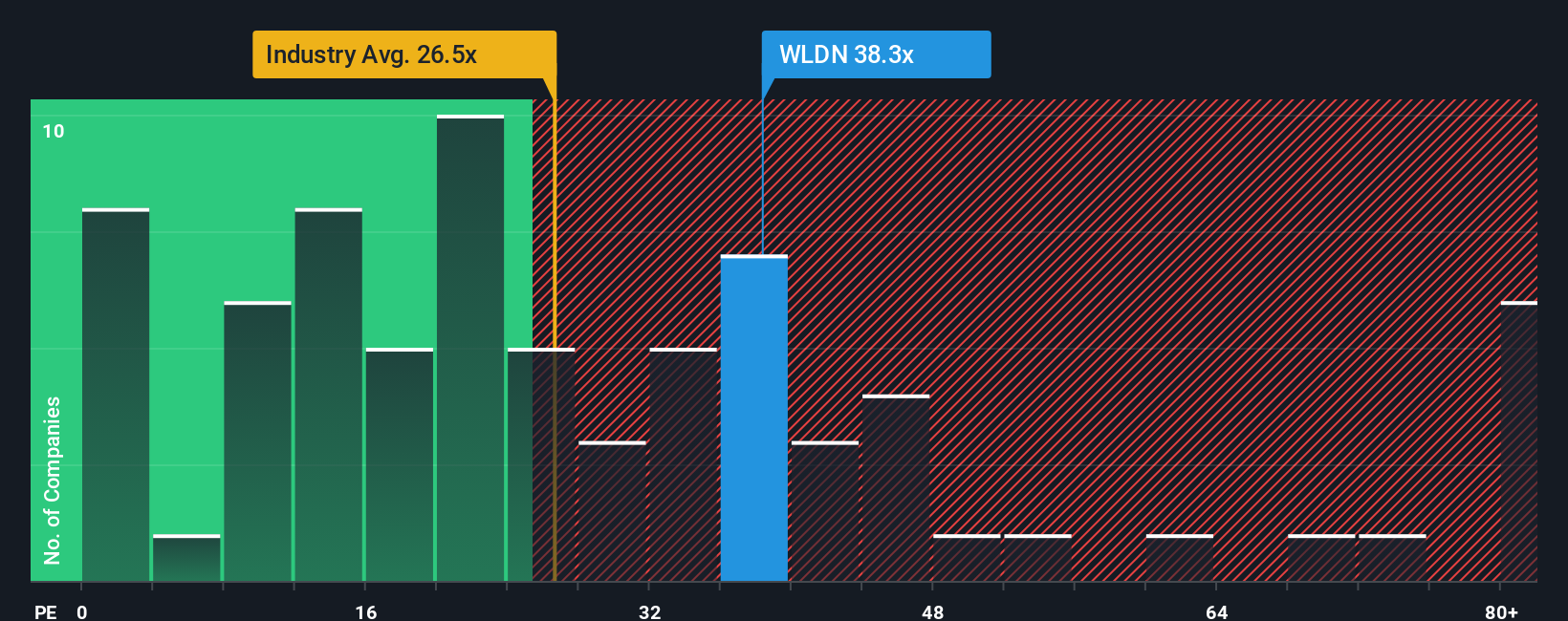

Another View: Market Ratios Flash a Caution Sign

While narratives and intrinsic estimates point to upside, the market’s own yardstick looks stretched. Willdan trades on a P/E of 36.9 times, well above the Professional Services industry at 24.8 times and its fair ratio of 22.9 times. If sentiment cools, multiple compression could erase a chunk of those projected gains.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Willdan Group Narrative

If you see the story differently or want to stress test these assumptions with your own research, you can build a full narrative in minutes: Do it your way.

A great starting point for your Willdan Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, put Simply Wall Street’s powerful Screener to work so you do not miss fresh opportunities that could reshape your portfolio.

- Tap into early stage potential with these 3625 penny stocks with strong financials that already boast solid financial foundations instead of risky story stocks.

- Capitalize on the AI transformation in healthcare by reviewing these 30 healthcare AI stocks building real solutions for diagnosis, treatment, and patient outcomes.

- Lock in reliable income streams by scanning these 13 dividend stocks with yields > 3% that combine healthy yields with supportable payout ratios.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Willdan Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:WLDN

Willdan Group

Provides professional, technical, and consulting services through engineering, program management, policy advisory, and software and data analytics primarily in the United States.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5361.6% undervalued

139 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18054.9% undervalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.319.9% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2449.4% undervalued

33 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

KA

kapirey on STIF Société anonyme ·

STIF Société anonyme will achieve 14% revenue growth with a focus on future gains

Fair Value:€43.6317.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Palantir Technologies ·

Palantir is strategic geopolitical asset at the intersection of AI, defense, and Western alliances.

Fair Value:US$120.1411.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Village Farms International ·

VFF is a vertically integrated, low-cost cannabis producer

Fair Value:US$4.7244.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.6% undervalued

111 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74017.0% undervalued

38 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.1% undervalued

1182 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative