Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:TASK

TaskUs (NASDAQ:TASK) Might Have The Makings Of A Multi-Bagger

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Speaking of which, we noticed some great changes in TaskUs' (NASDAQ:TASK) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for TaskUs:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

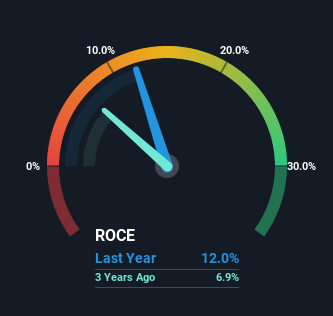

0.12 = US$95m ÷ (US$902m - US$110m) (Based on the trailing twelve months to December 2022).

So, TaskUs has an ROCE of 12%. That's a pretty standard return and it's in line with the industry average of 12%.

Check out our latest analysis for TaskUs

Above you can see how the current ROCE for TaskUs compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for TaskUs.

What The Trend Of ROCE Can Tell Us

We like the trends that we're seeing from TaskUs. Over the last four years, returns on capital employed have risen substantially to 12%. Basically the business is earning more per dollar of capital invested and in addition to that, 44% more capital is being employed now too. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

The Bottom Line

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what TaskUs has. Given the stock has declined 53% in the last year, this could be a good investment if the valuation and other metrics are also appealing. That being the case, research into the company's current valuation metrics and future prospects seems fitting.

While TaskUs looks impressive, no company is worth an infinite price. The intrinsic value infographic in our free research report helps visualize whether TASK is currently trading for a fair price.

While TaskUs isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if TaskUs might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TASK

TaskUs

Provides outsourced digital services for companies in Philippines, the United States, India, and internationally.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7060.2% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.226.4% undervalued

32 followersusers have followed this narrative

7 commentsusers have commented on this narrative

10 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0542.8% undervalued

37 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.9% undervalued

86 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

WI

Wizkhalifa on PSP Energy Berhad ·

PSP Energy Breaks Key Downtrend, Momentum Building for Further Upside

Fair Value:RM 0.09257.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

Bakullizta on Indofood CBP Sukses Makmur ·

Blindly Bullish on Indofood CBP Sukses Makmur's 5.3% Revenue Growth

Fair Value:Rp9.05k31.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on CSL ·

CSL Investment Thesis

Fair Value:AU$14023.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.9% undervalued

59 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9724.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1935.7% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0