- United States

- /

- Machinery

- /

- OTCPK:NMHI

Nature's Miracle Holding Inc.'s (NASDAQ:NMHI) 81% Dip Still Leaving Some Shareholders Feeling Restless Over Its P/SRatio

Nature's Miracle Holding Inc. (NASDAQ:NMHI) shareholders that were waiting for something to happen have been dealt a blow with a 81% share price drop in the last month. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 91% loss during that time.

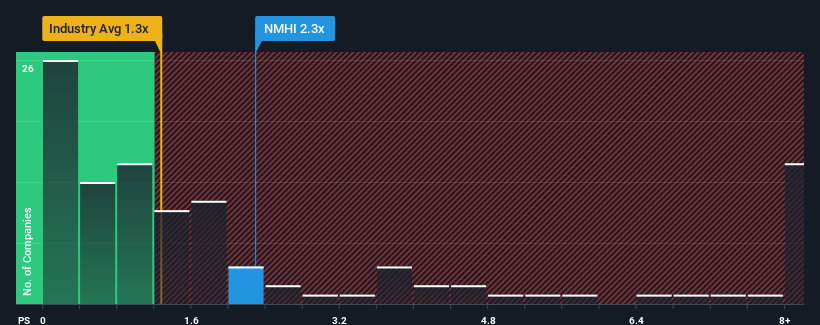

Even after such a large drop in price, when almost half of the companies in the United States' Commercial Services industry have price-to-sales ratios (or "P/S") below 1.3x, you may still consider Nature's Miracle Holding as a stock probably not worth researching with its 2.3x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Nature's Miracle Holding

How Nature's Miracle Holding Has Been Performing

Nature's Miracle Holding has been doing a good job lately as it's been growing revenue at a solid pace. It might be that many expect the respectable revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Nature's Miracle Holding's earnings, revenue and cash flow.How Is Nature's Miracle Holding's Revenue Growth Trending?

In order to justify its P/S ratio, Nature's Miracle Holding would need to produce impressive growth in excess of the industry.

Taking a look back first, we see that the company grew revenue by an impressive 17% last year. Still, revenue has fallen 3.9% in total from three years ago, which is quite disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 8.5% shows it's an unpleasant look.

With this in mind, we find it worrying that Nature's Miracle Holding's P/S exceeds that of its industry peers. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

The Final Word

Nature's Miracle Holding's P/S remain high even after its stock plunged. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Nature's Miracle Holding revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. With a revenue decline on investors' minds, the likelihood of a souring sentiment is quite high which could send the P/S back in line with what we'd expect. Should recent medium-term revenue trends persist, it would pose a significant risk to existing shareholders' investments and prospective investors will have a hard time accepting the current value of the stock.

You need to take note of risks, for example - Nature's Miracle Holding has 5 warning signs (and 4 which can't be ignored) we think you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

If you're looking to trade Nature's Miracle Holding, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nature's Miracle Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:NMHI

Nature's Miracle Holding

An agriculture technology company, provides lighting and grow media products to growers in the controlled environment agriculture industry in the United States and Canada.

Undervalued with high growth potential.

Market Insights

Community Narratives