Advertisement

- United States

- /

- Commercial Services

- /

- NasdaqGS:HCSG

Healthcare Services Group (HCSG): Reassessing Valuation After a Strong 3-Month and 1-Year Share Price Rebound

Simply Wall St

Reviewed by Simply Wall St

Healthcare Services Group (HCSG) has quietly put together a solid comeback, with the stock up roughly 19% over the past 3 months and more than 50% over the past year, outpacing broader healthcare services peers.

See our latest analysis for Healthcare Services Group.

That performance has come as investors warm to a cleaner story around Healthcare Services Group, with a 90 day share price return of about 19% and a 1 year total shareholder return above 50%. This suggests momentum is clearly building after years of underperformance.

If this rebound has you rethinking the space, it could be worth exploring other healthcare stocks that are showing improving fundamentals and renewed interest from investors.

Yet despite the strong rebound and improving earnings, HCSG still trades below analyst targets and faces a mixed long term track record. This raises the question: is this a genuine value opportunity, or is the market already pricing in a full recovery?

Most Popular Narrative: 12.6% Undervalued

With Healthcare Services Group closing at $18.79 against a narrative fair value of $21.50, the valuation case leans toward meaningful upside if assumptions hold.

The analysts have a consensus price target of $17.0 for Healthcare Services Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $19.0, and the most bearish reporting a price target of just $15.0.

Curious how steady mid single digit growth, a sharp margin reset, and a much lower future earnings multiple can still point higher from here? The real twist is how these moving parts interact over time. Want to see the exact profit and valuation path this narrative is banking on? Dive into the full breakdown to uncover the numbers behind that fair value.

Result: Fair Value of $21.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent client concentration and labor cost pressures could quickly erode margins and challenge the optimistic earnings and valuation assumptions embedded in this narrative.

Find out about the key risks to this Healthcare Services Group narrative.

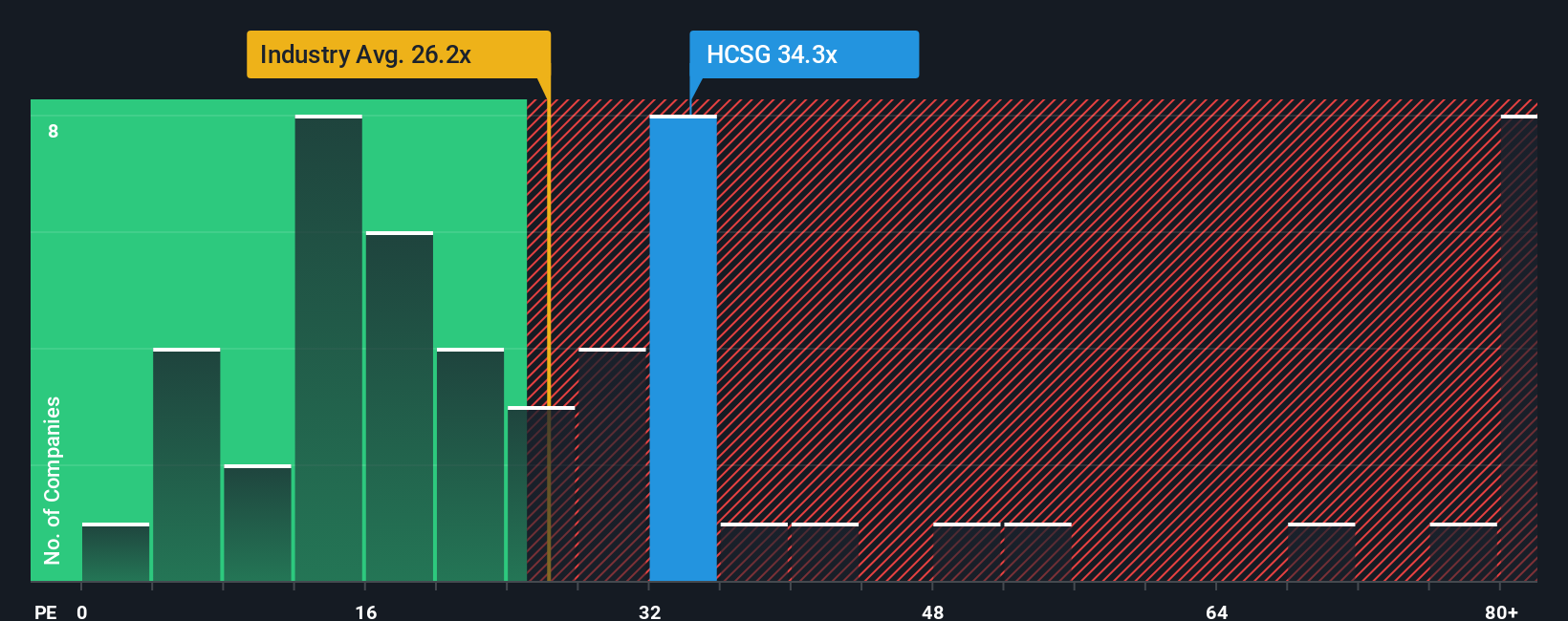

Another View: Market Multiples Flash a Warning

Step away from narrative fair value and the picture shifts. On current numbers, HCSG trades at about 33 times earnings versus roughly 23 times for both peers and the broader commercial services group, and above a fair ratio of 25 times. That premium leaves far less room for mistakes, so how confident are you in the recovery story?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Healthcare Services Group Narrative

If you see things differently or want to dig into the numbers yourself, you can build a personalised view of HCSG in just minutes: Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Healthcare Services Group.

Looking for more investment ideas?

Before you move on, lock in your next smart move with targeted stock ideas from the Simply Wall St Screener, built to match what you care about most.

- Boost your income potential by scanning these 15 dividend stocks with yields > 3% that can strengthen a portfolio with reliable cash returns.

- Ride structural growth trends by focusing on these 26 AI penny stocks positioned at the heart of transformative technology.

- Sharpen your value strategy with these 907 undervalued stocks based on cash flows that may still be flying under the market's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Healthcare Services Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HCSG

Healthcare Services Group

Provides management, administrative, and operating services to the housekeeping, laundry, linen, facility maintenance, and dietary service departments of nursing homes, retirement complexes, rehabilitation centers, and hospitals in the United States.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

43 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.6% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative