Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:ADP

Automatic Data Processing (NASDAQ:ADP) Seems To Use Debt Quite Sensibly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Automatic Data Processing, Inc. (NASDAQ:ADP) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Automatic Data Processing's Net Debt?

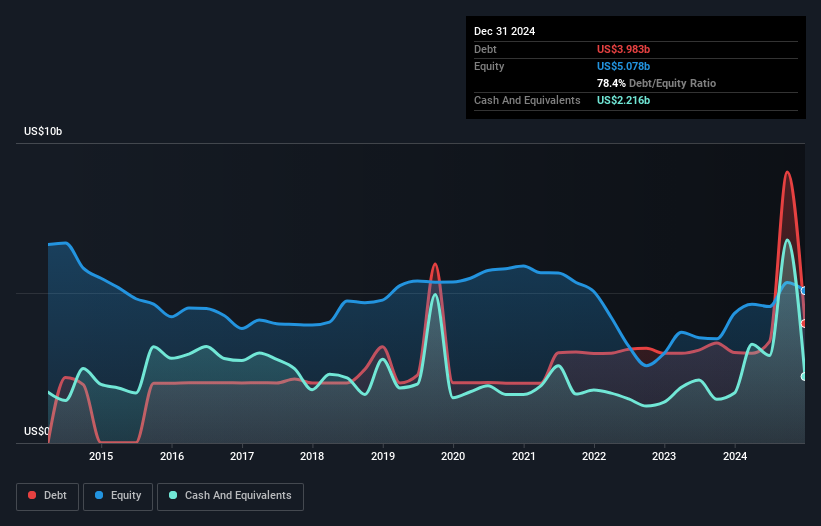

As you can see below, at the end of December 2024, Automatic Data Processing had US$3.98b of debt, up from US$3.01b a year ago. Click the image for more detail. On the flip side, it has US$2.22b in cash leading to net debt of about US$1.77b.

How Healthy Is Automatic Data Processing's Balance Sheet?

The latest balance sheet data shows that Automatic Data Processing had liabilities of US$54.3b due within a year, and liabilities of US$4.72b falling due after that. Offsetting these obligations, it had cash of US$2.22b as well as receivables valued at US$3.50b due within 12 months. So it has liabilities totalling US$53.3b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Automatic Data Processing is worth a massive US$121.6b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Carrying virtually no net debt, Automatic Data Processing has a very light debt load indeed.

See our latest analysis for Automatic Data Processing

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Automatic Data Processing's net debt is only 0.30 times its EBITDA. And its EBIT covers its interest expense a whopping 44.5 times over. So we're pretty relaxed about its super-conservative use of debt. And we also note warmly that Automatic Data Processing grew its EBIT by 11% last year, making its debt load easier to handle. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Automatic Data Processing's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Automatic Data Processing recorded free cash flow worth 74% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that Automatic Data Processing's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its level of total liabilities does undermine this impression a bit. Taking all this data into account, it seems to us that Automatic Data Processing takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. Over time, share prices tend to follow earnings per share, so if you're interested in Automatic Data Processing, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ADP

Automatic Data Processing

Provides cloud-based human capital management (HCM) solutions worldwide.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

61 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

JA

Jades on Coca-Cola ·

Coca-Cola’s Enduring Moat in a Health-Conscious World: Steady Compounder Poised for 5-10% Annual Returns Through Emerging Market Dominance

Fair Value:US$66.221.2% overvalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

ET

Ethan_cpa on Xero ·

Xero: Growth Was Priced In — Execution Is Not

Fair Value:AU$101.5622.4% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.4% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

Recently Updated Narratives

VA

Vallix on Telix Pharmaceuticals ·

TLX... a Market's Overreaction or a Falling Knife?

Fair Value:AU$1845.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kabstck on Sims ·

Rally in sustainable practices over value recyclable metal stock

Fair Value:AU$18.0717.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Regeneron Pharmaceuticals ·

Regeneron Pharmaceuticals Inc. (REGN): The Biotech Stalwart – Defensive Growth Amid Biosimilar Headwinds in 2026.

Fair Value:US$893.8811.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.0% undervalued

65 followersusers have followed this narrative

5 commentsusers have commented on this narrative

28 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.1% undervalued

1300 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.4% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

Trending Discussion

US

User on Caesars Entertainment ·

I can't take seriously any analysis of Caesars Entertainment when there is not present (at least onc...

0

|0