Advertisement

Wabash National Corporation (NYSE:WNC) has announced that it will pay a dividend of $0.08 per share on the 24th of July. The dividend yield will be 3.3% based on this payment which is still above the industry average.

We've discovered 3 warning signs about Wabash National. View them for free.Wabash National's Distributions May Be Difficult To Sustain

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. While Wabash National is not profitable, it is paying out less than 75% of its free cash flow, which means that there is plenty left over for reinvestment into the business. This gives us some comfort about the level of the dividend payments.

Over the next year, EPS is forecast to rise by 44.8%. We like to see the company moving towards profitability, but this probably won't be enough for it to post positive net income this year. The positive free cash flows give us some comfort, however, that the dividend could continue to be sustained.

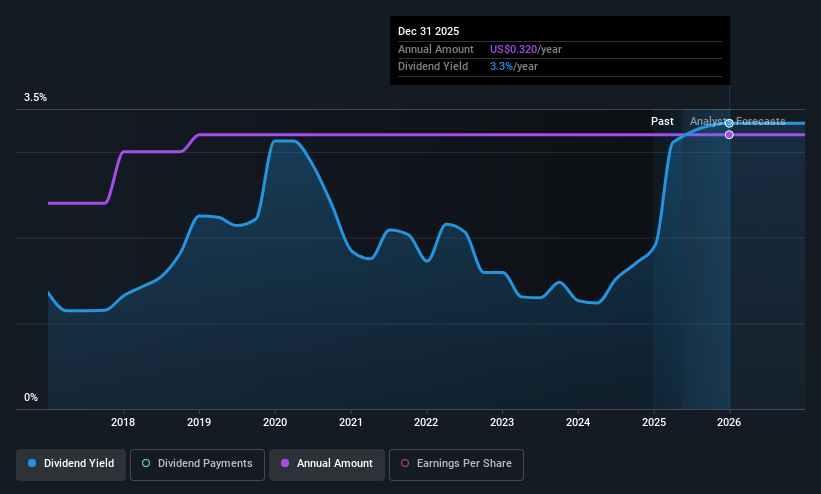

Check out our latest analysis for Wabash National

Wabash National Is Still Building Its Track Record

Wabash National's dividend has been pretty stable for a little while now, but we will continue to be cautious until it has been demonstrated for a few more years. Since 2017, the annual payment back then was $0.24, compared to the most recent full-year payment of $0.32. This works out to be a compound annual growth rate (CAGR) of approximately 3.7% a year over that time. Modest dividend growth is good to see, especially with the payments being relatively stable. However, the payment history is relatively short and we wouldn't want to rely on this dividend too much.

The Dividend Has Growth Potential

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Wabash National has impressed us by growing EPS at 7.5% per year over the past five years. It's not an ideal situation that the company isn't turning a profit but the growth recently is a positive sign. All is not lost, but the future of the dividend definitely rests upon the company's ability to become profitable soon.

In Summary

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Wabash National's payments, as there could be some issues with sustaining them into the future. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 3 warning signs for Wabash National that investors need to be conscious of moving forward. Is Wabash National not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Wabash National might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WNC

Wabash National

Manufactures engineered solutions and services for transportation, logistics and infrastructure industry in the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor