Advertisement

Today, we'll take a closer look at 3M Company (NYSE:MMM) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. Finding a good, stable company, with a decent yield, that is in a growing market can be a great opportunity for long-term investors.

First, we will take a broad overview of performance.

The value drivers of 3M are the trailing 12-month revenue growth of 10.8%, the EBIT margin of 22.7%, Return of Capital Employed of 21% and the cost of Equity 6.4%. The company has trailing 12-month revenues of US$34.7b and US$5.9b in net income.

Explore this interactive chart for our latest analysis on 3M!

The company also increased the 2021 full-year guidance from US$9.7 to $US10.1 (upper bound). This shows that the expectation is that the company is still in a growing market.

They have reinvested around US$3b in their business (mostly stemming from the 3 year value of their research assets) and their expected fundamental growth rate is about 4%. It seems that MMM, has a good fundamental performance across the years and may have a good chance to increase the size and sales over the long run. Even though the next few quarters may present higher growth, we can see that the company is in a mature phase and cannot't expect a double-digit growth rate from current projects and operations.

A mature company, can still be a great income investment, so let's dig into dividends.

Dividend Performance

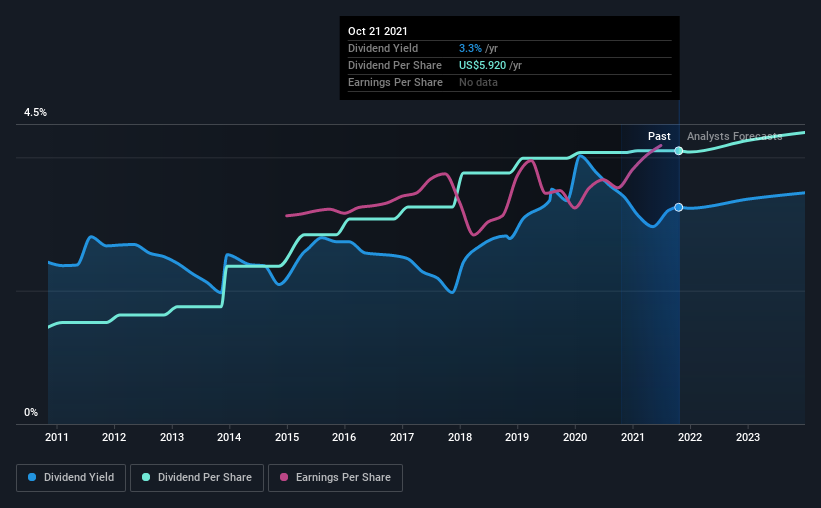

With 3M yielding 3.3% and having paid a dividend for over 10 years, many investors likely find the company quite interesting. The company seems to be currently trading at a stable long-term price, so the dividend yield can be quite attractive along with less downside risk.

We'd guess that plenty of investors have purchased it for the income. Some simple research can reduce the risk of buying 3M for its dividend - read on to learn more.

Payout ratios

Here, we will investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax.

3M paid out 58% of its profit as dividends, over the trailing twelve-month period. This is a healthy payout ratio, signaling that the company is committed to returning cash to investors.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. 3M paid out a conservative 48% of its free cash flow as dividends last year.

It's positive to see that 3M's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable.

We update our data on 3M every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility & Growth

The dividend has been stable over the past 10 years, which is great.

During the past 10-year period, the first annual payment was US$2.1 in 2011, compared to US$5.9 last year. This works out to be a compound annual growth rate (CAGR) of approximately 11% a year over that time.

Earnings have grown at around 5.0% a year for the past five years, which is great for a mature company!

Key Takeaways

First, we think 3M has an acceptable payout ratio and its dividend is well covered by cashflow.

Second, earnings growth has been stable, and dividends have been relatively stable and slowly growing. 3M has a number of positive attributes, but it definitely isn't at the beginning of high growth, and the long-term stability is the central feature the company.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

Valuation is complex, but we're here to simplify it.

Discover if 3M might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:MMM

3M

Provides diversified technology services in the Americas, the Asia Pacific, Europe, the Middle East, Africa, and internationally.

Good value low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor