Advertisement

- United States

- /

- Machinery

- /

- NYSE:KAI

Is Kadant’s (KAI) Margin Resilience Amid Trade Headwinds Enhancing Its Investment Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

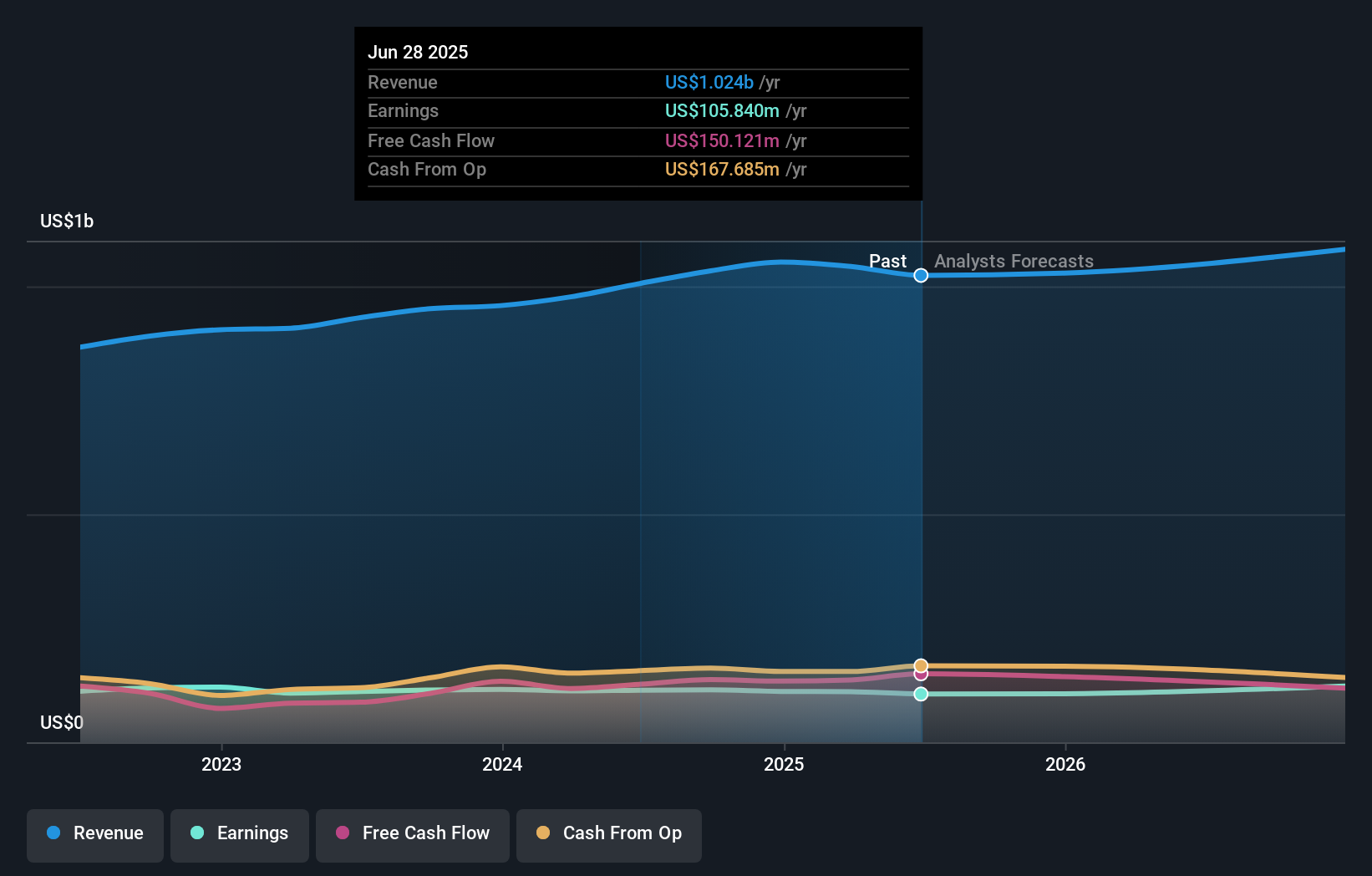

- Kadant recently reported quarterly revenues of US$271.6 million, which were flat year-over-year but exceeded analyst expectations by 4.2% with strong gross margin performance despite global trade uncertainties and weaker capital equipment demand.

- An interesting insight is that while a director executed an insider sale of 1,435 shares valued at about US$405,179, no insider purchases have occurred over the past year, but such sales are not necessarily an indication of company outlook.

- We will explore how Kadant’s ability to outperform analyst expectations amid challenging market conditions impacts its broader investment narrative.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 35 companies in the world exploring or producing it. Find the list for free.

Kadant Investment Narrative Recap

To be a Kadant shareholder, you need to believe in its global leadership in critical process solutions and its ability to maintain robust aftermarket parts demand, even as broader capital equipment orders slow. The recent revenue beat and strong gross margins, despite trade uncertainties and weaker equipment demand, support this resilience, but do not materially change the primary near-term catalyst of continued aftermarket growth or the biggest risk of delayed capital equipment orders amid global trade challenges.

Among recent announcements, the October debt facility expansion stands out, increasing Kadant’s financial flexibility and enabling ongoing investment in core growth areas and acquisitions. This move is particularly relevant given the uncertain project timing in the capital equipment segment and may help the company manage through uneven global demand cycles.

By contrast, investors should be aware that revenue timing can quickly become less predictable when capital equipment orders are…

Read the full narrative on Kadant (it's free!)

Kadant's narrative projects $1.1 billion revenue and $141.4 million earnings by 2028. This requires 3.5% yearly revenue growth and a $35.6 million earnings increase from $105.8 million today.

Uncover how Kadant's forecasts yield a $343.33 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Two community valuations of Kadant put fair value between US$200 and US$270, both below current trading levels. However, many are closely watching how delayed capital equipment orders and trade policy risks could shape Kadant’s financial resilience and long-term prospects, explore several alternative viewpoints to form your own conclusion.

Explore 2 other fair value estimates on Kadant - why the stock might be worth as much as $270.49!

Build Your Own Kadant Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kadant research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Kadant research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kadant's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kadant might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KAI

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative