- United States

- /

- Machinery

- /

- NYSE:IR

Ingersoll Rand Inc.'s (NYSE:IR) Share Price Matching Investor Opinion

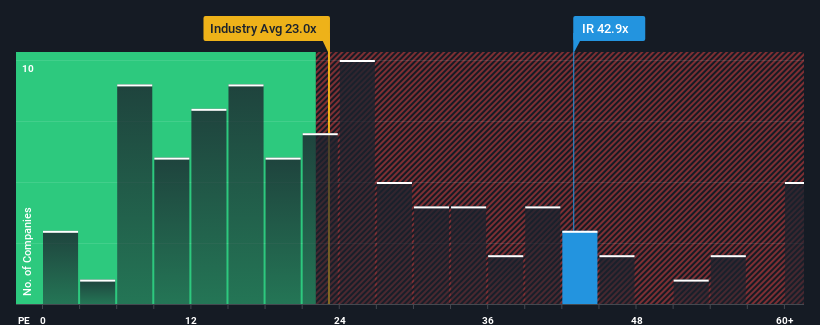

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 18x, you may consider Ingersoll Rand Inc. (NYSE:IR) as a stock to avoid entirely with its 42.9x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With earnings growth that's superior to most other companies of late, Ingersoll Rand has been doing relatively well. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Ingersoll Rand

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Ingersoll Rand would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a decent 12% gain to the company's bottom line. Pleasingly, EPS has also lifted 87% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 23% each year during the coming three years according to the analysts following the company. With the market only predicted to deliver 11% per year, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Ingersoll Rand's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Ingersoll Rand maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Many other vital risk factors can be found on the company's balance sheet. Our free balance sheet analysis for Ingersoll Rand with six simple checks will allow you to discover any risks that could be an issue.

Of course, you might also be able to find a better stock than Ingersoll Rand. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:IR

Ingersoll Rand

Provides various mission-critical air, gas, liquid, and solid flow creation technologies services and solutions worldwide.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives