Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:GWW

How Investors Are Reacting To W.W. Grainger (GWW) Beating EPS Estimates While Reaffirming Guidance

Simply Wall St

Reviewed by Sasha Jovanovic

- In the past quarter, W.W. Grainger reported adjusted EPS of US$10.21, surpassing Wall Street expectations on the back of firm pricing and tight cost control, while reaffirming full-year guidance for adjusted EPS of US$39–US$39.75 and revenue of US$17.80–US$18.00 billion.

- This combination of an earnings beat and unchanged guidance, despite ongoing macroeconomic headwinds, highlights management’s confidence in the company’s operational resilience and pricing discipline.

- Next, we’ll examine how this earnings beat and reaffirmed full-year guidance may influence Grainger’s investment narrative and future expectations.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

W.W. Grainger Investment Narrative Recap

To own Grainger, you need to believe that steady MRO demand, strong pricing power and efficient distribution can support durable earnings, even when industrial activity is muted. The latest earnings beat and reaffirmed guidance do not materially change the near term picture, but they reinforce the current catalyst around operational resilience while leaving the key risk of margin pressure from tariffs, LIFO impacts and pricing intensity very much in focus.

Against that backdrop, the board’s recent decision to lift the quarterly dividend to US$2.26 per share, and then keep it unchanged in subsequent quarters, ties directly into the catalyst of consistent free cash flow supporting shareholder returns. It signals an ongoing willingness to return cash even as the company invests in automation and digital capabilities, which could become more important if MRO demand stays softer for longer or competitive pricing tightens.

However, behind this steady guidance and dividend track, there is an important margin related risk that investors should be aware of...

Read the full narrative on W.W. Grainger (it's free!)

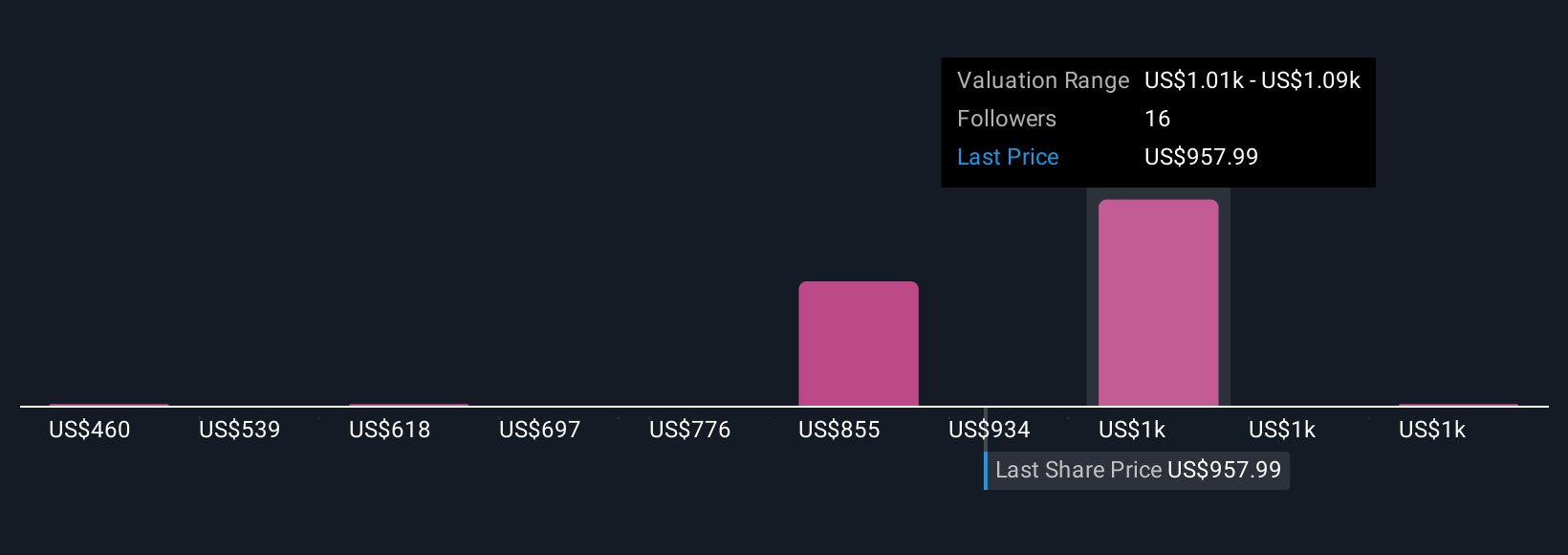

W.W. Grainger's narrative projects $21.3 billion revenue and $2.3 billion earnings by 2028. This requires 6.7% yearly revenue growth and an earnings increase of about $0.4 billion from $1.9 billion today.

Uncover how W.W. Grainger's forecasts yield a $1055 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently see Grainger’s fair value between about US$939 and US$1,250, underlining how far opinions can stretch. Set that against ongoing concerns around tariff and LIFO driven margin pressure, and you can see why it pays to compare several different views on how resilient Grainger’s profitability might really be.

Explore 3 other fair value estimates on W.W. Grainger - why the stock might be worth as much as 28% more than the current price!

Build Your Own W.W. Grainger Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your W.W. Grainger research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free W.W. Grainger research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W.W. Grainger's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if W.W. Grainger might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GWW

W.W. Grainger

Distributes maintenance, repair, and operating products and services primarily in North America, Japan, and the United Kingdom.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

60 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

60 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative