- United States

- /

- Aerospace & Defense

- /

- NYSE:GD

Does General Dynamics (NYSE:GD) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that General Dynamics Corporation (NYSE:GD) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for General Dynamics

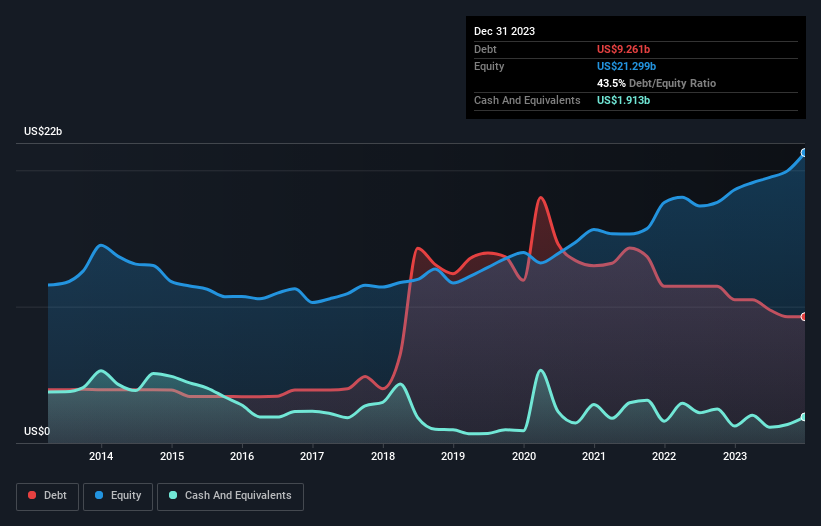

What Is General Dynamics's Net Debt?

The image below, which you can click on for greater detail, shows that General Dynamics had debt of US$9.26b at the end of December 2023, a reduction from US$10.5b over a year. However, because it has a cash reserve of US$1.91b, its net debt is less, at about US$7.35b.

A Look At General Dynamics' Liabilities

Zooming in on the latest balance sheet data, we can see that General Dynamics had liabilities of US$16.4b due within 12 months and liabilities of US$17.1b due beyond that. Offsetting these obligations, it had cash of US$1.91b as well as receivables valued at US$11.0b due within 12 months. So its liabilities total US$20.6b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since General Dynamics has a huge market capitalization of US$74.9b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

We'd say that General Dynamics's moderate net debt to EBITDA ratio ( being 1.6), indicates prudence when it comes to debt. And its commanding EBIT of 10.8 times its interest expense, implies the debt load is as light as a peacock feather. On the other hand, General Dynamics's EBIT dived 19%, over the last year. If that rate of decline in earnings continues, the company could find itself in a tight spot. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine General Dynamics's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, General Dynamics generated free cash flow amounting to a very robust 84% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

Both General Dynamics's ability to to convert EBIT to free cash flow and its interest cover gave us comfort that it can handle its debt. But truth be told its EBIT growth rate had us nibbling our nails. Considering this range of data points, we think General Dynamics is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. We'd be motivated to research the stock further if we found out that General Dynamics insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:GD

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Community Narratives