Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:CW

Curtiss-Wright (CW): Assessing Valuation Following Major Share Buyback Expansion

Simply Wall St

Reviewed by Simply Wall St

Curtiss-Wright (CW) has announced a substantial increase to its share buyback authorization, adding $416 million and lifting the total authorization above $2 billion. This move demonstrates confidence in its financial position and outlook.

See our latest analysis for Curtiss-Wright.

Alongside this substantial buyback increase, Curtiss-Wright’s stock has attracted attention for its persistent momentum, with a year-to-date share price return of over 52% and a 12-month total shareholder return of nearly 45%. Recent announcements, including a steady quarterly dividend and participation in key industry conferences, have reinforced investor confidence in both the company’s strategy and its long-term growth profile.

If developments like these have you interested in the broader aerospace and defense sector, take a moment to explore See the full list for free..

With shares soaring over 50% this year, analysts and investors alike are considering whether Curtiss-Wright is trading below its true value or if the market is already accounting for all its future growth.

Most Popular Narrative: 11.9% Undervalued

With the most closely watched narrative assigning Curtiss-Wright a fair value of $608, well above the last close of $536, there is a sizable gap between the current price and what consensus sees as justified by the fundamentals.

Surging global defense budgets, increased geopolitical tensions, and a potential expansion of NATO's spend target from 2% to 5% of GDP are fueling strong multi-year demand for Curtiss-Wright's defense systems, including embedded computing, mission-critical electronics, and platform content. Management expects 20% growth in direct foreign military sales for 2025 and a visible international pipeline, positioning the company for sustained revenue and earnings expansion.

Curious why analysts think this growth trajectory demands a market re-rating? There is a key projection about Curtiss-Wright’s ability to capture explosive sector gains, with numbers that could surprise even seasoned investors. Find out what future targets drive this bullish narrative and if the company’s next act will break out of the pack.

Result: Fair Value of $608 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rapid advances in digital defense tech or delays in nuclear projects could challenge Curtiss-Wright’s path and pressure its projected growth rates.

Find out about the key risks to this Curtiss-Wright narrative.

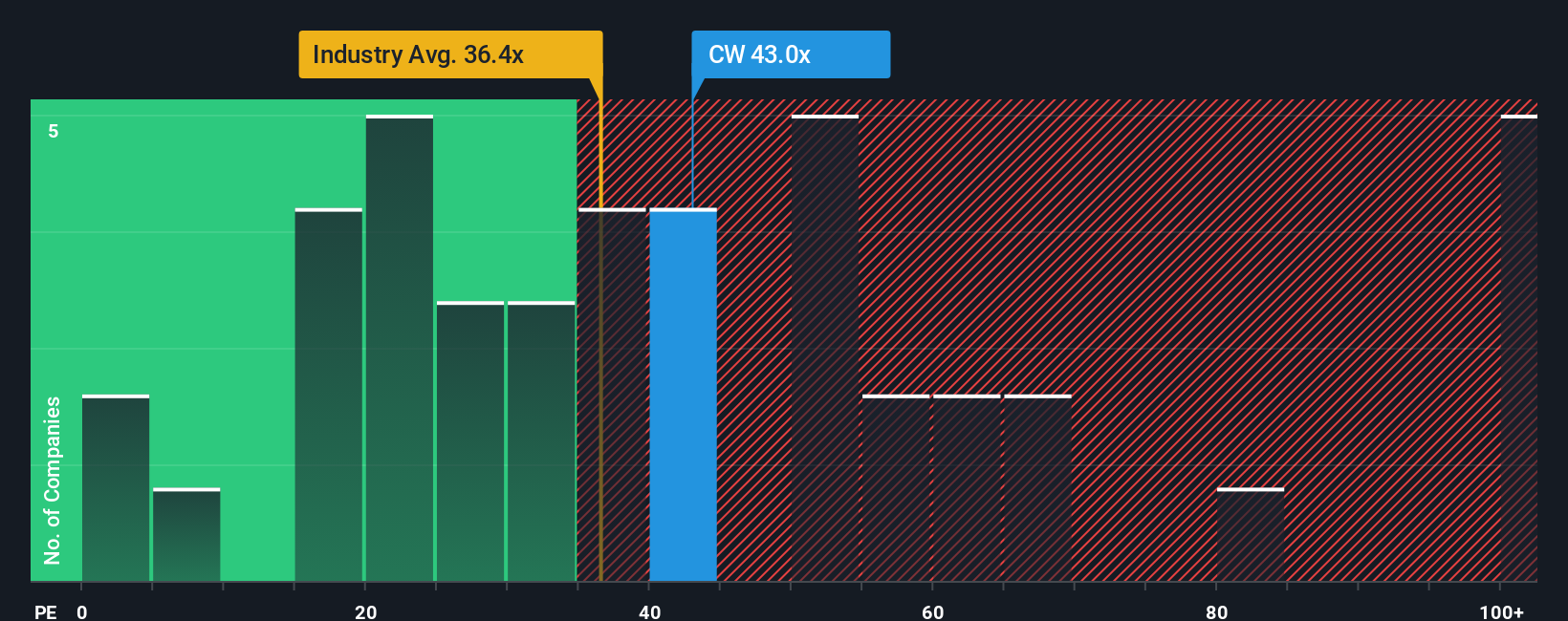

Another View: Looking at Price-to-Earnings Ratios

While some narratives see Curtiss-Wright as undervalued relative to their growth outlook, the current price-to-earnings ratio tells a different story. At 42.5x, the shares trade above the US Aerospace & Defense industry average of 35.4x and the fair ratio of 27x. This suggests investors may be paying a steep premium. Should this gap concern those seeking more value going forward?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Curtiss-Wright Narrative

If you see things differently, or want to chart your own perspective, you can quickly build your own narrative using our tools in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Curtiss-Wright.

Looking for More Investment Ideas?

Some of the most compelling investment opportunities might be just outside your radar. Don’t get left behind and let your next great find come from a fresh perspective.

- Capitalize on high yields and stable income by tapping into these 17 dividend stocks with yields > 3% with returns above 3% and strong track records.

- Jump ahead of the curve with these 25 AI penny stocks, identifying companies driving artificial intelligence breakthroughs and future-proofing your portfolio.

- Spot hidden gems by assessing these 919 undervalued stocks based on cash flows that the market has yet to fully appreciate for their true potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CW

Curtiss-Wright

Provides engineered products, solutions, and services mainly to aerospace and defense, commercial power, process, and industrial markets worldwide.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative