Advertisement

- United States

- /

- Building

- /

- NYSE:BLDR

Assessing Builders FirstSource (BLDR) Valuation After Recent Share Price Momentum

Why Builders FirstSource Is On Investors’ Radar Today

Builders FirstSource (BLDR) is drawing fresh attention after recent trading, with the share price at $126.38 and returns over the past month, past 3 months, and year giving investors new performance context.

See our latest analysis for Builders FirstSource.

For context, Builders FirstSource has seen strong near term momentum, with a 7 day share price return of 20.30% and a 30 day share price return of 20.75%. The 1 year total shareholder return shows a 21.77% decline, which contrasts with cumulative three and five year total shareholder returns of 76.29% and 204.75%. Recent strength therefore follows a much weaker year, but still sits on top of solid longer term gains.

If this kind of move has you thinking about what else is out there, it could be a good moment to broaden your search with fast growing stocks with high insider ownership.

With Builders FirstSource trading at $126.38, a small 3% discount to the average analyst price target and an intrinsic value estimate that sits about 19% above the market, you have to ask: is this a genuine opportunity, or is the market already baking in future growth?

Most Popular Narrative: 4.6% Undervalued

Based on the most followed narrative, Builders FirstSource’s fair value of about $132.52 sits a little above the recent close at $126.38, which puts the spotlight on how that gap is justified.

The analysts have a consensus price target of $140.316 for Builders FirstSource based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $158.0, and the most bearish reporting a price target of just $125.0.

Curious what sits behind that fair value call? Revenue that edges higher, margins that settle at a new level, and a future earnings multiple that has to work hard. The full narrative ties those moving parts together in a detailed earnings path and valuation bridge.

Result: Fair Value of $132.52 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, it is worth keeping in mind that prolonged housing softness and ongoing pricing pressure in a competitive market could undercut both the margin story and recovery expectations.

Find out about the key risks to this Builders FirstSource narrative.

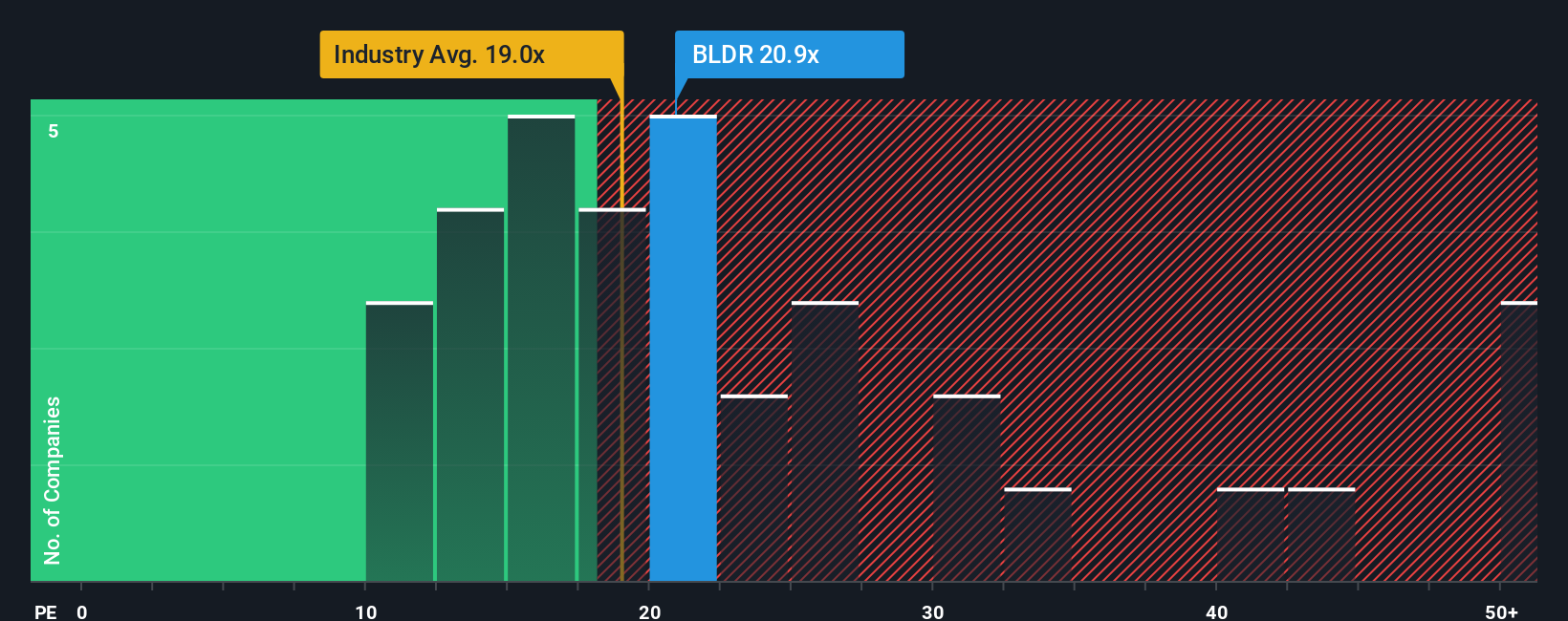

Another View On Builders FirstSource’s Valuation

The fair value narrative suggests Builders FirstSource is modestly undervalued, but the market’s preferred yardstick tells a different story. On a P/E of 23.5x, the shares are pricier than both the US Building industry at 21.8x and peers at 20.6x, even though the fair ratio points to 26.7x as a level the market could move toward. That gap leaves you weighing whether you see more risk of sentiment cooling toward the sector or the market leaning in closer to that higher fair ratio.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Builders FirstSource Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to shape the story yourself, you can build a fresh view in just a few minutes with Do it your way.

A great starting point for your Builders FirstSource research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one stock, you could miss other opportunities that fit you even better, so use this moment to scan the market with purpose.

- Spot potential value plays early by running your filters across these 886 undervalued stocks based on cash flows that might be trading below what their cash flows suggest.

- Zero in on income opportunities by checking out these 12 dividend stocks with yields > 3% that may suit a portfolio focused on regular payouts.

- Get exposure to a fast evolving theme by reviewing these 80 cryptocurrency and blockchain stocks that are tied to blockchain and digital asset trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Builders FirstSource might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BLDR

Builders FirstSource

Provides building materials for professional builders in new residential construction and repair, and remodeling in the United States.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

75 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

66 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Abitibi Metals ·

Abitibi Metals’ High-Grade B26 Polymetallic Deposit Trading at a Fraction of Peers, 96% Undervalued?

Fair Value:CA$1.2950.4% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

EV

everyseed on Zylox-Tonbridge Medical Technology ·

Zylox-Tonbridge: Early Signs of an Emerging Global Vascular Intervention Platform

Fair Value:HK$30.8539.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

Anthony_Lee on Geohan Corporation Berhad ·

Geohan's Growth Outlook Brightens on Expanding Order Book and Easing Cost Pressures

Fair Value:RM 0.7460.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

75 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative