Advertisement

- United States

- /

- Machinery

- /

- NasdaqGS:TWIN

Twin Disc, Incorporated's (NASDAQ:TWIN) CEO Looks Like They Deserve Their Pay Packet

Key Insights

- Twin Disc to hold its Annual General Meeting on 26th of October

- Salary of US$648.4k is part of CEO John Batten's total remuneration

- The total compensation is similar to the average for the industry

- Twin Disc's total shareholder return over the past three years was 148% while its EPS grew by 91% over the past three years

We have been pretty impressed with the performance at Twin Disc, Incorporated (NASDAQ:TWIN) recently and CEO John Batten deserves a mention for their role in it. Shareholders will have this at the front of their minds in the upcoming AGM on 26th of October. The focus will probably be on the future company strategy as shareholders cast their votes on resolutions such as executive remuneration and other matters. We think the CEO has done a pretty decent job and we discuss why the CEO compensation is appropriate.

View our latest analysis for Twin Disc

How Does Total Compensation For John Batten Compare With Other Companies In The Industry?

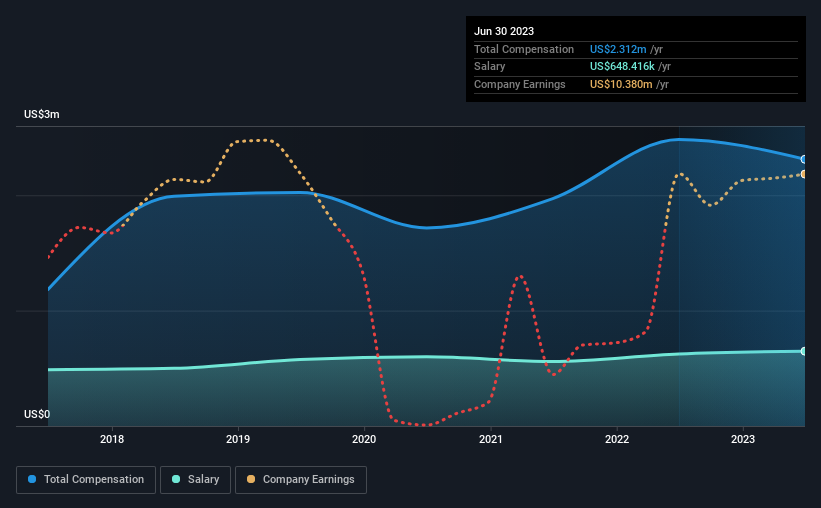

At the time of writing, our data shows that Twin Disc, Incorporated has a market capitalization of US$187m, and reported total annual CEO compensation of US$2.3m for the year to June 2023. That's slightly lower by 6.9% over the previous year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$648k.

On comparing similar companies from the American Machinery industry with market caps ranging from US$100m to US$400m, we found that the median CEO total compensation was US$2.1m. This suggests that Twin Disc remunerates its CEO largely in line with the industry average. Furthermore, John Batten directly owns US$34m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$648k | US$624k | 28% |

| Other | US$1.7m | US$1.9m | 72% |

| Total Compensation | US$2.3m | US$2.5m | 100% |

Talking in terms of the industry, salary represented approximately 16% of total compensation out of all the companies we analyzed, while other remuneration made up 84% of the pie. It's interesting to note that Twin Disc pays out a greater portion of remuneration through salary, compared to the industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Twin Disc, Incorporated's Growth Numbers

Over the past three years, Twin Disc, Incorporated has seen its earnings per share (EPS) grow by 91% per year. It achieved revenue growth of 14% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. This sort of respectable year-on-year revenue growth is often seen at a healthy, growing business. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Twin Disc, Incorporated Been A Good Investment?

Most shareholders would probably be pleased with Twin Disc, Incorporated for providing a total return of 148% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Given the company's decent performance, the CEO remuneration policy might not be shareholders' central point of focus in the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Twin Disc that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Twin Disc might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TWIN

Twin Disc

Engages in the design, manufacture, and sale of marine and heavy duty off-highway power transmission equipment in the United States, the Netherlands, China, Australia, Italy, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor