Legence (LGN) shares have been showing upward momentum lately, climbing over 10% in the past month. Investors are taking note as the company reports annual revenue growth above 10% along with a significant swing in net income.

Legence’s 1-month share price return of 14% highlights building momentum, especially with a year-to-date gain now sitting at 18%. This upward shift signals a renewed sense of optimism around the company as investors respond to recent growth and operational progress.

With shares rallying and growth metrics on the rise, the key question now is whether Legence is trading at a bargain or if the market has already factored in its future potential, which could leave little room for upside.

Advertisement

Price-to-Sales of 1x: Is it justified?

Legence is currently valued at a price-to-sales ratio of 1x, which places its valuation beneath both its industry and peer averages. With a last close price of $36.12 and peers commanding higher sales multiples, the company looks attractively priced based on revenue.

The price-to-sales (P/S) ratio measures how much investors are willing to pay per dollar of sales. This is a particularly useful metric for companies that are unprofitable, like Legence. In cyclical sectors such as construction, revenue-based multiples can reveal relative market optimism or skepticism where earnings are volatile or negative.

For Legence, the 1x P/S ratio stands out against the US Construction industry average of 1.4x and the peer group’s average of 2x. This direct comparison with the sector shows the market is discounting Legence's shares more heavily than those of its competitors, possibly leaving room for revaluation if performance improves.

However, sustained net losses and ongoing sector volatility remain key risks. These factors could quickly reverse current optimism if not addressed in upcoming quarters.

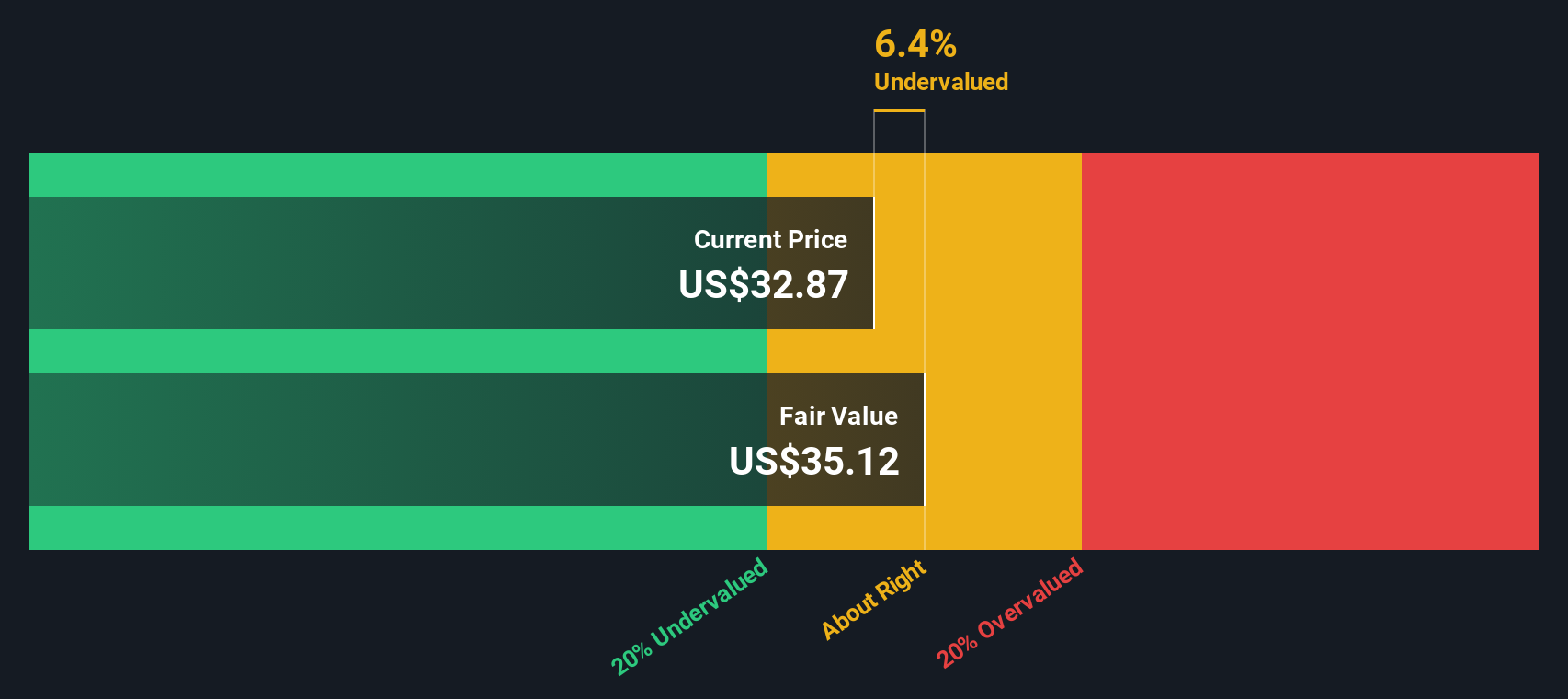

While Legence’s current share price trades below peers based on sales, our DCF model points to a different story. According to this method, Legence’s recent price of $36.12 sits slightly above our fair value estimate of $35.04, which suggests the market may be pricing in more optimism than fundamentals support.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Legence for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Legence Narrative

If you have a different take or want to dig into the numbers yourself, you can easily build your own perspective on Legence in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Legence.

Looking for more investment ideas?

Don't let fresh opportunities pass you by. Experience the power of the Simply Wall Street Screener and get ahead with original stock ideas tailored for forward-thinking investors.

Capture the explosive growth potential in artificial intelligence by starting with these 27 AI penny stocks. See which companies are making real breakthroughs in this transformative sector.

Maximize your portfolio’s income stream by securing steady returns through these 17 dividend stocks with yields > 3%, which features companies committed to rewarding shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies