- United States

- /

- Oil and Gas

- /

- NYSE:TXO

Top US Growth Stocks With High Insider Ownership For September 2024

Reviewed by Simply Wall St

As the Dow Jones Industrial Average hits a record high and the Nasdaq Composite faces pressure from declining chip stocks, investors are closely monitoring market dynamics influenced by inflation data and Federal Reserve rate decisions. In this environment, growth companies with high insider ownership can offer unique advantages, as insiders' significant stakes often align their interests with those of shareholders, potentially driving long-term value.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 24.3% |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.2% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 32.3% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

| Hims & Hers Health (NYSE:HIMS) | 13.8% | 40.7% |

| On Holding (NYSE:ONON) | 28.4% | 24.2% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.1% | 95% |

| BBB Foods (NYSE:TBBB) | 22.9% | 51.2% |

| Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

Let's dive into some prime choices out of the screener.

AerSale (NasdaqCM:ASLE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: AerSale Corporation, with a market cap of $265.50 million, supplies aftermarket commercial aircraft, engines, and parts to various aviation sectors including airlines, leasing companies, OEMs, and government contractors globally.

Operations: AerSale's revenue segments include Tech Ops - MRO Services ($102.33 million), Tech Ops - Product Sales ($21.49 million), Asset Management Solutions - Engine ($161.35 million), and Asset Management Solutions - Aircraft ($69.38 million).

Insider Ownership: 24.1%

Earnings Growth Forecast: 140% p.a.

AerSale has shown significant insider buying over the past three months, indicating strong internal confidence. Despite recent drops from several Russell 2000 indices, the company reported a year-over-year revenue increase to US$77.1 million for Q2 2024 and forecasts annual profit growth above market averages. Analysts predict a 63.1% rise in stock price, and earnings are expected to grow by over 140% annually, with profitability anticipated within three years.

- Click to explore a detailed breakdown of our findings in AerSale's earnings growth report.

- According our valuation report, there's an indication that AerSale's share price might be on the cheaper side.

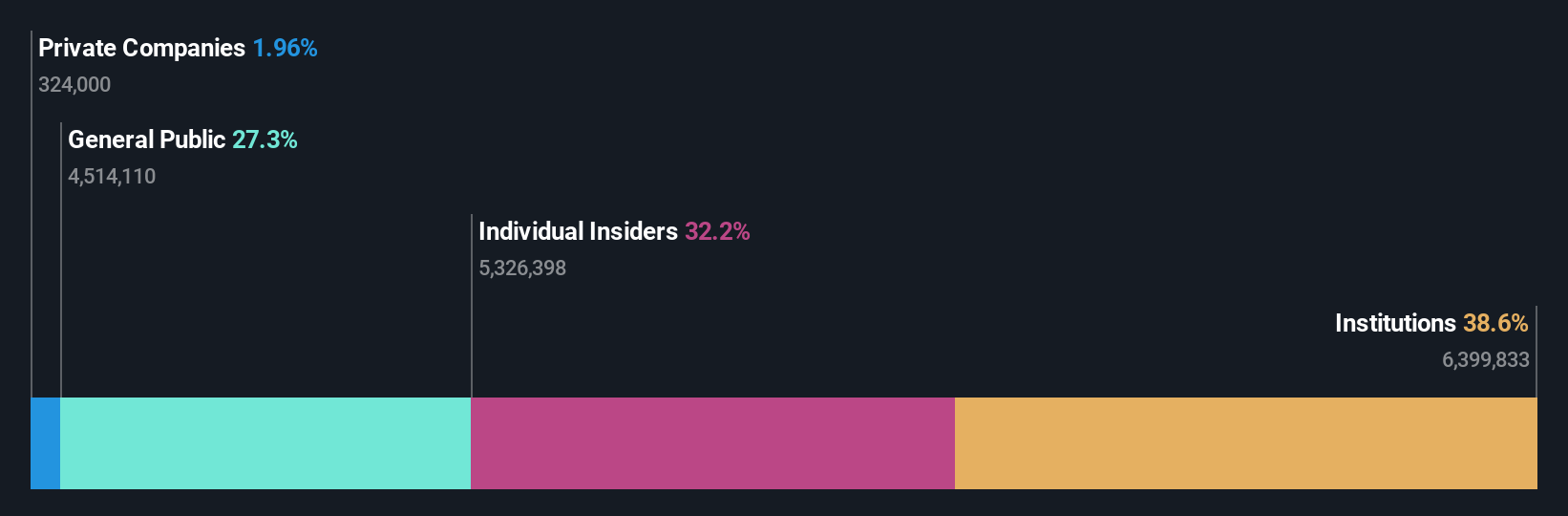

Capital Bancorp (NasdaqGS:CBNK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Capital Bancorp, Inc. operates as the bank holding company for Capital Bank, N.A., with a market cap of $348.38 million.

Operations: Capital Bancorp's revenue segments include Opensky ($70.71 million), Corporate ($2.74 million), Commercial Bank ($78.21 million), and Capital Bank Home Loans (CBHL) ($5.84 million).

Insider Ownership: 35%

Earnings Growth Forecast: 33.6% p.a.

Capital Bancorp has demonstrated strong insider confidence with no substantial insider selling in the past three months. The company is trading at a significant discount to its estimated fair value and relative to peers. Recent earnings reports show net income growth, with Q2 2024 net interest income rising to US$37.06 million from US$35.34 million a year ago. Analysts forecast annual profit growth of 33.6% and revenue growth of 26.7%, both outpacing market averages, despite an unstable dividend track record and recent executive changes including a new CFO appointment in July 2024.

- Get an in-depth perspective on Capital Bancorp's performance by reading our analyst estimates report here.

- In light of our recent valuation report, it seems possible that Capital Bancorp is trading behind its estimated value.

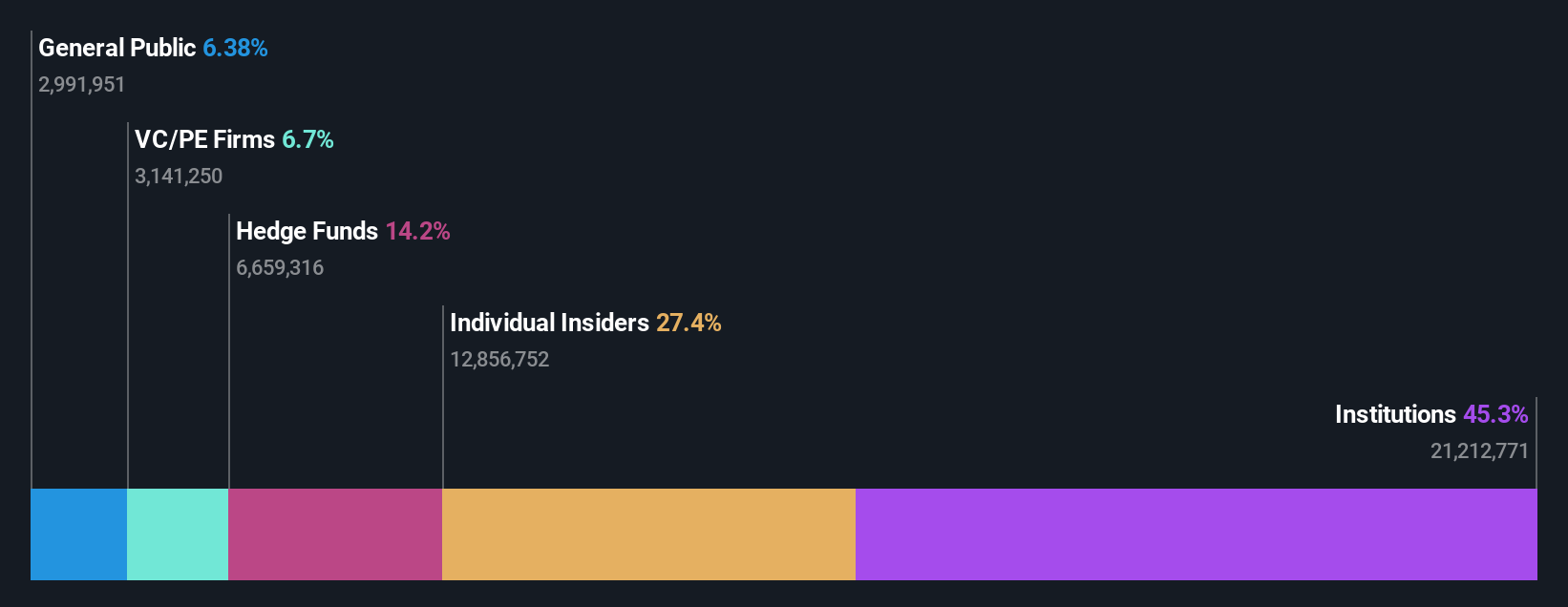

TXO Partners (NYSE:TXO)

Simply Wall St Growth Rating: ★★★★★☆

Overview: TXO Partners, L.P. is an oil and natural gas company that focuses on acquiring, developing, optimizing, and exploiting conventional oil, natural gas, and natural gas liquid reserves in North America with a market cap of $717.18 million.

Operations: The company's revenue segment is primarily derived from the exploration and production of oil, natural gas, and natural gas liquids, totaling $286.59 million.

Insider Ownership: 25.2%

Earnings Growth Forecast: 147.1% p.a.

TXO Partners has seen substantial insider buying over the past three months, indicating strong insider confidence. Despite a decrease in revenue and net income for the first half of 2024, TXO is forecast to achieve high annual revenue growth of 23.4% and significant earnings growth of 147.14%. However, its dividend yield of 11.25% is not well covered by earnings or free cash flows. The company trades at a significant discount to its estimated fair value.

- Delve into the full analysis future growth report here for a deeper understanding of TXO Partners.

- Our valuation report here indicates TXO Partners may be undervalued.

Where To Now?

- Click here to access our complete index of 181 Fast Growing US Companies With High Insider Ownership.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if TXO Partners might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TXO

TXO Partners

An oil and natural gas company, focuses on the acquisition, development, optimization, and exploitation of conventional oil, natural gas, and natural gas liquid reserves in North America.

Reasonable growth potential and fair value.