- United States

- /

- Banks

- /

- OTCPK:SOME

Somerset Trust Holding (SOME) Margin Gains Challenge Value Discount Narrative

Reviewed by Simply Wall St

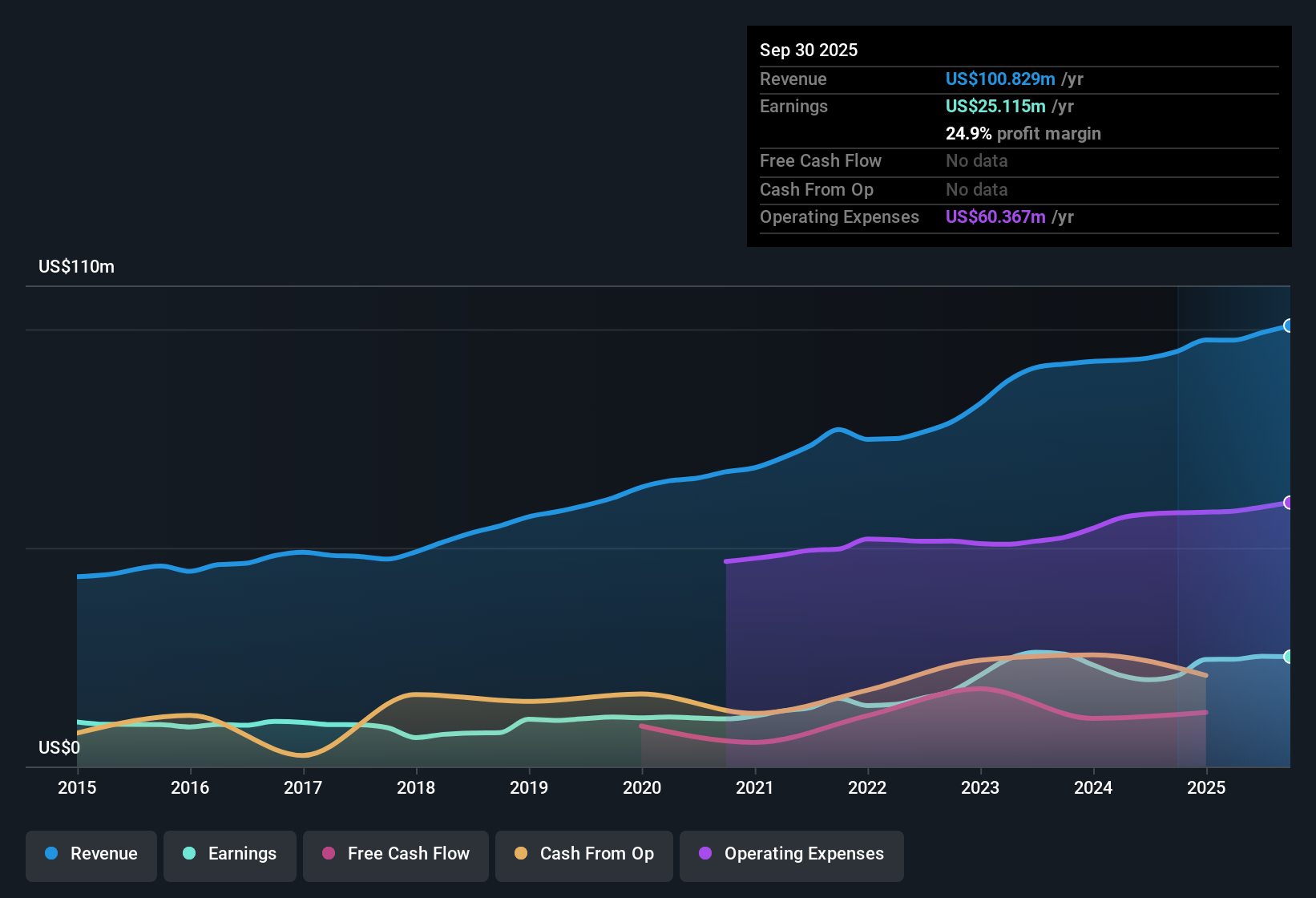

Somerset Trust Holding (SOME) turned in a strong performance this year, with net profit margins pushing up to 24.9% from last year’s 21.9% and a standout 20.8% earnings growth, well above the company’s five-year average of 15.3%. With shares trading at $63, a substantial discount to an estimated fair value of $154.11, and a price-to-earnings ratio of just 6.3x compared to peers, the valuation picture looks particularly attractive. Investors will be encouraged by the acceleration in earnings momentum and a balance of rewards highlighted by profitability, growth, and a healthy dividend.

See our full analysis for Somerset Trust Holding.Next, we’ll see how these numbers compare to the key narratives and expectations held by the Simply Wall St community, and whether the headlines live up to the story.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Broaden to 24.9% With Quality Growth

- Profitability improved as net profit margins reached 24.9%, expanding from 21.9% last year. This level also outpaces the five-year trend of 15.3% average annual earnings growth.

- Earnings momentum, shown by the recent 20.8% growth rate, highlights a pattern of stable performance and resilience that investors are now rewarding more than in previous years.

- In market coverage, stability and steady operations are emphasized as reasons for seeing Somerset as a promising option among conservative regional banks.

- Analysts note that these improvements suggest prudent management is turning into real value for shareholders, not just a short-term boost.

Price-to-Earnings Still Undercuts Industry and Peers

- The company is now trading at a 6.3x price-to-earnings ratio, versus the US Banks industry average of 11.1x and peer average of 12.5x. This signals a possible discount versus comparable stocks.

- The prevailing analysis points to the market overlooking Somerset’s earnings quality, since basic multiples hint it is undervalued for the level of profit and momentum it is delivering.

- With shares at $63 but DCF fair value at $154.11, there is a notable gap suggesting upside if the market recognizes this performance.

- Commentary from sector-watchers describes similar banks attracting premiums as conditions favor balance-sheet strength and profitability. This deepens the perceived disconnect here.

No Confirmed Risks Tilts Rewards Balance

- No new risks with confirmed outcomes appear in recent filings or data. Key rewards now include an attractive valuation, an appealing dividend, and clear profit or revenue growth.

- The combination of strong margins, undervalued share price, and positive profit momentum heavily supports the positive investment case currently taking shape.

- Analysts project that the tilt towards rewards over risks makes the stock an appealing watchlist candidate as investors refocus on steady, value-rich regionals.

- Continued outperformance on basic metrics could drive renewed investor attention, especially if the market environment remains risk-averse.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Somerset Trust Holding's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite strengths in earnings growth and valuation, Somerset Trust’s limited market recognition could indicate missed potential for steady growth across different business cycles.

If you want stocks where consistency is more visible, use stable growth stocks screener (2097 results) to zero in on companies whose revenue and earnings hold firm no matter the environment.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OTCPK:SOME

Somerset Trust Holding

Operates as the bank holding company for Somerset Trust Company that provides banking products and services in Pennsylvania.

Solid track record with excellent balance sheet and pays a dividend.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion