Park National (PRK) has caught the eye of some investors recently, as returns have trended lower over the month with the stock down 5%. Its longer-term track record, however, remains a point of interest.

The recent 5% dip in Park National’s share price over the past month comes after a period of quiet for the company, but the bigger story is in the numbers. While 2024 has started with softer momentum, Park’s 3-year total shareholder return is up 17.6% and the 5-year figure stands near 98%, highlighting the real long-term value that patient investors have seen.

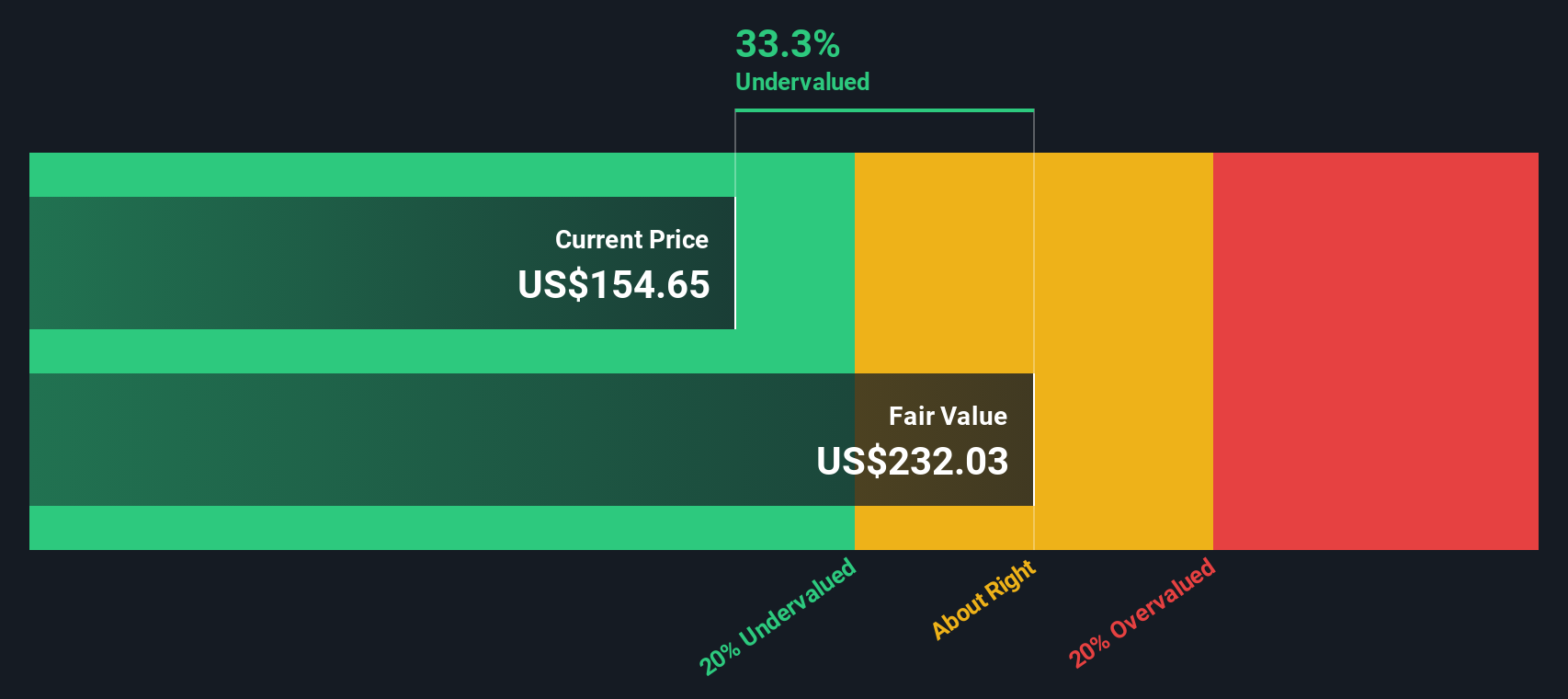

With shares trading at a discount to analyst targets and recent growth figures still positive, the big question is whether Park National is currently undervalued or if the market has already factored in all future gains.

Advertisement

Price-to-Earnings of 15.1x: Is it justified?

With Park National’s shares last closing at $157.31, the price-to-earnings (P/E) ratio stands at 15.1x, putting the stock at a premium relative to its industry. Compared to peers and the broader US Bank sector, this higher multiple sets a high bar for continuing growth.

The P/E ratio measures what investors are willing to pay today for each dollar of company earnings and is widely used to value banks and financial stocks. For Park National, a P/E of 15.1 implies the market is expecting above-average profitability or growth prospects from the company, which may or may not match reality depending on future performance.

The company’s 15.1x P/E is well above both the US Banks industry average at 11.2x and the peer group’s average at 13x. This suggests the market is pricing in greater earnings potential or stability for Park National relative to its rivals. However, regression analysis indicates the fair price-to-earnings ratio should be closer to 11.5x, spotlighting a significant premium. If investor sentiment shifts, there is room for this multiple to compress toward that fair level.

However, slipping annual revenue growth and declining year-to-date total return remain key risks that could pressure Park National’s valuation if momentum does not improve.

Another View: Discounted Cash Flow Tells a Different Story

While a higher price-to-earnings ratio suggests Park National is expensive compared to its industry, our DCF model offers a different perspective. According to this method, the stock trades at a 31% discount to its fair value, which indicates it might be undervalued. Could the market be overlooking this?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Park National for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Park National Narrative

If you want a different take or trust your own approach, it’s easy to dive into the numbers and build your perspective in just minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Park National.

Looking for more investment ideas?

Staying ahead in today’s market means always being on the lookout for the next standout opportunity. Let Simply Wall Street’s powerful tools surface fresh options for your portfolio before they make headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Operates as the bank holding company for Park National Bank that provides commercial banking and trust services in small and medium population areas in the United States.