Advertisement

- United States

- /

- Banks

- /

- NYSE:WAL

Why Western Alliance Bancorporation (WAL) Is Up 7.3% After Fed Rate Cut Hopes Lift Regional Banks

Simply Wall St

Reviewed by Sasha Jovanovic

- Shares of Western Alliance Bancorporation recently moved higher after comments from New York Fed President John Williams suggested there is potential for a near-term interest rate cut, boosting market expectations for a December policy adjustment.

- This shift in interest rate outlook prompted broader positive sentiment for regional banks, reflecting how monetary policy expectations can quickly influence financial sector sentiment and outlook.

- We’ll now explore how the increased probability of a Federal Reserve rate cut could impact Western Alliance Bancorporation’s investment narrative.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Western Alliance Bancorporation Investment Narrative Recap

To be comfortable as a shareholder in Western Alliance Bancorporation, you need to believe in the company’s core strengths in commercial lending and its ability to capitalize on growth in fast-expanding Western and Sun Belt markets, while efficiently managing risk in its specialty verticals. The recent uptick in shares, driven by Federal Reserve rate cut optimism, has improved sentiment; however, this shift does not significantly alter the most important near-term catalyst, net interest margin recovery, or address the biggest risk linked to commercial real estate loan concentrations.

Among recent announcements, the company’s robust third-quarter earnings report stands out. With net income and earnings per share both higher year-over-year, this operational strength remains closely tied to interest rate expectations and ongoing loan performance, reinforcing the interplay between earnings resilience and the interest rate outlook as central to the stock’s short-term direction.

In contrast, it’s worth considering that rising optimism following Fed commentary could inadvertently distract from lingering risks in commercial real estate loan exposure that investors should be aware of...

Read the full narrative on Western Alliance Bancorporation (it's free!)

Western Alliance Bancorporation's narrative projects $4.4 billion revenue and $1.4 billion earnings by 2028. This requires 11.9% yearly revenue growth and a $566 million increase in earnings from $833.4 million today.

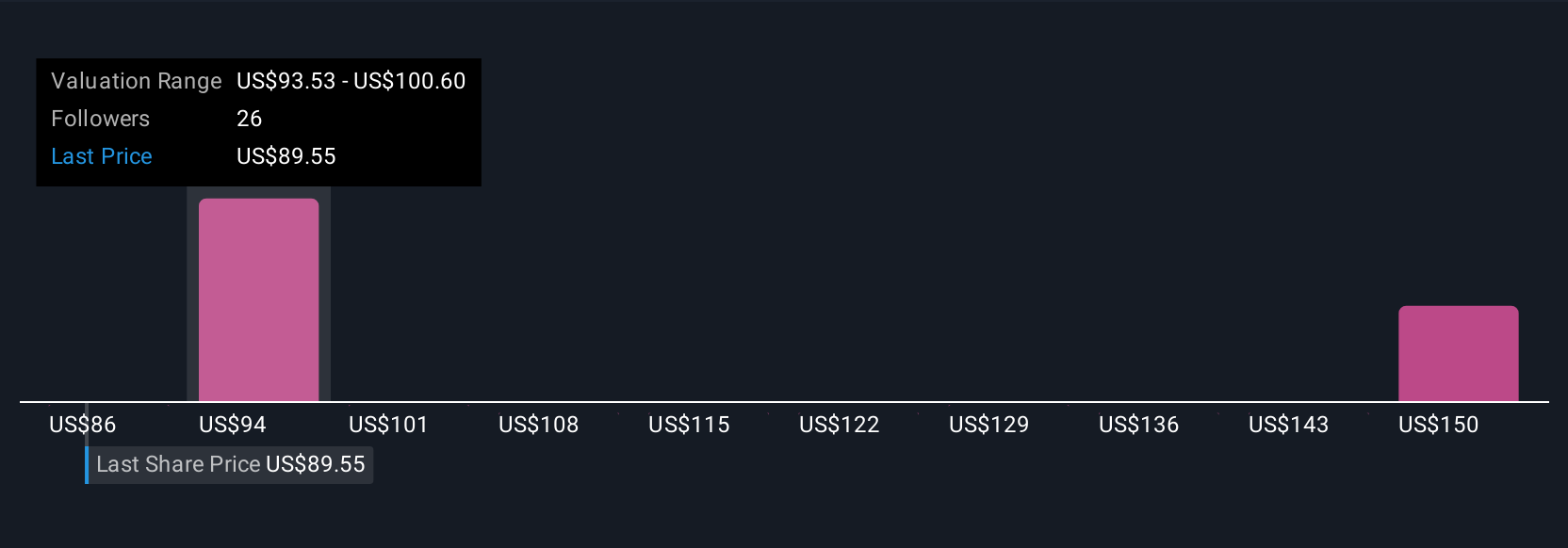

Uncover how Western Alliance Bancorporation's forecasts yield a $102.06 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Six different fair value estimates from the Simply Wall St Community range from US$96.06 to US$169.52 per share. While opinions on valuation differ widely, concerns remain about the bank’s exposure to commercial real estate loan risk and its influence on future results.

Explore 6 other fair value estimates on Western Alliance Bancorporation - why the stock might be worth over 2x more than the current price!

Build Your Own Western Alliance Bancorporation Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Western Alliance Bancorporation research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Western Alliance Bancorporation research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Western Alliance Bancorporation's overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Western Alliance Bancorporation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WAL

Western Alliance Bancorporation

Operates as the bank holding company for Western Alliance Bank that provides various banking products and related services primarily in Arizona, California, and Nevada.

Very undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor