- United States

- /

- Banks

- /

- NYSE:USB

U.S. Bancorp (NYSE:USB) Announces Expanded Embedded Payment Solutions For Businesses

Reviewed by Simply Wall St

U.S. Bancorp (NYSE:USB) recently launched an expanded suite of embedded payment solutions aimed at enhancing payment capabilities for businesses, marking a notable product development in its offerings. Over the last quarter, the company's share price was flat, reflecting broader market trends amid ongoing geopolitical developments in the Middle East and anticipation of the Federal Reserve's interest rate decisions. Despite the introduction of new financial services products and executive changes, the overall stock performance aligned with the market's stability, with no substantial deviation resulting from these corporate activities or the broader economic context.

Buy, Hold or Sell U.S. Bancorp? View our complete analysis and fair value estimate and you decide.

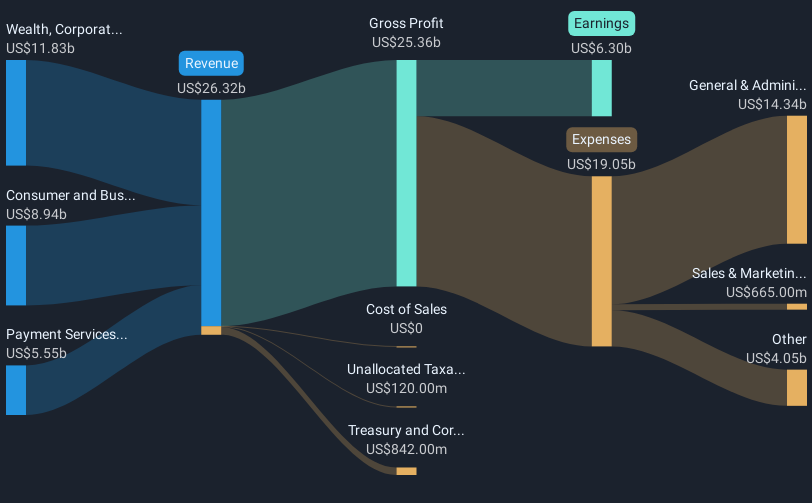

The recent expansion of U.S. Bancorp's embedded payment solutions, aiming to enhance payment capabilities for businesses, could be pivotal in shaping future revenue streams. By targeting affluent customer segments and boosting fee income, the company aligns its strategic focus on transforming digital payments and merchant acquiring. This could bolster future revenue growth and support earnings forecasts, notwithstanding the inherent risks associated with economic uncertainty and regulatory changes. Analysts have projected a revenue growth rate of 8.4% annually for the next three years, anticipating earnings to rise to US$7.5 billion by May 2028.

Over the last five years, U.S. Bancorp has delivered a total shareholder return of 37.20%, reflecting its ability to create value through share price appreciation and dividends. However, in the previous year, the company's 35% earnings growth did not translate into comparable share performance, as it underperformed the US Banks industry, which returned 21.9%. This highlights potential challenges in aligning operational success with market perceptions.

The current share price of US$40.98 suggests a 16.7% discount to the consensus analyst price target of US$49.18, indicating potential upside if future growth assumptions materialize. The company's focus on fee-generating business models and digital transformation could enhance profitability, aligning with analyst expectations of improved profit margins and earnings growth. Investors evaluating these assumptions should consider economic factors that could influence market conditions, potentially impacting U.S. Bancorp's financial outcomes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:USB

U.S. Bancorp

A financial services holding company, provides various financial services to individuals, businesses, institutional organizations, governmental entities, and other financial institutions in the United States.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Community Narratives