Advertisement

- United States

- /

- Banks

- /

- NYSE:TFIN

Will Triumph Financial’s (TFIN) New Buyback Offset Weaker Earnings in a Shifting Banking Landscape?

Simply Wall St

Reviewed by Sasha Jovanovic

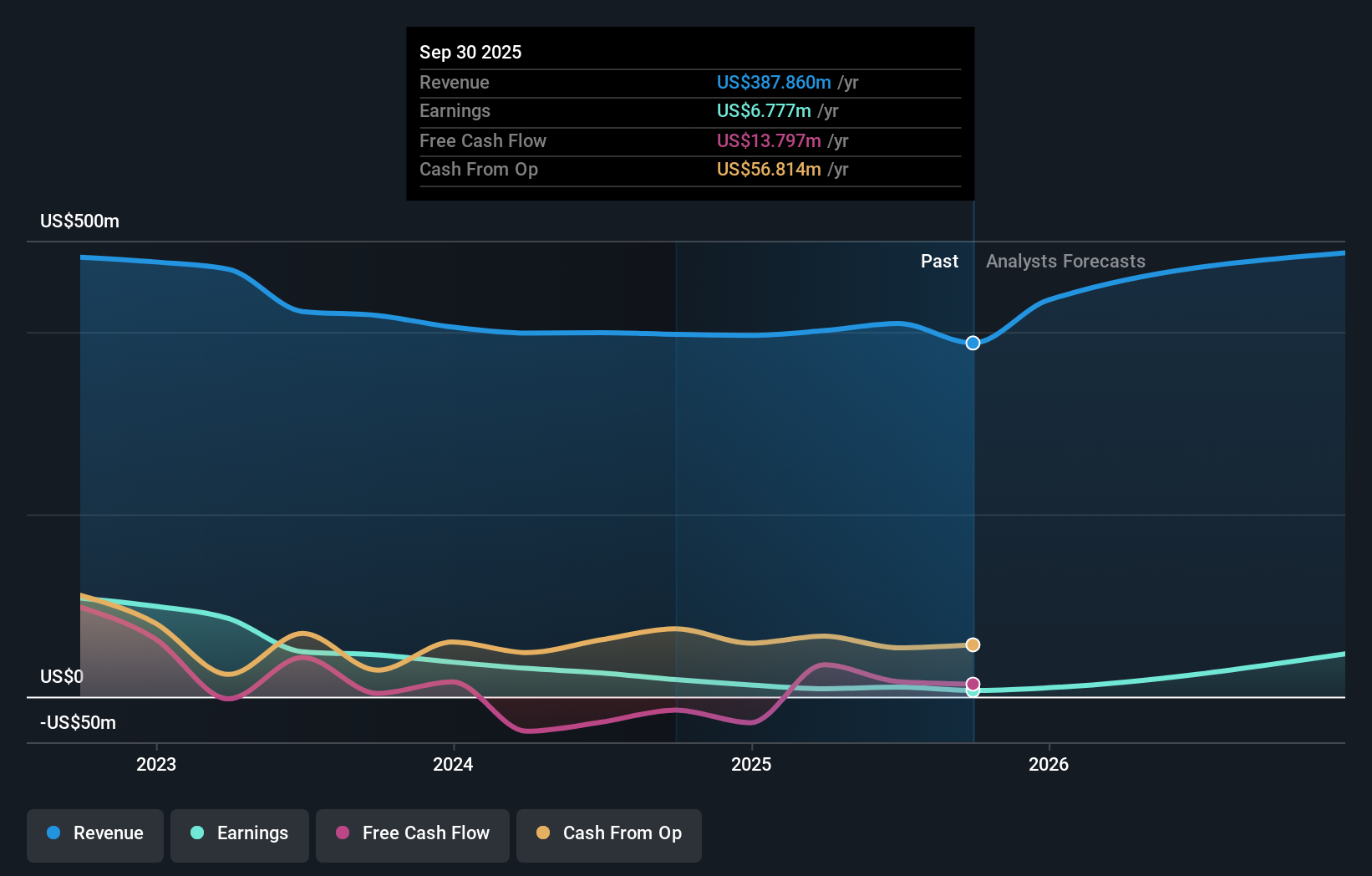

- In October 2025, Triumph Financial, Inc. reported third quarter earnings showing net interest income of US$87.83 million and net income of US$1.71 million, both down from the previous year, and announced a new one-year share repurchase program of up to US$30 million.

- This combination of modest earnings, continued buyback activity, and a backdrop of cooler inflation data shaped investor sentiment amid sector-wide shifts in regional banking.

- We'll examine how the recently announced US$30 million share repurchase program influences Triumph Financial's investment narrative and outlook.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Triumph Financial Investment Narrative Recap

For investors to be confident shareholders in Triumph Financial, they need to believe in the company's long-term strength in freight-focused financial services, while managing through near-term earnings volatility and competitive threats. The recent third-quarter results showed continued profit pressure, and while the announcement of a US$30 million share repurchase signals capital confidence, it does not significantly change the current short-term narrative: the key catalyst remains the ramp-up of Triumph's intelligence and payments segments, and the major risk continues to be freight cycle exposure.

The new share buyback program, valid for the next year, is the most relevant recent announcement. While it may offer some support to the share price, its effect is likely to be limited unless the company can demonstrate sustained improvement in its profit margins through further growth in its technology-led businesses.

However, investors should be mindful that concentrated exposure to freight and logistics clients could quickly amplify credit risks if...

Read the full narrative on Triumph Financial (it's free!)

Triumph Financial's outlook anticipates $602.4 million in revenue and $131.3 million in earnings by 2028. This is based on a 13.8% annual revenue growth rate and a jump in earnings from $10.4 million today to $131.3 million, an increase of approximately $120.9 million.

Uncover how Triumph Financial's forecasts yield a $60.50 fair value, in line with its current price.

Exploring Other Perspectives

Two individual fair value estimates from the Simply Wall St Community range widely, spanning US$13.71 to US$60.50 per share. Your view may differ, but keep in mind the ongoing risk of freight sector volatility shaping Triumph Financial’s performance.

Explore 2 other fair value estimates on Triumph Financial - why the stock might be worth as much as $60.50!

Build Your Own Triumph Financial Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Triumph Financial research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Triumph Financial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Triumph Financial's overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 27 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 34 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Triumph Financial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TFIN

Triumph Financial

A financial holding company, provides banking, factoring, payments, and intelligence services in the United States.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor