Advertisement

- United States

- /

- Banks

- /

- NYSE:SFBS

ServisFirst Bancshares (SFBS): Assessing Valuation After Q3 Revenue Miss Drives Investor Recalibration

Simply Wall St

Reviewed by Simply Wall St

ServisFirst Bancshares (SFBS) shares have come under pressure after the company’s third quarter revenue missed expectations by 7%. Although all regions remained profitable, investors reacted quickly to the earnings shortfall.

See our latest analysis for ServisFirst Bancshares.

The earnings disappointment has led to a sharp market reaction, with ServisFirst Bancshares’ share price falling 4.25% in a single day and extending its downward momentum. The stock is now down 18.39% year-to-date. Total shareholder return over the last twelve months sits at -25.92%, highlighting both the near-term volatility and the need for a longer-term perspective on performance, especially after years of solid gains.

If the market’s quick shift in sentiment has you reassessing your options, now could be the perfect time to broaden your search and discover fast growing stocks with high insider ownership

With ServisFirst Bancshares trading nearly 27% below average analyst price targets and showing strong profitability even as growth slows, investors have to ask: Is there real value here, or has the market fully accounted for future risks and rewards?

Most Popular Narrative: 21.3% Undervalued

With ServisFirst Bancshares’ fair value set at $86.67, which is over $18 above its last close, the most popular narrative points to significant upside for the stock based on underlying business drivers and outlook.

Expansion in key Southeastern markets and technology optimization support strong organic growth and sector-leading efficiency. This reinforces long-term earnings potential. Diversification through noninterest income initiatives and disciplined underwriting enhances profitability, resilience, and stability across market cycles.

Want to know the secret behind this bullish outlook? The fair value calculation hinges on ambitious assumptions for growth and profitability, as well as a specific discount rate that makes all the difference. Which aggressive financial projections are setting this price? Click to see the full narrative and discover what analysts are forecasting for ServisFirst Bancshares.

Result: Fair Value of $86.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing challenges in commercial real estate and rising credit costs could quickly undermine this bullish outlook if conditions worsen unexpectedly.

Find out about the key risks to this ServisFirst Bancshares narrative.

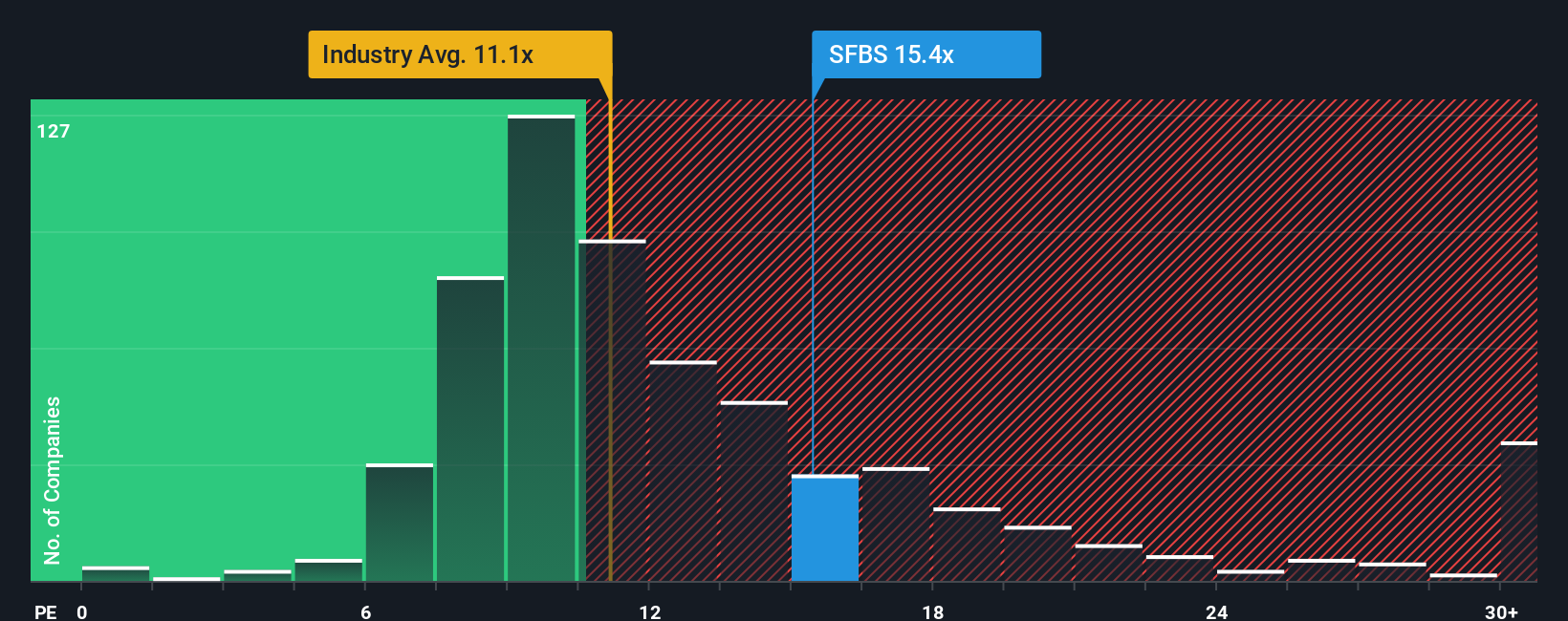

Another View: A Multiples-Based Reality Check

Looking beyond the fair value estimate, ServisFirst Bancshares is trading at a price-to-earnings ratio of 14.6x. This is more expensive than both the US Banks industry average of 11.2x and the market-implied fair ratio of 13.3x. Such a premium might signal investor optimism, or it may highlight valuation risk if the outlook falters. Is the market overlooking something, or pricing in too much?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own ServisFirst Bancshares Narrative

If you see things differently or want to conduct your own analysis, you can craft a personalized narrative in just a few minutes. Do it your way

A great starting point for your ServisFirst Bancshares research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never settle for just one opportunity. Widen your search with our powerful tools to catch the trends and stocks others are missing.

- Uncover potential big movers before the crowd with these 3584 penny stocks with strong financials, which brings robust financials to the table and shakes up expectations in the small-cap space.

- Capitalize on the next breakthrough in computing by pursuing these 26 quantum computing stocks, where rapid advancements could transform portfolios ahead of the mainstream.

- Strengthen your income stream by targeting these 18 dividend stocks with yields > 3%, which delivers consistent yields greater than 3% for reliable returns even in turbulent markets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SFBS

ServisFirst Bancshares

Operates as the bank holding company for ServisFirst Bank that provides various banking services to individual and corporate customers.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor