Advertisement

- United States

- /

- Banks

- /

- NYSE:NIC

Nicolet Bankshares (NIC): Valuation Insights Following Renewed Sector Optimism in Regional Banks

Simply Wall St

Reviewed by Kshitija Bhandaru

Nicolet Bankshares (NIC) gained attention as regional bank shares rallied, following upbeat earnings reports from major peers and signals from the Federal Reserve about a possible shift toward easier monetary policy. This news sparked fresh optimism across the sector.

See our latest analysis for Nicolet Bankshares.

This wave of optimism for regional banks has not erased recent volatility for Nicolet Bankshares. Its 21% year-to-date share price return remains impressive, despite a 2% dip over the past week and mild profit-taking in the last month. Looking beyond short-term moves, total shareholder returns of nearly 24% over the past year and more than 100% in five years suggest momentum is still building. Investors are continuing to weigh sector risks and the company’s upcoming earnings announcement.

If strong banking returns have you thinking bigger, it is the perfect time to broaden your investing horizons and discover fast growing stocks with high insider ownership

But with Nicolet Bankshares enjoying strong long-term returns and trading below analyst targets, investors may wonder whether the market is still underestimating its potential or if recent enthusiasm has already priced in the company’s future growth.

Price-to-Earnings of 13.7x: Is it justified?

Nicolet Bankshares is currently trading at a price-to-earnings (P/E) ratio of 13.7x, which puts it above key benchmarks and raises questions about market expectations for future growth. Despite positive recent momentum, investors should consider whether the premium attached to NIC’s earnings is warranted given industry dynamics and company performance.

The P/E ratio is a straightforward way to compare a company's market value to its earnings and is especially relevant for banks like NIC. Typically, a higher P/E reflects higher anticipated earnings growth or confidence in the business model.

However, Nicolet Bankshares trades at a more expensive multiple than both its US Banks peers (industry average 11.2x) and the peer group average (12.3x). Notably, its fair P/E ratio, based on regression analysis, is estimated to be 11.4x. This suggests the current valuation may be stretched if growth does not accelerate.

Explore the SWS fair ratio for Nicolet Bankshares

Result: Price-to-Earnings of 13.7x (OVERVALUED)

However, slowing revenue growth and recent share price volatility could challenge bullish expectations. This reminds investors that risks remain despite strong long-term returns.

Find out about the key risks to this Nicolet Bankshares narrative.

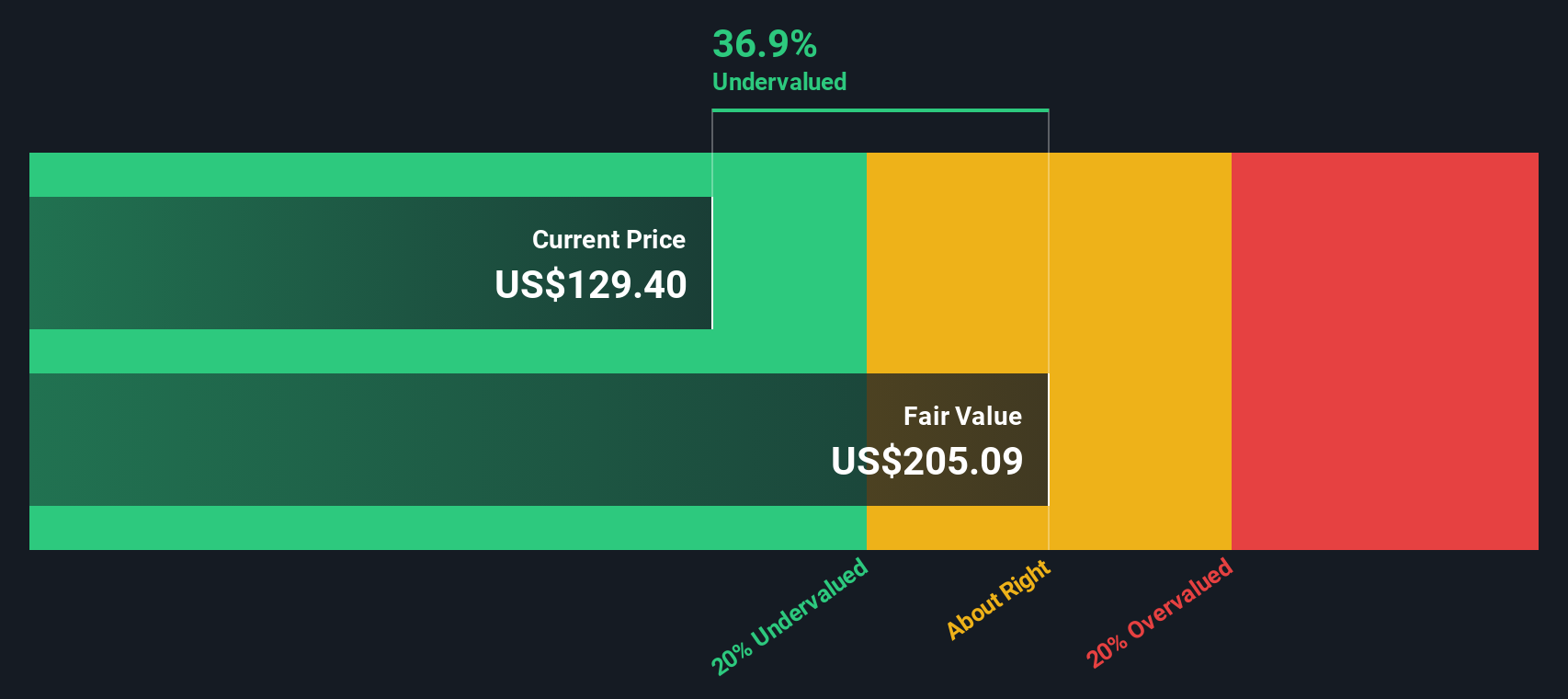

Another View: SWS DCF Model Suggests Undervaluation

While the company's market price looks expensive based on earnings multiples, the SWS DCF model presents a different perspective. According to our DCF, Nicolet Bankshares is trading almost 40% below its estimated fair value, indicating potential undervaluation. Could the market be underestimating future cash flows and long-term value?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nicolet Bankshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Nicolet Bankshares Narrative

If you see the story differently or want to dive into the data on your own terms, you can build a personal Nicolet Bankshares view in just minutes, Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Nicolet Bankshares.

Looking for More Investment Ideas?

Sharpen your portfolio by uncovering standout opportunities across new markets. Smart investors seize the moment, so do not miss the innovations and growth shaping tomorrow’s winners.

- Tap into the momentum of digital assets by evaluating these 79 cryptocurrency and blockchain stocks, which are pioneering secure payment solutions and reshaping financial technology.

- Get ahead of income trends with these 18 dividend stocks with yields > 3%, offering high yields and proven track records in returning value to shareholders.

- Catch the next wave in healthcare by assessing these 33 healthcare AI stocks, driving advanced patient care and breakthroughs in medical technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nicolet Bankshares might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NIC

Nicolet Bankshares

Operates as the bank holding company for Nicolet National Bank that provides banking products and services for businesses and individuals in Wisconsin, Michigan, and Minnesota.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets