Advertisement

- United States

- /

- Banks

- /

- NYSE:CUBI

A Fresh Look at Customers Bancorp (CUBI) Valuation After Strong Q3 Results and Preferred Stock Redemption

Simply Wall St

Reviewed by Simply Wall St

Customers Bancorp (CUBI) caught investor attention after posting a strong third-quarter update that beat expectations for both revenue and net interest income, while unveiling plans to redeem $85 million in preferred stock.

See our latest analysis for Customers Bancorp.

Customers Bancorp’s strong earnings update and news of a preferred stock redemption have fueled renewed interest, helping the company build momentum after a period of sideways trading. Even with some recent volatility, the 45% year-to-date share price return and a total shareholder return of over 113% for the past three years highlight the stock’s robust trajectory in both the short and longer term.

If you’re curious what else is catching investor attention lately, now is a perfect time to uncover opportunities with fast growing stocks with high insider ownership.

Given the company’s rapid earnings growth, analyst price targets well above current levels, and a significant discount to its estimated intrinsic value, the key question remains: Is Customers Bancorp truly undervalued, or are investors already pricing in further growth?

Most Popular Narrative: 18.6% Undervalued

With the most widely followed narrative setting fair value nearly 19% above the last close, the stock’s pricing appears to leave meaningful upside on the table. Strong digital banking catalysts, major business investments, and evolving team dynamics set the backdrop for a value thesis that looks beyond current market volatility.

The rapid digitization of commercial banking and payments is driving institutional clients to seek tech-focused, 24/7 banking solutions. This is a shift that Customers Bancorp capitalizes on through its proprietary cubiX platform. With payments volume of $1.5 trillion in 2024 and accelerating growth, ongoing regulatory clarity around digital assets and stablecoins positions Customers as the leading provider, supporting significant potential for deposit and fee income growth.

Ready to dig into the valuation math? The future price target is built on bold projections that include rapid earnings expansion and a digital platform strategy uncommon in traditional banking. Which surprising metric really moves the needle here? Find out what gives this narrative its edge before everyone else does.

Result: Fair Value of $84.75 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative could quickly shift if regulatory changes slow digital asset growth, or if rising competition puts pressure on margins and loan origination.

Find out about the key risks to this Customers Bancorp narrative.

Another View: Market Multiples Send a Different Signal

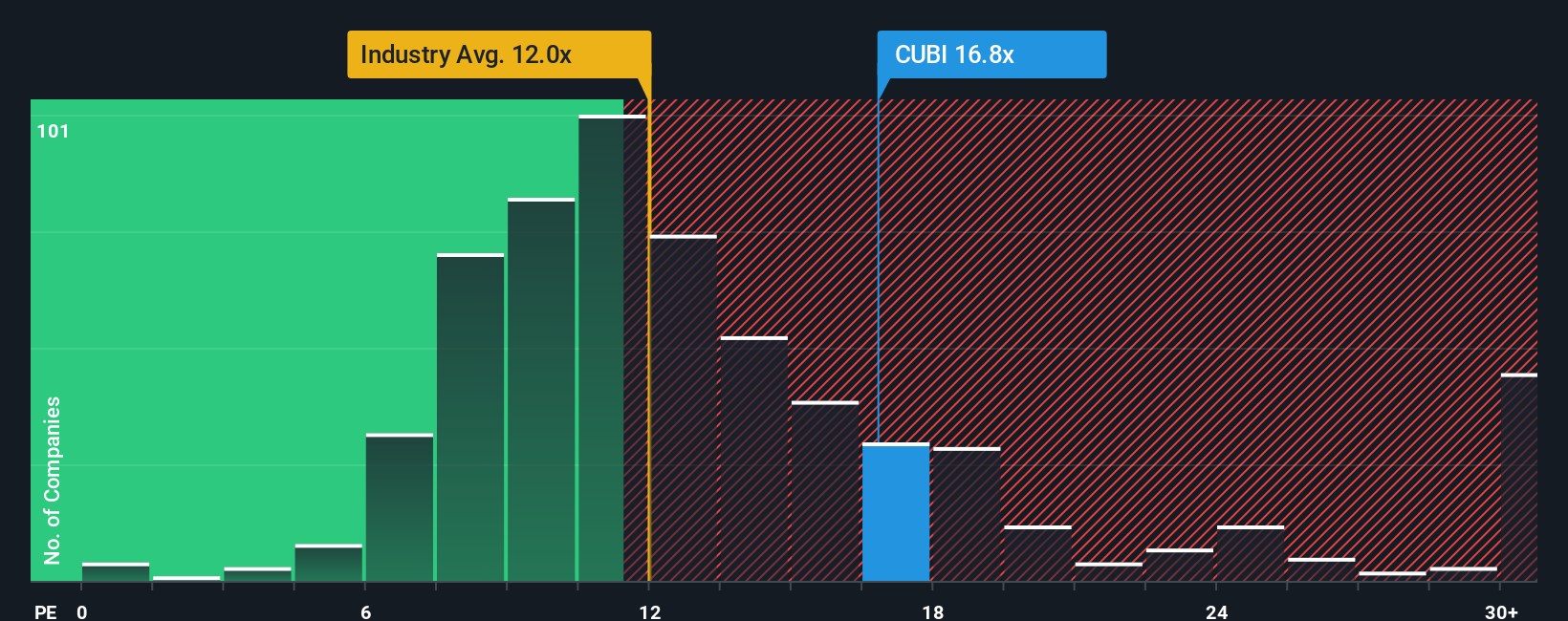

While the value thesis points to upside, a look at price-to-earnings multiples shows that investors are paying a premium compared to peers and the broader industry. Customers Bancorp’s 14.5x multiple is higher than the US Banks industry average of 11.4x and above similar companies at 10.7x. It is still below the market's calculated fair ratio of 15.3x. The premium may indicate growth potential or could suggest a risk of overpaying given the current momentum.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Customers Bancorp Narrative

If you see things differently or prefer hands-on research, you can build your own Customers Bancorp story using the data in just a few minutes. Do it your way.

A great starting point for your Customers Bancorp research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Why settle for just one exciting stock when there are powerful opportunities waiting to be found? Use these handpicked lists to guide your next smart investment move.

- Uncover income potential and stability with these 15 dividend stocks with yields > 3%, offering yields above 3% for consistent return seekers.

- Target long-term growth in healthcare by considering these 30 healthcare AI stocks, where artificial intelligence is driving breakthrough innovations.

- Step ahead in rapidly evolving technology and payments with these 81 cryptocurrency and blockchain stocks, revealing firms powering the crypto and blockchain ecosystem.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CUBI

Customers Bancorp

Operates as the bank holding company for Customers Bank that provides banking products and services.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative