The board of William Penn Bancorporation (NASDAQ:WMPN) has announced that it will pay a dividend of $0.03 per share on the 9th of February. Including this payment, the dividend yield on the stock will be 1.0%, which is a modest boost for shareholders' returns.

View our latest analysis for William Penn Bancorporation

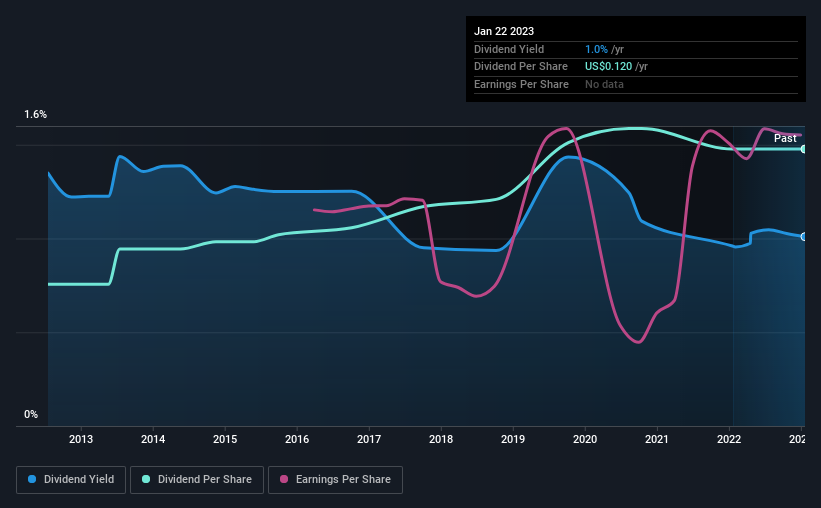

William Penn Bancorporation's Earnings Will Easily Cover The Distributions

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock.

William Penn Bancorporation has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Taking data from its last earnings report, calculating for the company's payout ratio shows 41%, which means that William Penn Bancorporation would be able to pay its last dividend without pressure on the balance sheet.

If the trend of the last few years continues, EPS will grow by 15.5% over the next 12 months. Assuming the dividend continues along recent trends, we think the future payout ratio could be 32% by next year, which is in a pretty sustainable range.

William Penn Bancorporation Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. Since 2013, the annual payment back then was $0.0614, compared to the most recent full-year payment of $0.12. This works out to be a compound annual growth rate (CAGR) of approximately 6.9% a year over that time. The dividend has been growing very nicely for a number of years, and has given its shareholders some nice income in their portfolios.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. We are encouraged to see that William Penn Bancorporation has grown earnings per share at 15% per year over the past five years. Earnings are on the uptrend, and it is only paying a small portion of those earnings to shareholders.

We Really Like William Penn Bancorporation's Dividend

In summary, it is good to see that the dividend is staying consistent, and we don't think there is any reason to suspect this might change over the medium term. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Are management backing themselves to deliver performance? Check their shareholdings in William Penn Bancorporation in our latest insider ownership analysis. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

If you're looking to trade William Penn Bancorporation, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if William Penn Bancorporation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:WMPN

William Penn Bancorporation

Operates as the holding company for William Penn Bank that provides retail and commercial banking products and related financial services in the United States.

Flawless balance sheet unattractive dividend payer.

Similar Companies

Market Insights

Community Narratives