Advertisement

- United States

- /

- Banks

- /

- NasdaqCM:PLBC

Plumas Bancorp (NASDAQ:PLBC) Looks Interesting, And It's About To Pay A Dividend

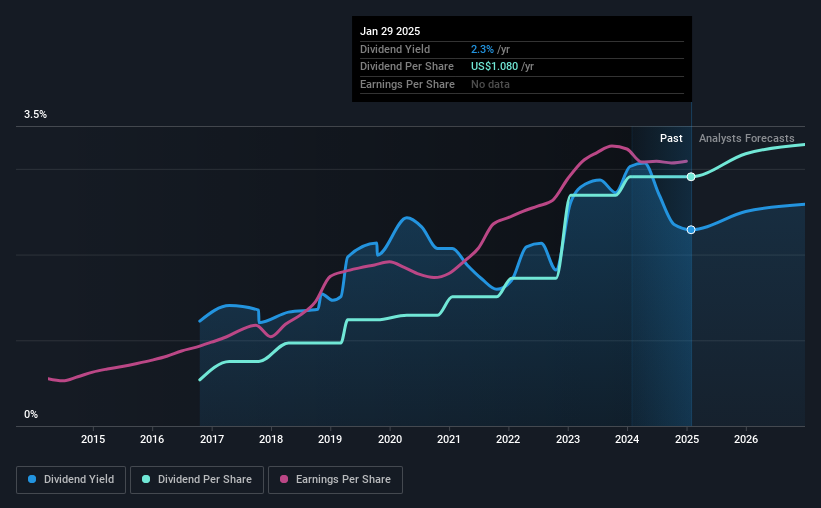

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Plumas Bancorp (NASDAQ:PLBC) is about to go ex-dividend in just 3 days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Meaning, you will need to purchase Plumas Bancorp's shares before the 3rd of February to receive the dividend, which will be paid on the 17th of February.

The company's next dividend payment will be US$0.30 per share, and in the last 12 months, the company paid a total of US$1.08 per share. Based on the last year's worth of payments, Plumas Bancorp has a trailing yield of 2.3% on the current stock price of US$47.17. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to investigate whether Plumas Bancorp can afford its dividend, and if the dividend could grow.

View our latest analysis for Plumas Bancorp

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Plumas Bancorp paid out just 22% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. For this reason, we're glad to see Plumas Bancorp's earnings per share have risen 10% per annum over the last five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Plumas Bancorp has delivered an average of 23% per year annual increase in its dividend, based on the past eight years of dividend payments. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

Final Takeaway

Is Plumas Bancorp worth buying for its dividend? Companies like Plumas Bancorp that are growing rapidly and paying out a low fraction of earnings, are usually reinvesting heavily in their business. This strategy can add significant value to shareholders over the long term - as long as it's done without issuing too many new shares. In summary, Plumas Bancorp appears to have some promise as a dividend stock, and we'd suggest taking a closer look at it.

Wondering what the future holds for Plumas Bancorp? See what the two analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:PLBC

Plumas Bancorp

Operates as the bank holding company for the Plumas Bank that provides various banking products and services for small and middle market businesses and individuals in California, Nevada, and Oregon.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative