Advertisement

- United States

- /

- Banks

- /

- NasdaqCM:LCNB

Shareholders May Be Wary Of Increasing LCNB Corp.'s (NASDAQ:LCNB) CEO Compensation Package

Key Insights

- LCNB's Annual General Meeting to take place on 22nd of April

- Total pay for CEO Eric Meilstrup includes US$431.0k salary

- The total compensation is similar to the average for the industry

- Over the past three years, LCNB's EPS fell by 15% and over the past three years, the total loss to shareholders 9.3%

LCNB Corp. (NASDAQ:LCNB) has not performed well recently and CEO Eric Meilstrup will probably need to up their game. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 22nd of April. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. The data we present below explains why we think CEO compensation is not consistent with recent performance.

See our latest analysis for LCNB

How Does Total Compensation For Eric Meilstrup Compare With Other Companies In The Industry?

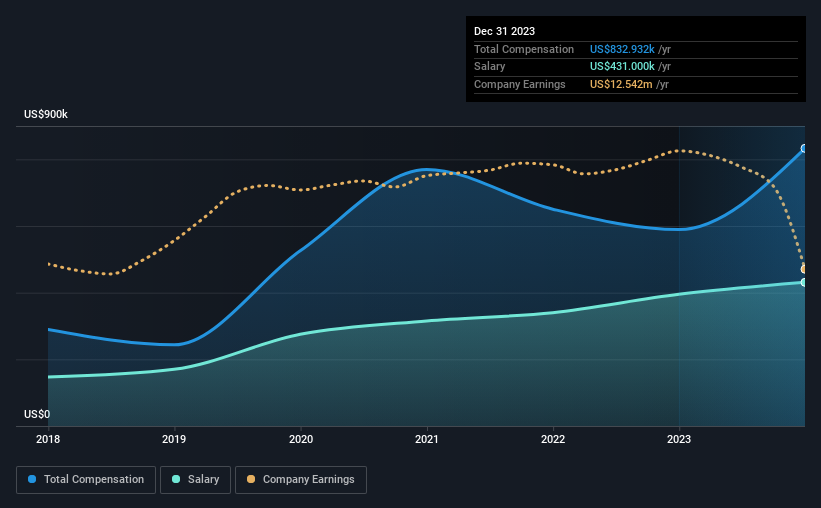

According to our data, LCNB Corp. has a market capitalization of US$186m, and paid its CEO total annual compensation worth US$833k over the year to December 2023. That's a notable increase of 41% on last year. We note that the salary of US$431.0k makes up a sizeable portion of the total compensation received by the CEO.

In comparison with other companies in the American Banks industry with market capitalizations ranging from US$100m to US$400m, the reported median CEO total compensation was US$1.1m. This suggests that LCNB remunerates its CEO largely in line with the industry average. What's more, Eric Meilstrup holds US$542k worth of shares in the company in their own name.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$431k | US$395k | 52% |

| Other | US$402k | US$194k | 48% |

| Total Compensation | US$833k | US$589k | 100% |

On an industry level, roughly 45% of total compensation represents salary and 55% is other remuneration. According to our research, LCNB has allocated a higher percentage of pay to salary in comparison to the wider industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

LCNB Corp.'s Growth

Over the last three years, LCNB Corp. has shrunk its earnings per share by 15% per year. It saw its revenue drop 7.2% over the last year.

The decline in EPS is a bit concerning. And the fact that revenue is down year on year arguably paints an ugly picture. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has LCNB Corp. Been A Good Investment?

Since shareholders would have lost about 9.3% over three years, some LCNB Corp. investors would surely be feeling negative emotions. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We've identified 3 warning signs for LCNB that investors should be aware of in a dynamic business environment.

Switching gears from LCNB, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:LCNB

LCNB

Operates as the financial holding company for LCNB National Bank that provides banking services in the United States.

Flawless balance sheet 6 star dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative