Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:INDB

Independent Bank (INDB): Valuation Insights Following Q3 Results and Enterprise Acquisition

Simply Wall St

Reviewed by Simply Wall St

Independent Bank (INDB) released its third quarter results, meeting revenue expectations and slightly exceeding earnings forecasts. Management pointed to the completed Enterprise acquisition and improved net interest margin as important factors behind this performance.

See our latest analysis for Independent Bank.

Independent Bank’s share price has steadily gained momentum this year, climbing 9.5% since January and closing at $69.2 most recently. While the third quarter’s earnings news and fresh buyback clearly reassured investors, the one-year total shareholder return stands at 12.6%. This suggests a moderate recovery after a challenging multi-year stretch.

If recent gains have you rethinking your strategy, it could be the perfect time to expand your search and discover fast growing stocks with high insider ownership

Given the recent earnings beat and a share price still trading below analyst targets, the question now is whether Independent Bank is an overlooked value play or if the market has already priced in the bank’s future prospects.

Most Popular Narrative: 16.4% Undervalued

Independent Bank's fair value in the most popular narrative stands well above its latest closing price. This sets the stage for a deeper look at what is driving its valuation outlook.

Ongoing U.S. population migration to secondary and smaller metropolitan areas, alongside strong small business formation in core markets, positions Independent Bank to benefit from outsized loan and deposit growth from community banking and small business lending, positively impacting long-term revenue and fee income.

Wondering what fuels this bullish outlook? The narrative relies on market trends and ambitious financial targets, suggesting aggressive revenue and profit growth assumptions that could redefine the company’s future. Explore further to uncover which underlying drivers shape this bold valuation call.

Result: Fair Value of $82.75 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing commercial real estate exposure and execution risks from recent acquisitions could still challenge the optimistic outlook for Independent Bank’s future growth.

Find out about the key risks to this Independent Bank narrative.

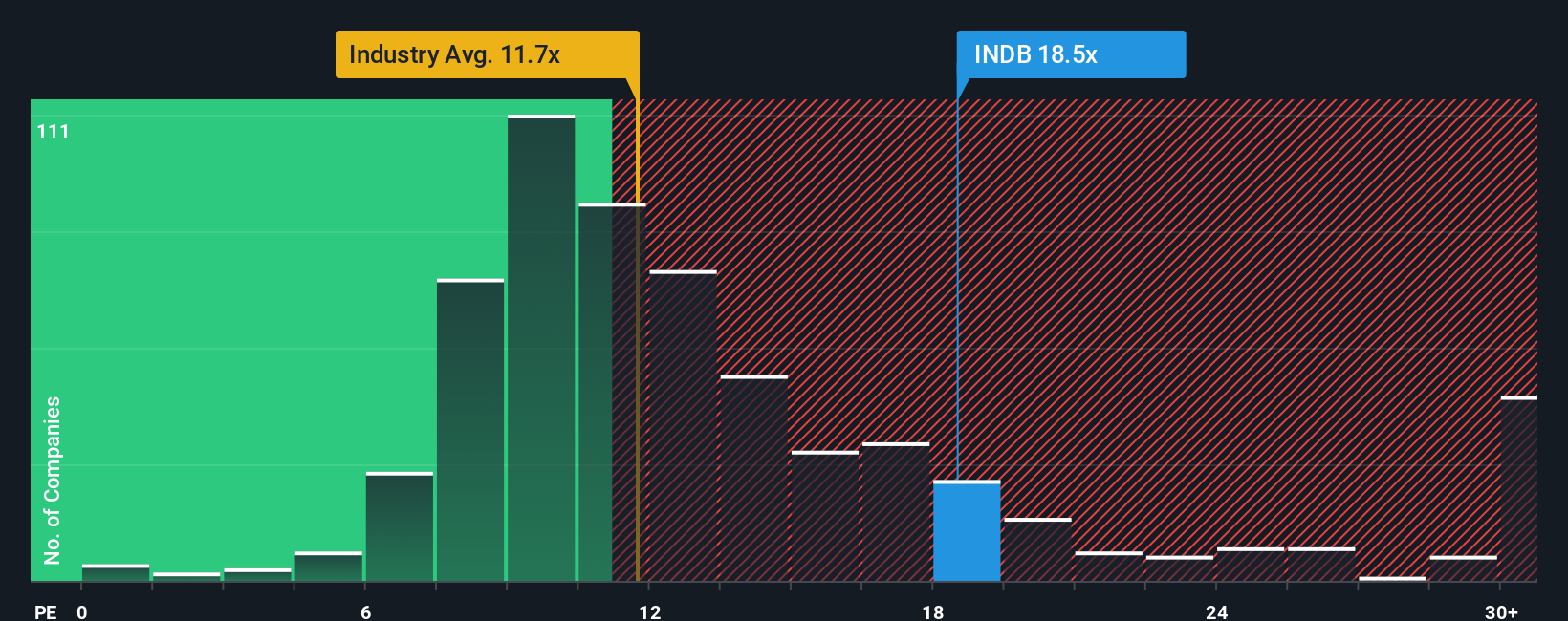

Another View: Multiples Point to a Different Story

Looking at valuation through price-to-earnings, Independent Bank trades at 19.2x, noticeably higher than its industry at 11.2x and its peers at 10x. The fair ratio stands at 18.3x, so shares appear expensive by almost every comparative check. Could this premium be justified, or is there valuation risk ahead?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Independent Bank Narrative

If you’d rather draw your own conclusions or want to dig deeper into the numbers, you can craft an independent perspective in just minutes. Do it your way

A great starting point for your Independent Bank research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Why settle for just one opportunity when you could get ahead of the curve? Use Simply Wall Street’s tools to uncover other stocks built for tomorrow.

- Tap into income potential and see which companies stand out for reliable yields by reviewing these 17 dividend stocks with yields > 3% offering payouts over 3%.

- Access the front lines of innovation and growth with these 27 AI penny stocks as these companies drive transformation in artificial intelligence.

- Zero in on value and financial strength by targeting these 3560 penny stocks with strong financials designed to balance risk and reward for bold investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:INDB

Independent Bank

Operates as the bank holding company for Rockland Trust Company that provides commercial banking products and services to individuals and small-to-medium sized businesses in the United States.

Flawless balance sheet with high growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor