Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:HONE

HarborOne Bancorp (NASDAQ:HONE) Is Paying Out A Larger Dividend Than Last Year

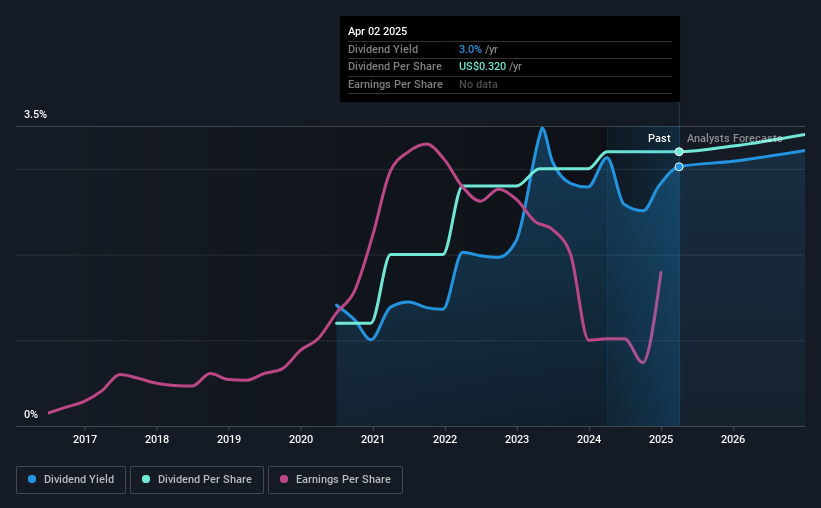

HarborOne Bancorp, Inc.'s (NASDAQ:HONE) periodic dividend will be increasing on the 23rd of April to $0.09, with investors receiving 13% more than last year's $0.08. Based on this payment, the dividend yield for the company will be 3.0%, which is fairly typical for the industry.

HarborOne Bancorp's Earnings Will Easily Cover The Distributions

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important.

Having paid out dividends for 5 years, HarborOne Bancorp has a good history of paying out a part of its earnings to shareholders. Based on HarborOne Bancorp's last earnings report, the payout ratio is at a decent 48%, meaning that the company is able to pay out its dividend with a bit of room to spare.

The next 3 years are set to see EPS grow by 75.8%. The future payout ratio could be 34% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

View our latest analysis for HarborOne Bancorp

HarborOne Bancorp Is Still Building Its Track Record

HarborOne Bancorp's dividend has been pretty stable for a little while now, but we will continue to be cautious until it has been demonstrated for a few more years. Since 2020, the annual payment back then was $0.12, compared to the most recent full-year payment of $0.32. This implies that the company grew its distributions at a yearly rate of about 22% over that duration. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. We are encouraged to see that HarborOne Bancorp has grown earnings per share at 14% per year over the past five years. The company is paying a reasonable amount of earnings to shareholders, and is growing earnings at a decent rate so we think it could be a decent dividend stock.

HarborOne Bancorp Looks Like A Great Dividend Stock

Overall, a dividend increase is always good, and we think that HarborOne Bancorp is a strong income stock thanks to its track record and growing earnings. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All of these factors considered, we think this has solid potential as a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Earnings growth generally bodes well for the future value of company dividend payments. See if the 4 HarborOne Bancorp analysts we track are forecasting continued growth with our free report on analyst estimates for the company . Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if HarborOne Bancorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:HONE

HarborOne Bancorp

Provides financial services to individuals, families, small and mid-size businesses, and municipalities.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|4.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|32.5% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor