- United States

- /

- Banks

- /

- NasdaqGM:HIFS

The one-year loss for Hingham Institution for Savings (NASDAQ:HIFS) shareholders likely driven by its shrinking earnings

Hingham Institution for Savings (NASDAQ:HIFS) shareholders should be happy to see the share price up 18% in the last month. But that doesn't change the reality of under-performance over the last twelve months. The cold reality is that the stock has dropped 33% in one year, under-performing the market.

On a more encouraging note the company has added US$40m to its market cap in just the last 7 days, so let's see if we can determine what's driven the one-year loss for shareholders.

Check out our latest analysis for Hingham Institution for Savings

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

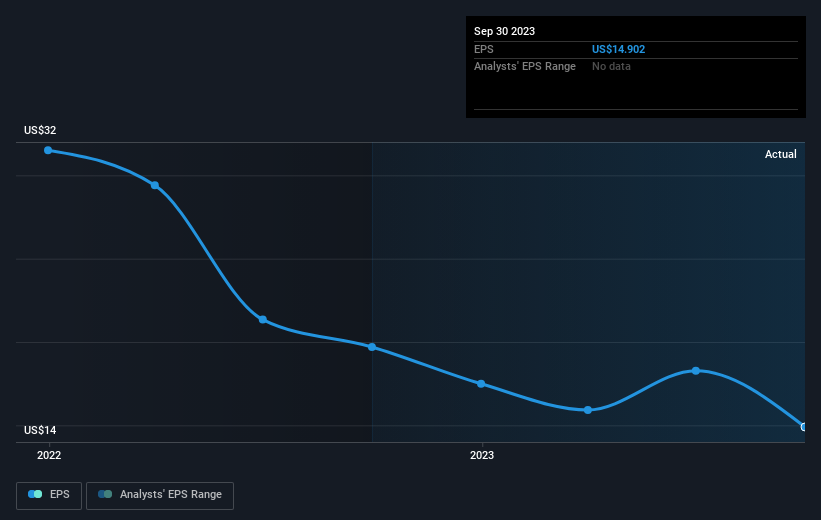

Unfortunately Hingham Institution for Savings reported an EPS drop of 24% for the last year. The share price decline of 33% is actually more than the EPS drop. This suggests the EPS fall has made some shareholders are more nervous about the business.

The company's earnings per share (over time) is depicted in the image below (click to see the exact numbers).

We consider it positive that insiders have made significant purchases in the last year. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. Dive deeper into the earnings by checking this interactive graph of Hingham Institution for Savings' earnings, revenue and cash flow.

A Different Perspective

While the broader market gained around 19% in the last year, Hingham Institution for Savings shareholders lost 32% (even including dividends). Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 0.4% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 2 warning signs for Hingham Institution for Savings that you should be aware of before investing here.

Hingham Institution for Savings is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Hingham Institution for Savings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:HIFS

Hingham Institution for Savings

Provides various financial products and services to individuals and small businesses in the United States.

Excellent balance sheet unattractive dividend payer.