Advertisement

- United States

- /

- Banks

- /

- NasdaqCM:BVFL

BV Financial (BVFL) Margin Decline Challenges Bullish Narratives on Earnings Stability

Simply Wall St

Reviewed by Simply Wall St

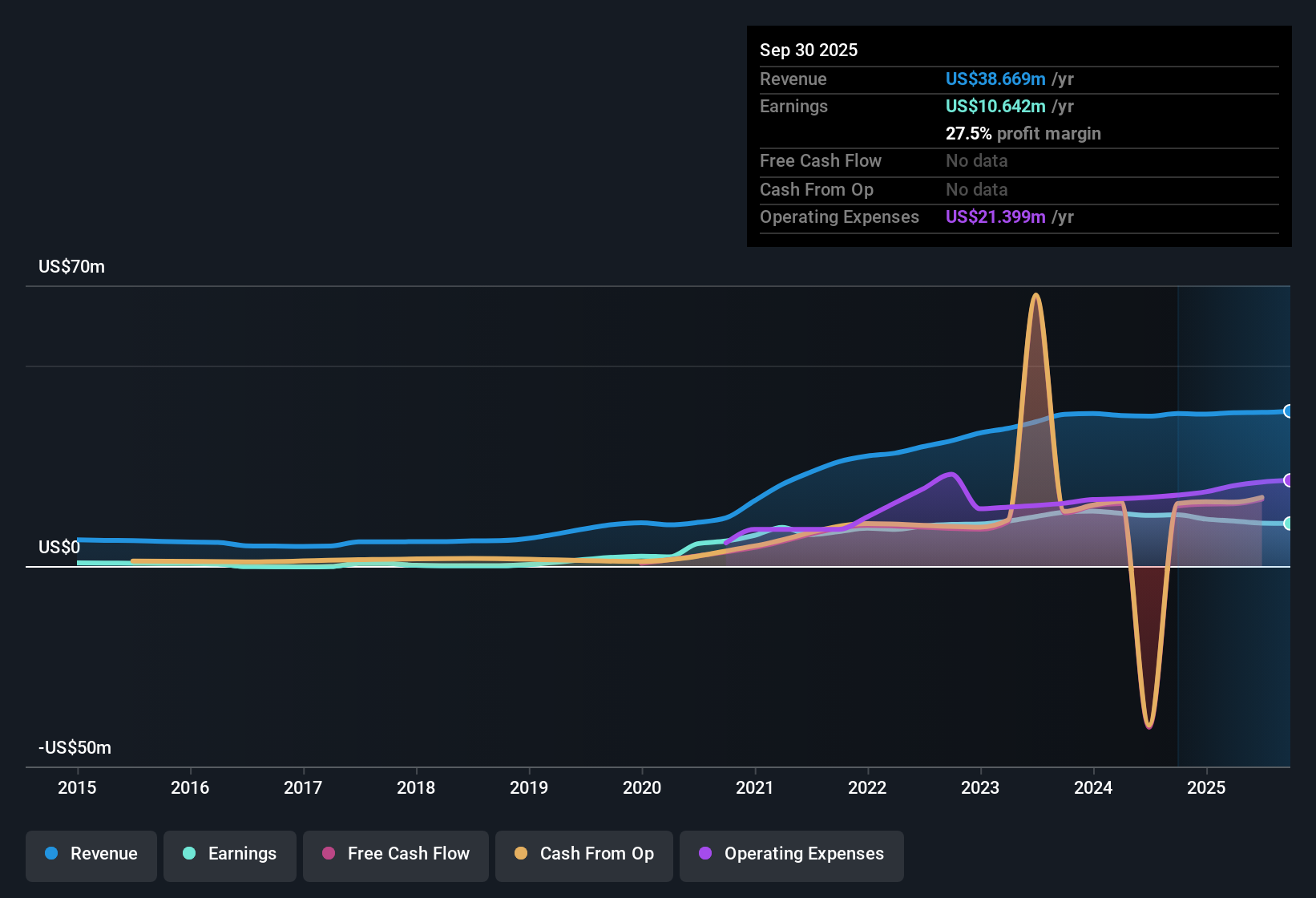

BV Financial (BVFL) reported a net profit margin of 27.9%, a noticeable drop from last year’s 33.9%. Over the past five years, the company has averaged earnings growth of 11.9% per year but posted negative earnings growth in the most recent year. The stock is currently trading at $14.70, which places its Price-to-Earnings ratio at 13.2x. This is higher than its peer group average of 8.3x and above the US Banks industry average of 11.2x, with shares sitting above an estimated fair value of $13.81. While high earnings quality and a lack of insider selling offer some comfort, the recent slide in margins and stalled profit growth could weigh on investor sentiment as the company seeks to restore its previous momentum.

See our full analysis for BV Financial.Next, we will see how these numbers hold up when compared to the prevailing narratives. Sometimes they reinforce investor sentiment and at other times they challenge the consensus view.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Slip Below Historical Average

- Net profit margin fell to 27.9%, sliding well below last year’s 33.9% and departing from its five-year earnings growth average of 11.9% per year.

- What is particularly notable is how the decline in margin heightens investor focus on the company’s ability to regain operating efficiency.

- The prior multi-year record of steady earnings expansion contrasts sharply with the most recent year’s downturn, giving investors a clear reason to await signs of stabilization.

- This kind of margin contraction can pressure expectations for future profit growth, especially in banking, where profitability often sets the tone for broader financial health.

Trading at a Premium to Peers

- BV Financial’s Price-to-Earnings ratio is 13.2x, well above both its peer average of 8.3x and the wider US Banks industry at 11.2x.

- This persistent premium valuation draws scrutiny, as investors now compare it to recent negative profit growth and a net margin that lags historical levels.

- Analysts monitoring relative multiples will note the tension between BV Financial’s quality reputation and its current valuation, which may be harder to justify without renewed growth.

- The DCF fair value estimate of $13.81 implies shares trade over fair value, limiting the case for those seeking immediate upside based only on current fundamentals.

Insider Moves Offer Minor Reassurance

- The company recently reported no substantial insider selling, marking a small but meaningful signal at a time when momentum has waned.

- While substantial selling might rattle investors, the lack thereof does little to sweep away concerns about sliding margins or stalled growth.

- Insider retention helps soothe some doubts, but with margins falling and last year’s earnings turning negative, most investors will want to see concrete operational or strategic progress before getting more optimistic.

- These fundamentals leave the market in a watchful, wait-and-see mode. Even stability in insider activity is not enough to shift sentiment decisively given profit concerns.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on BV Financial's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

BV Financial’s premium valuation and declining margins, along with recent negative earnings growth, signal a lack of dependable near-term momentum or value upside.

If you want to focus on better-priced opportunities with stronger fundamentals, use these 878 undervalued stocks based on cash flows to uncover companies currently trading below their estimated worth and positioned for potential gains.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BV Financial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:BVFL

BV Financial

Operates as the holding company for BayVanguard Bank that provides various financial services to individuals and businesses in the United States.

Flawless balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets