Advertisement

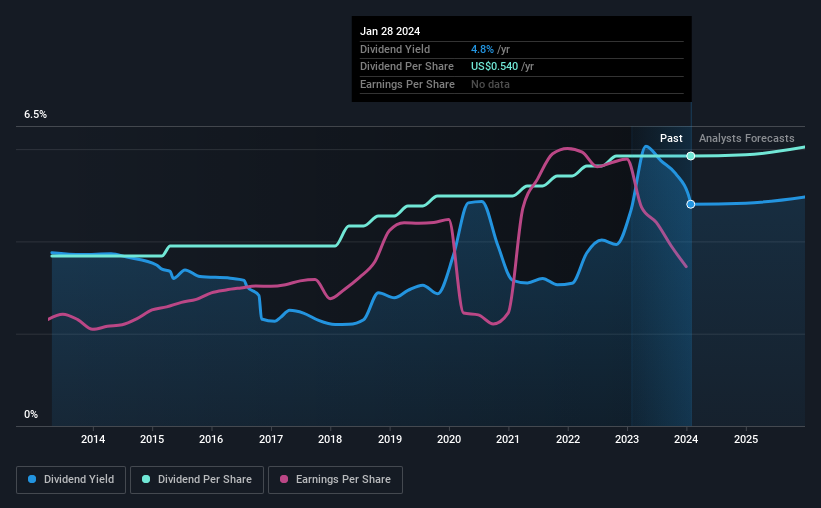

Brookline Bancorp, Inc.'s (NASDAQ:BRKL) investors are due to receive a payment of $0.135 per share on 23rd of February. This makes the dividend yield 4.8%, which will augment investor returns quite nicely.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Brookline Bancorp's stock price has increased by 37% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

See our latest analysis for Brookline Bancorp

Brookline Bancorp's Earnings Will Easily Cover The Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained.

Brookline Bancorp has a long history of paying out dividends, with its current track record at a minimum of 10 years. Past distributions do not necessarily guarantee future ones, but Brookline Bancorp's payout ratio of 64% is a good sign as this means that earnings decently cover dividends.

Looking forward, EPS is forecast to rise by 47.4% over the next 3 years. The future payout ratio could be 50% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

Brookline Bancorp Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. Since 2014, the annual payment back then was $0.34, compared to the most recent full-year payment of $0.54. This works out to be a compound annual growth rate (CAGR) of approximately 4.7% a year over that time. While the consistency in the dividend payments is impressive, we think the relatively slow rate of growth is less attractive.

The Dividend's Growth Prospects Are Limited

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Unfortunately things aren't as good as they seem. Brookline Bancorp has seen earnings per share falling at 4.0% per year over the last five years. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. Earnings are forecast to grow over the next 12 months and if that happens we could still be a little bit cautious until it becomes a pattern.

We should note that Brookline Bancorp has issued stock equal to 15% of shares outstanding. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

In Summary

Overall, we think Brookline Bancorp is a solid choice as a dividend stock, even though the dividend wasn't raised this year. The earnings coverage is acceptable for now, but with earnings on the decline we would definitely keep an eye on the payout ratio. Taking all of this into consideration, the dividend looks viable moving forward, but investors should be mindful that the company has pushed the boundaries of sustainability in the past and may do so again.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 2 warning signs for Brookline Bancorp that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Brookline Bancorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:BRKL

Brookline Bancorp

Beacon Financial Corporation operates as the holding company for Beacon Bank & Trust that provides various banking solutions in New England and New York, the United States.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor