- United States

- /

- Auto Components

- /

- NasdaqGS:QS

QuantumScape (NYSE:QS) Integrates Advanced Cobra Separator Process

QuantumScape (NYSE:QS) achieved a significant milestone by successfully integrating its advanced Cobra separator process into baseline cell production, potentially impacting its share price 102% increase over the last quarter. This development, expected to improve production speed and scalability, likely added weight to the company’s recent stock performance. While the broader market, including the Dow and Nasdaq, experienced moderate gains amid AI-driven growth and trade policy speculations, QuantumScape's innovations in battery technology distinguished its trajectory from index trends, contrasting with market sectors influenced by trade and inflation concerns.

We've identified 3 weaknesses for QuantumScape (1 is significant) that you should be aware of.

Find companies with promising cash flow potential yet trading below their fair value.

Over the past year, QuantumScape's shares have produced a total return of 54.34% for investors, registering a significant appreciation. Against the broader market's return of 12.6% and the US Auto Components industry's decline of 2.6% over the same period, QuantumScape's performance distinctly stands out. This robust performance underscores the market's optimism concerning the company's technological advancements and strategic partnerships.

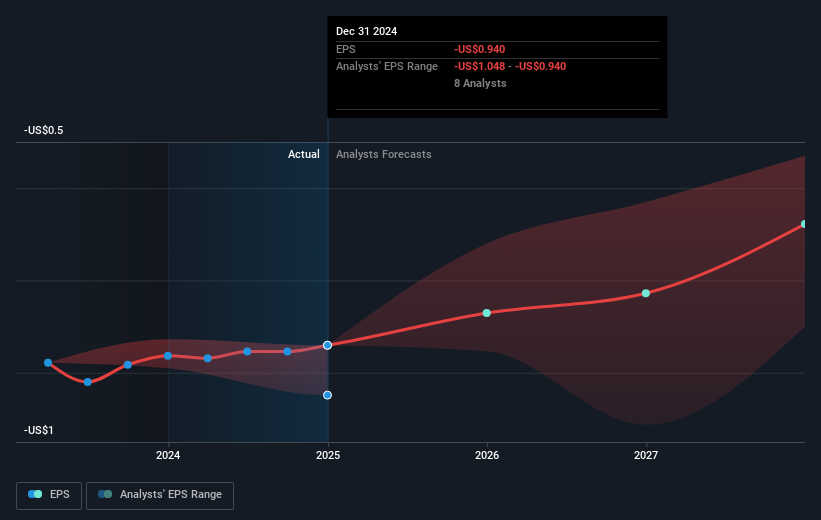

The integration of the advanced Cobra separator process, as mentioned in the introduction, may positively impact QuantumScape's future revenue and earnings, even though the company currently reports zero revenue and remains unprofitable with earnings of negative US$471.63 million. Analysts forecast revenue growth rates that surpass market averages, and the company's share price, despite recent volatility, remains below the consensus fair value estimate of US$20.08. This discount suggests potential misalignment between current market sentiments and analyst expectations, indicating room for possible price movement towards the target. Additionally, with the share price still trading well below its estimated fair value, there seems to be room for potential upside if QuantumScape's innovations achieve anticipated commercial successes.

Assess QuantumScape's previous results with our detailed historical performance reports.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if QuantumScape might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:QS

QuantumScape

Develops solid-state lithium-metal battery technology for electric vehicles and other applications in the United States.

Flawless balance sheet with slight risk.

Similar Companies

Market Insights

Weekly Picks

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Recently Updated Narratives

Bentley Systems’ Strategic Positioning in the Digital Infrastructure Cycle

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

$MRT at Roth - Pick of the Panel

Popular Narratives

Mastercard: The Best Dividend Stock You're Ignoring

The Wafer Giant Threatening NVIDIA's GPU Hegemony