- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:6141

Strong week for PlotechLtd (TWSE:6141) shareholders doesn't alleviate pain of three-year loss

While it may not be enough for some shareholders, we think it is good to see the Plotech Co.,Ltd (TWSE:6141) share price up 21% in a single quarter. But that cannot eclipse the less-than-impressive returns over the last three years. In fact, the share price is down 44% in the last three years, falling well short of the market return.

While the last three years has been tough for PlotechLtd shareholders, this past week has shown signs of promise. So let's look at the longer term fundamentals and see if they've been the driver of the negative returns.

Check out our latest analysis for PlotechLtd

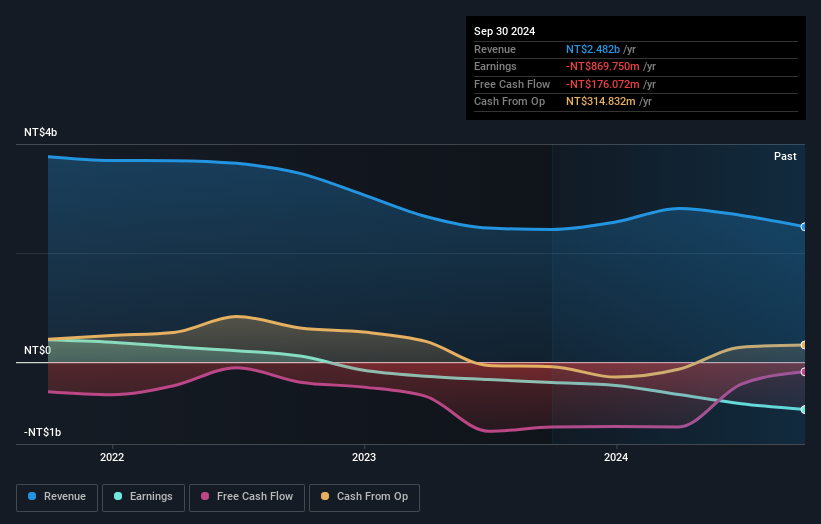

PlotechLtd wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

In the last three years PlotechLtd saw its revenue shrink by 16% per year. That means its revenue trend is very weak compared to other loss making companies. With revenue in decline, the share price decline of 13% per year is hardly undeserved. It would probably be worth asking whether the company can fund itself to profitability. The company will need to return to revenue growth as quickly as possible, if it wants to see some enthusiasm from investors.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

This free interactive report on PlotechLtd's balance sheet strength is a great place to start, if you want to investigate the stock further.

What About The Total Shareholder Return (TSR)?

We've already covered PlotechLtd's share price action, but we should also mention its total shareholder return (TSR). The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Dividends have been really beneficial for PlotechLtd shareholders, and that cash payout explains why its total shareholder loss of 41%, over the last 3 years, isn't as bad as the share price return.

A Different Perspective

PlotechLtd shareholders are down 4.2% for the year, but the market itself is up 29%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 2% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For instance, we've identified 4 warning signs for PlotechLtd (3 make us uncomfortable) that you should be aware of.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Taiwanese exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:6141

PlotechLtd

Engages in the designing, manufacturing, processing, and sale of films, printed circuit boards (PCB’s), and electronic components in Taiwan and China.

Slight and slightly overvalued.

Market Insights

Community Narratives