Advertisement

Sichuan Yahua Industrial Group Joins 2 Other Stocks That May Be Priced Below Estimated Value

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a mixed start to the new year, with U.S. stocks closing out a strong 2024 despite recent volatility and economic indicators like the Chicago PMI showing contraction, investors are keenly observing for opportunities that might be undervalued amidst these fluctuations. In this context, identifying stocks that may be priced below their estimated value can offer potential advantages, particularly when market dynamics suggest caution and strategic positioning.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Avant Group (TSE:3836) | ¥1881.00 | ¥3755.69 | 49.9% |

| Decisive Dividend (TSXV:DE) | CA$5.98 | CA$11.88 | 49.7% |

| Emporiki Eisagogiki Aftokiniton Ditrohon kai Mihanon Thalassis Societe Anonyme (ATSE:MOTO) | €2.725 | €5.45 | 50% |

| EnomotoLtd (TSE:6928) | ¥1438.00 | ¥2887.59 | 50.2% |

| Elekta (OM:EKTA B) | SEK61.45 | SEK122.25 | 49.7% |

| W5 Solutions (OM:W5) | SEK46.85 | SEK93.57 | 49.9% |

| Mr. Cooper Group (NasdaqCM:COOP) | US$93.54 | US$186.41 | 49.8% |

| Exosens (ENXTPA:EXENS) | €22.42 | €44.72 | 49.9% |

| Cicor Technologies (SWX:CICN) | CHF59.80 | CHF118.90 | 49.7% |

| Vogo (ENXTPA:ALVGO) | €2.93 | €5.85 | 49.9% |

Let's dive into some prime choices out of the screener.

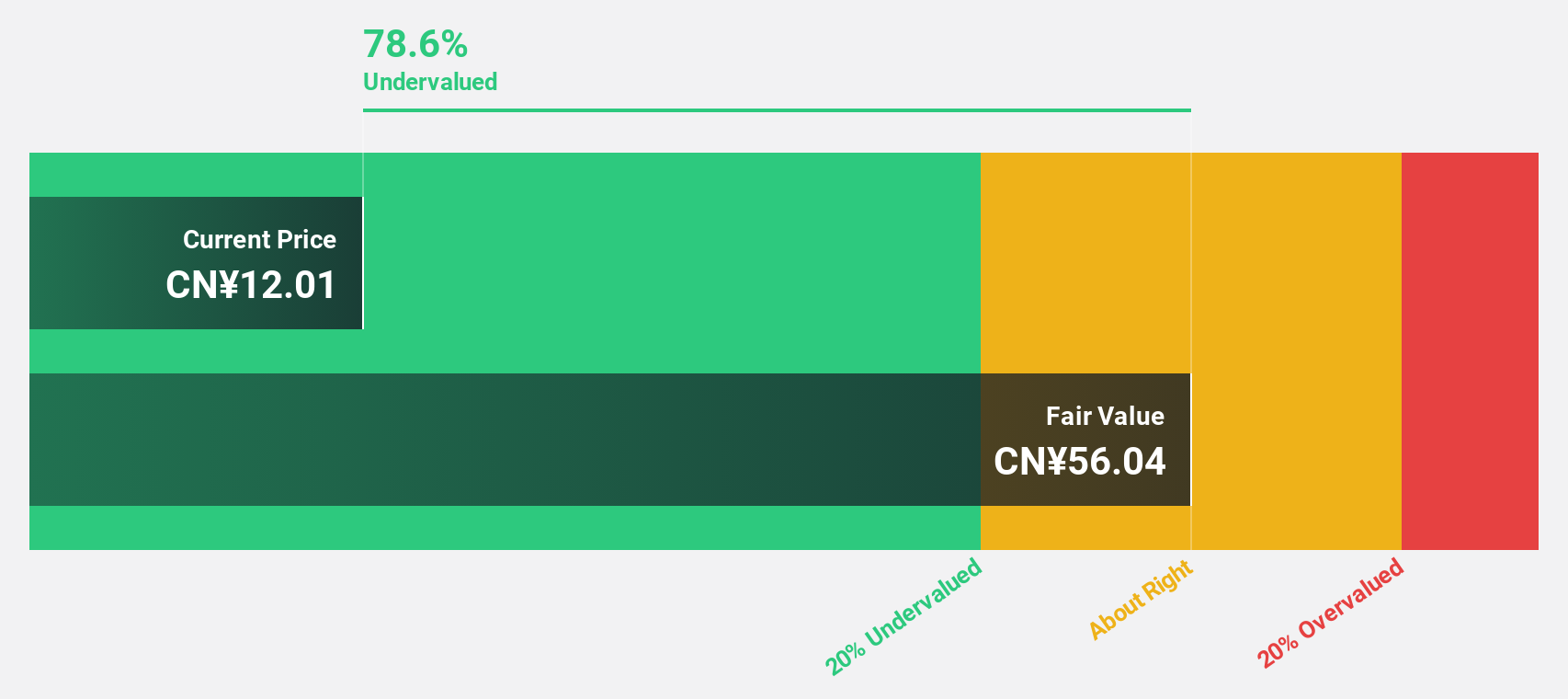

Sichuan Yahua Industrial Group (SZSE:002497)

Overview: Sichuan Yahua Industrial Group Co., Ltd. researches, produces, and sells civil explosives and blasting services both in China and internationally, with a market cap of CN¥12.83 billion.

Operations: Revenue Segments (in millions of CN¥): Civil Explosives and Blasting Services: CN¥null

Estimated Discount To Fair Value: 46.8%

Sichuan Yahua Industrial Group is trading at CN¥11.44, significantly below its estimated fair value of CN¥21.49, indicating potential undervaluation based on discounted cash flow analysis. Despite recent earnings declines—sales and net income dropped to CN¥5.92 billion and CN¥154.61 million respectively—the company is expected to achieve above-average market profit growth over the next three years, although its return on equity remains forecasted at a modest 11.3%.

- The growth report we've compiled suggests that Sichuan Yahua Industrial Group's future prospects could be on the up.

- Dive into the specifics of Sichuan Yahua Industrial Group here with our thorough financial health report.

Wuxi Best Precision Machinery (SZSE:300580)

Overview: Wuxi Best Precision Machinery Co., Ltd. specializes in the research, development, production, and sale of precision parts, intelligent equipment, and tooling products both in China and internationally with a market cap of CN¥11.14 billion.

Operations: Wuxi Best Precision Machinery Co., Ltd. generates revenue through its activities in precision parts, intelligent equipment, and tooling products across domestic and international markets.

Estimated Discount To Fair Value: 21.1%

Wuxi Best Precision Machinery, trading at CN¥23.54, is currently valued below its estimated fair value of CN¥29.83, suggesting it might be undervalued based on discounted cash flow analysis. The company reported nine-month sales of CN¥1.04 billion and net income of CN¥224.82 million, showing growth from the previous year. With forecasted revenue and earnings growth rates surpassing market averages, potential exists despite a volatile share price and an anticipated low return on equity at 13.2%.

- Our earnings growth report unveils the potential for significant increases in Wuxi Best Precision Machinery's future results.

- Navigate through the intricacies of Wuxi Best Precision Machinery with our comprehensive financial health report here.

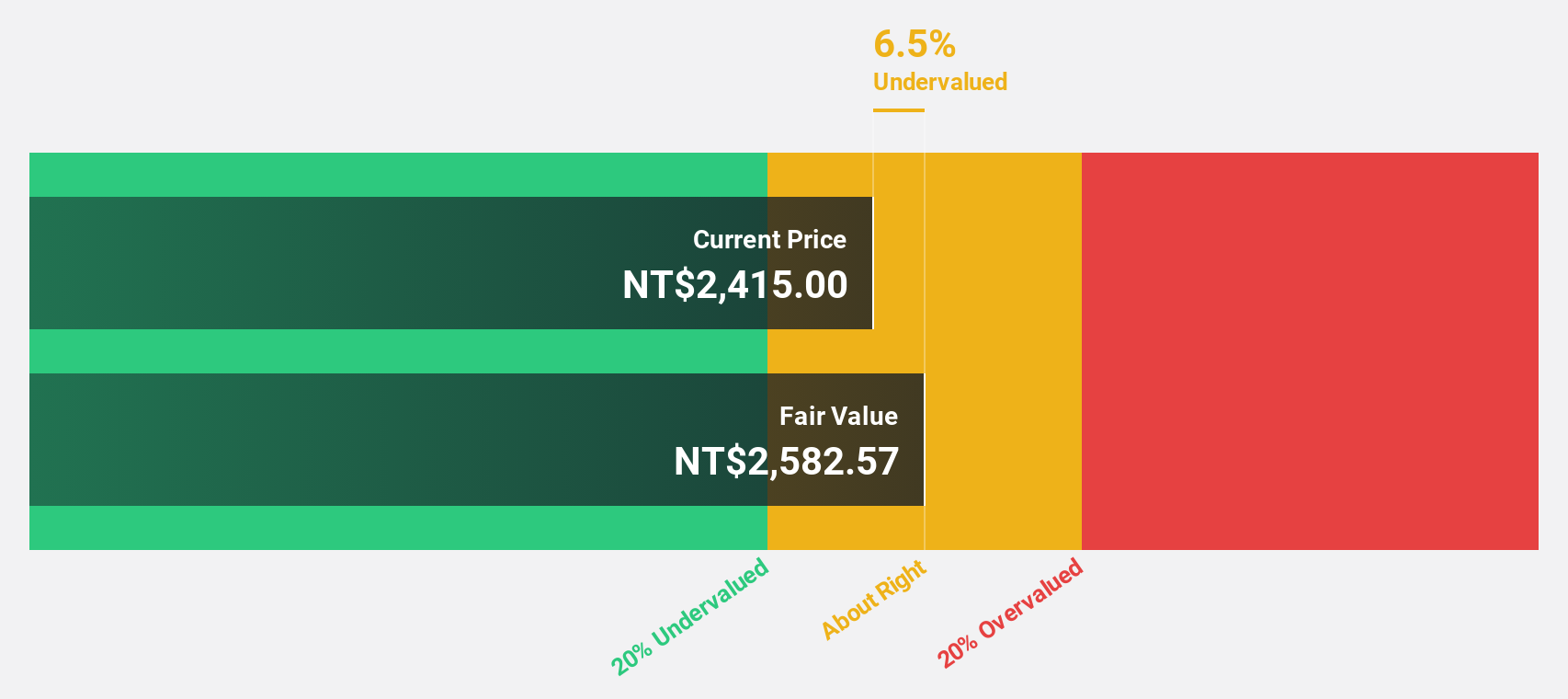

King Slide Works (TWSE:2059)

Overview: King Slide Works Co., Ltd. focuses on the research, development, design, and sale of rail kits for servers and network communication equipment in Taiwan, with a market capitalization of NT$143.42 billion.

Operations: The company's revenue segments include NT$2.16 billion from Chuanhu Company and NT$7.12 billion from Chuan Yi Company.

Estimated Discount To Fair Value: 11.7%

King Slide Works, trading at NT$1,510, is below its estimated fair value of NT$1,709.33. The company's recent earnings report shows significant growth with third-quarter sales reaching NT$2.58 billion and net income at NT$1.15 billion compared to last year’s figures. Despite high share price volatility and slower-than-market forecasted earnings growth of 18.42% annually, the firm's revenue is expected to grow rapidly at 21.2% per year.

- Upon reviewing our latest growth report, King Slide Works' projected financial performance appears quite optimistic.

- Click here to discover the nuances of King Slide Works with our detailed financial health report.

Key Takeaways

- Click through to start exploring the rest of the 878 Undervalued Stocks Based On Cash Flows now.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002497

Sichuan Yahua Industrial Group

Research, produces, and sells civil explosive equipment and blasting engineering service in China and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor