- Taiwan

- /

- Semiconductors

- /

- TWSE:3711

Top Growth Companies With Strong Insider Ownership

Reviewed by Simply Wall St

As global markets navigate a period of economic uncertainty marked by rate cuts from major central banks and mixed performances across indices, the Nasdaq Composite stands out with its record-breaking highs, driven by the robust performance of growth stocks. In such an environment, companies with strong insider ownership often attract attention as they can indicate confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 27% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.9% | 37.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.4% |

| Medley (TSE:4480) | 34% | 31.7% |

| Pharma Mar (BME:PHM) | 11.8% | 56.2% |

| CD Projekt (WSE:CDR) | 29.7% | 27% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.4% | 66.3% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 111.4% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's review some notable picks from our screened stocks.

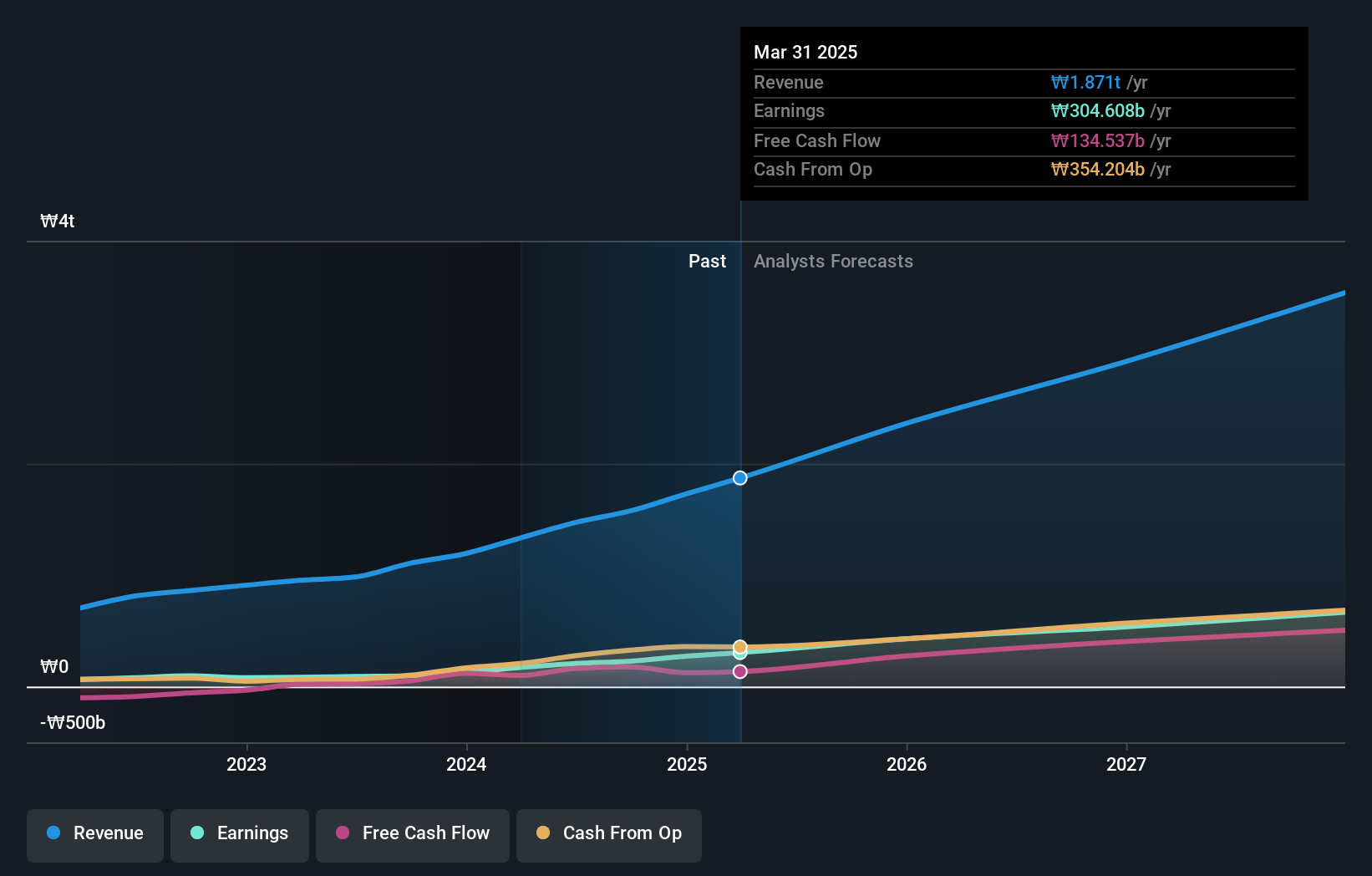

Samyang Foods (KOSE:A003230)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Samyang Foods Co., Ltd., along with its subsidiaries, operates in the food industry both in South Korea and internationally, with a market capitalization of approximately ₩5.27 trillion.

Operations: Revenue Segments (in millions of ₩):

Insider Ownership: 11.6%

Earnings Growth Forecast: 22.6% p.a.

Samyang Foods has shown impressive growth, with earnings increasing by 133.8% over the past year and forecasted to grow significantly at 22.63% annually over the next three years. The company's return on equity is expected to be high in three years, indicating strong financial health. Despite revenue growth being slower than earnings at 17.1%, it still surpasses the Korean market average of 5.2%. Currently trading at a substantial discount to its estimated fair value, Samyang Foods presents potential for investors focused on growth with high insider ownership dynamics.

- Unlock comprehensive insights into our analysis of Samyang Foods stock in this growth report.

- Our valuation report here indicates Samyang Foods may be overvalued.

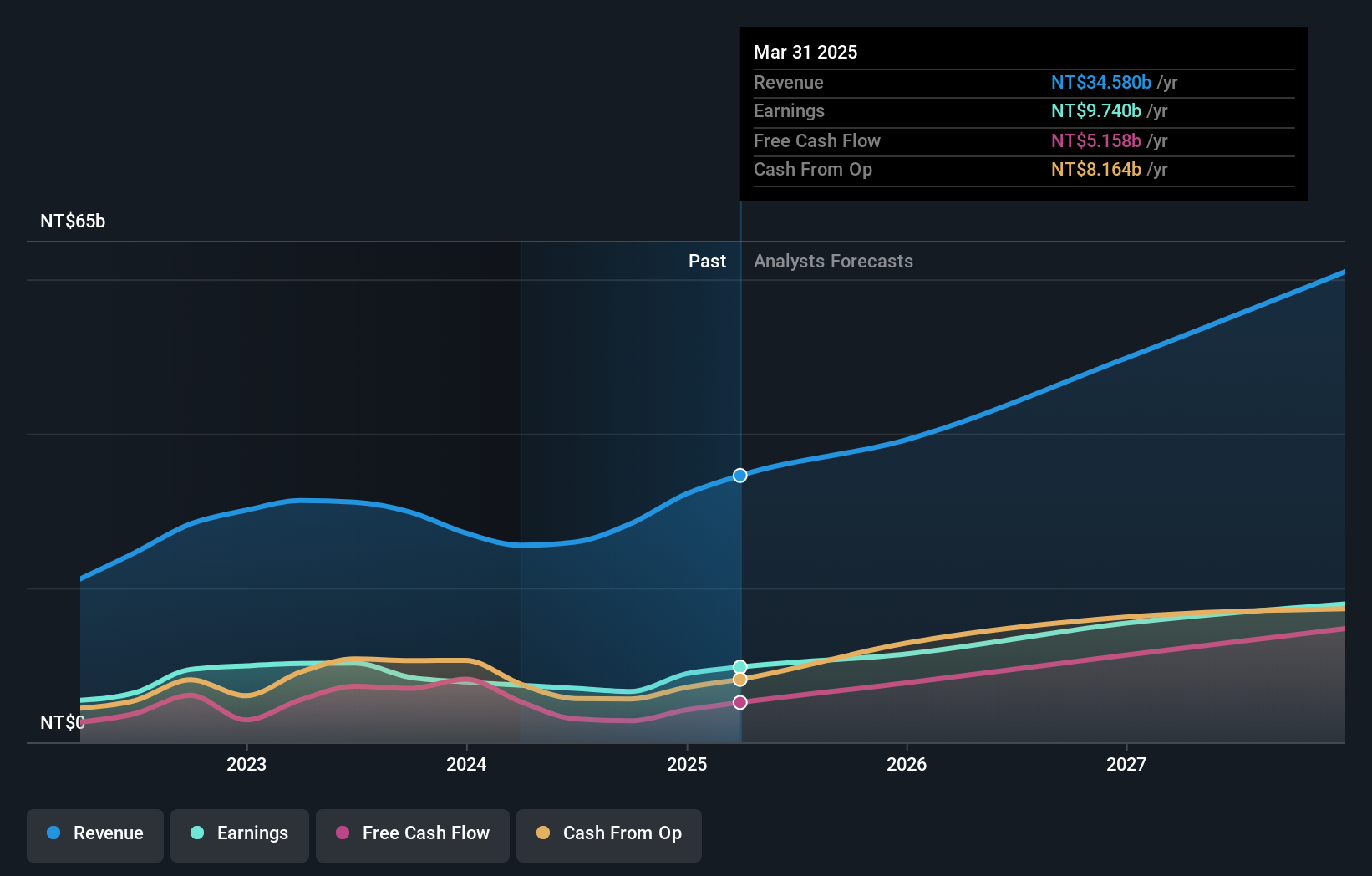

E Ink Holdings (TPEX:8069)

Simply Wall St Growth Rating: ★★★★★★

Overview: E Ink Holdings Inc. researches, develops, manufactures, and sells electronic paper display panels worldwide with a market cap of NT$304.54 billion.

Operations: The company generates revenue from its electronic components and parts segment, amounting to NT$28.32 billion.

Insider Ownership: 10.8%

Earnings Growth Forecast: 39.7% p.a.

E Ink Holdings is poised for substantial growth, with revenue and earnings projected to grow at 29.5% and 39.7% annually, respectively, outpacing the Taiwan market averages. Despite a recent decline in net income compared to last year, the company remains undervalued by 20.2% relative to its fair value estimate. Analysts anticipate a stock price increase of 28.7%. High insider ownership may align management interests with shareholders, supporting long-term growth prospects.

- Click to explore a detailed breakdown of our findings in E Ink Holdings' earnings growth report.

- Our comprehensive valuation report raises the possibility that E Ink Holdings is priced lower than what may be justified by its financials.

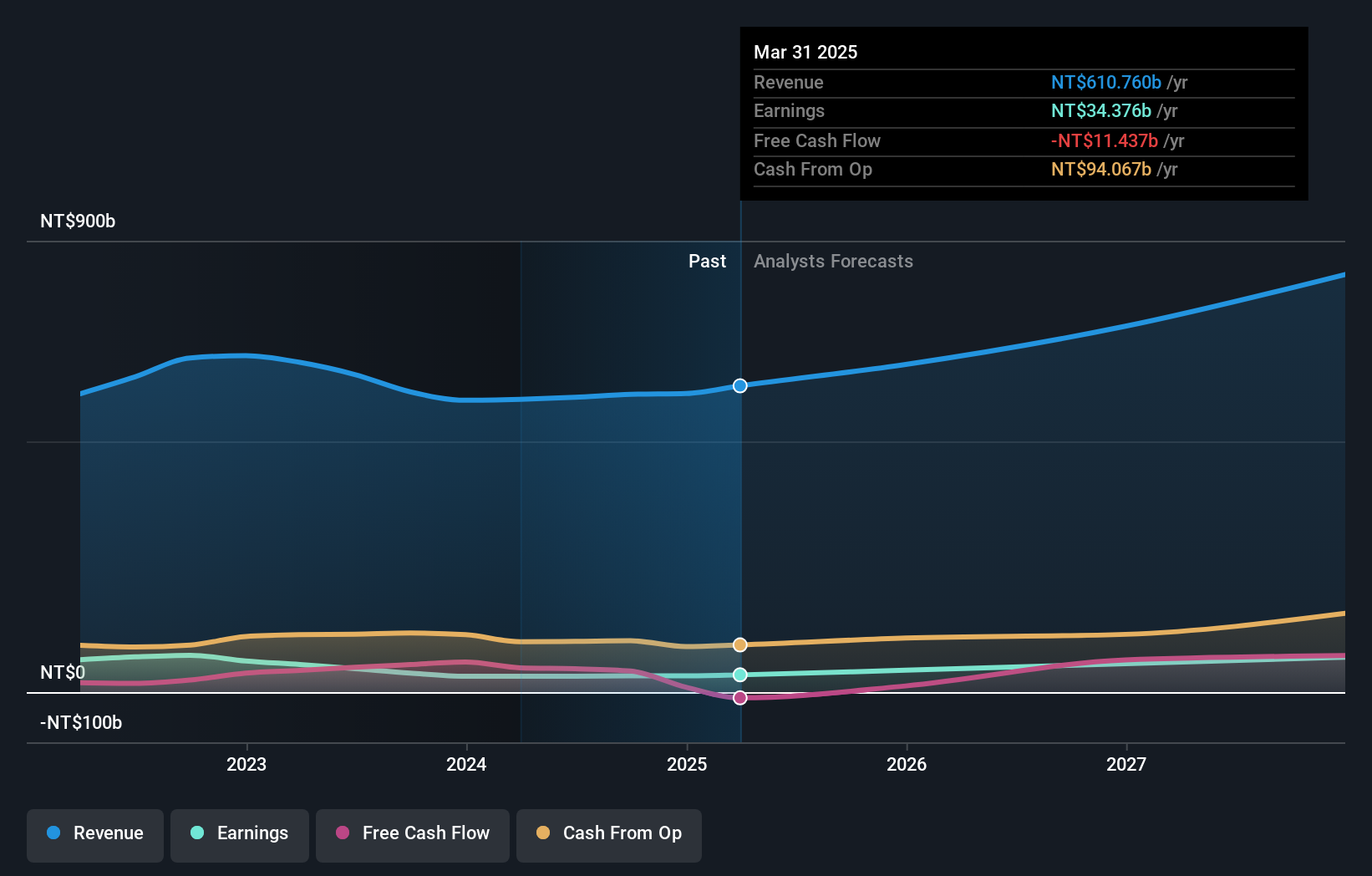

ASE Technology Holding (TWSE:3711)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ASE Technology Holding Co., Ltd. offers semiconductor packaging and testing, as well as electronic manufacturing services globally, with a market cap of NT$698.60 billion.

Operations: The company's revenue is primarily derived from Packaging (NT$263.44 billion), Electronic Manufacturing Services (EMS) (NT$308.95 billion), and Testing (NT$52.60 billion).

Insider Ownership: 28.5%

Earnings Growth Forecast: 32.9% p.a.

ASE Technology Holding is positioned for growth, with earnings projected to rise significantly at 32.9% annually, surpassing the Taiwan market average. While recent monthly revenues showed slight declines year-over-year, the company reported increased quarterly revenues and net income compared to last year. Trading below its estimated fair value by 23.7%, ASE's insider ownership could align management interests with shareholders, potentially enhancing long-term performance despite an unstable dividend history.

- Click here to discover the nuances of ASE Technology Holding with our detailed analytical future growth report.

- Upon reviewing our latest valuation report, ASE Technology Holding's share price might be too pessimistic.

Taking Advantage

- Dive into all 1568 of the Fast Growing Companies With High Insider Ownership we have identified here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:3711

ASE Technology Holding

Provides semiconductors packaging and testing, and electronic manufacturing services in the United States, Taiwan, Asia, Europe, and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Community Narratives