Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:4919

Take Care Before Diving Into The Deep End On Nuvoton Technology Corporation (TWSE:4919)

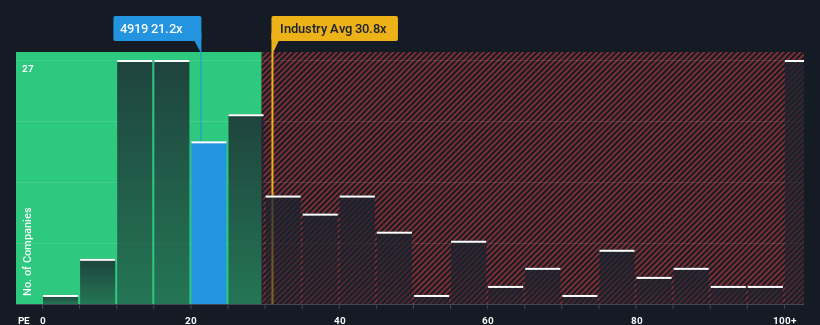

There wouldn't be many who think Nuvoton Technology Corporation's (TWSE:4919) price-to-earnings (or "P/E") ratio of 21.2x is worth a mention when the median P/E in Taiwan is similar at about 21x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

While the market has experienced earnings growth lately, Nuvoton Technology's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is moderate because investors think this poor earnings performance will turn around. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Check out our latest analysis for Nuvoton Technology

What Are Growth Metrics Telling Us About The P/E?

Nuvoton Technology's P/E ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the market.

Retrospectively, the last year delivered a frustrating 39% decrease to the company's bottom line. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Shifting to the future, estimates from the three analysts covering the company suggest earnings should grow by 34% over the next year. That's shaping up to be materially higher than the 24% growth forecast for the broader market.

In light of this, it's curious that Nuvoton Technology's P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From Nuvoton Technology's P/E?

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Nuvoton Technology's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Plus, you should also learn about these 3 warning signs we've spotted with Nuvoton Technology.

If these risks are making you reconsider your opinion on Nuvoton Technology, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Nuvoton Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:4919

Nuvoton Technology

A semiconductor company, engages in the research, design, development, manufacture, and sale of integrated circuits (ICs) in Taiwan and internationally.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

18 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.8% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k13.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Procter & Gamble ·

Insiders Sell, Investors Watch: What’s Going On at PG?

Fair Value:US$1506.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CW

Cwburton on Verano Holdings ·

Waiting for the Inevitable

Fair Value:CA$5.5278.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.6% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8684.3% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Trending Discussion

OI

OilStates on Oil States International ·

This article is overall well written. However, to correct a few points and to highlight a few additional points: -The shift towards more stable long-cycle offshore and international projects does not increase volatility or exposure to short-cycle markets, quite the opposite. Offshore projects have a much longer investment cycle, duration, and low volatility given these are multi-decade assets. -The article notes a lack of exposure to renewables. Oil States has applied decades of experience in technologies for traditional oil & gas technologies into the renewables sector including transfer of fixed and floating offshore platform technologies into offshore wind, downhole perforating and well completions technologies into geothermal, along with over 50+ renewables projects completed. We are supportive of a broad energy mix, yet to meet growing global energy demand requires both traditional as well as lower carbon resources. Both elements as well as other industrial product orders continue to contribute to Oil States decade-high backlog, which provides significant future revenue visibility. -One of the main storylines not captured here is cash flow generation. 75% of Company revenues (up from 51% in 2022) now come from offshore and international work, which provides good margins. With the strength of the Offshore Manufactured Products business segment, the high-grading of U.S. domestic land activities to focus on higher margin business lines, free cash flow (a non-GAAP metric) has grown significantly ($70 million in free cash flow on a TTM basis as of Sept. 30, 2025). This is quite high for a Company at this market cap, which results in a higher free cash flow yield vs. peers. -Free cash is being used to repurchase shares, to pay down debt (nearing net-debt zero), and to increase returns to stockholders. More detail can be found in our latest investor presentation here: https://ir.oilstatesintl.com/events-and-presentations/default.aspx

0

|0