- Taiwan

- /

- Semiconductors

- /

- TPEX:5314

Undiscovered Gems None And 2 Other Top Picks With Strong Potential

Reviewed by Simply Wall St

As global markets navigate a landscape shaped by cautious Federal Reserve commentary and political uncertainties, small-cap stocks have faced particular challenges, with indices like the S&P 600 experiencing notable declines. Amidst this backdrop of fluctuating interest rates and economic indicators, identifying promising investment opportunities requires a keen eye for companies with robust fundamentals and growth potential that may not yet be fully recognized by the broader market.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Resource Alam Indonesia | 2.66% | 30.36% | 43.87% | ★★★★★★ |

| Philippine Savings Bank | NA | 5.49% | 20.73% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Mandiri Herindo Adiperkasa | NA | 20.72% | 11.08% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Arab Insurance Group (B.S.C.) | NA | -59.20% | 20.33% | ★★★★★☆ |

| Eclatorq Technology | 37.47% | 8.43% | 18.41% | ★★★★★☆ |

| Chita Kogyo | 8.34% | 2.84% | 8.49% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Yuan Cheng CableLtd | 112.32% | 6.17% | 58.39% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Shenzhen Uniconn Technology (SZSE:301631)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Shenzhen Uniconn Technology Co., Ltd. specializes in the research, design, production, sale, and service of electrical connection components in China with a market cap of CN¥8.29 billion.

Operations: Shenzhen Uniconn Technology generates revenue primarily from the sale of electrical connection components. The company's cost structure includes expenses related to research and development, design, production, sales, and service activities. Its financial performance is marked by a notable net profit margin trend that reflects its operational efficiency in managing costs relative to its revenue streams.

Shenzhen Uniconn Technology, a dynamic player in the tech space, has shown impressive growth with earnings surging 29.1% last year, outpacing the electronic industry’s modest 1.9%. The company recently completed an IPO raising CNY 1.19 billion and reported significant revenue growth for the first nine months of 2024 at CNY 2.72 billion compared to CNY 2.06 billion a year prior. Net income also saw an uptick to CNY 183.67 million from CNY 177.04 million previously, highlighting its robust performance amidst market challenges and positioning it attractively below fair value by over 30%.

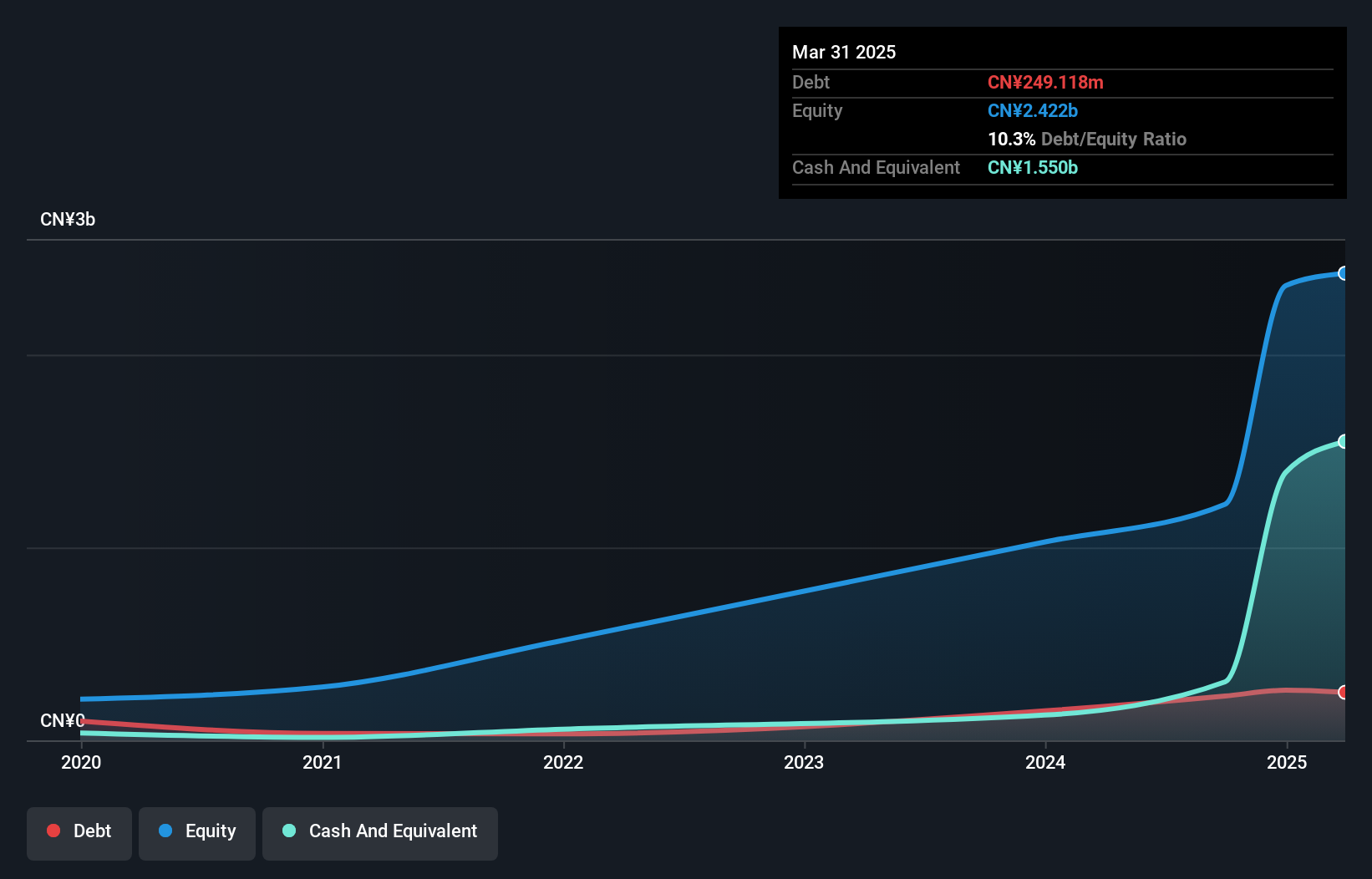

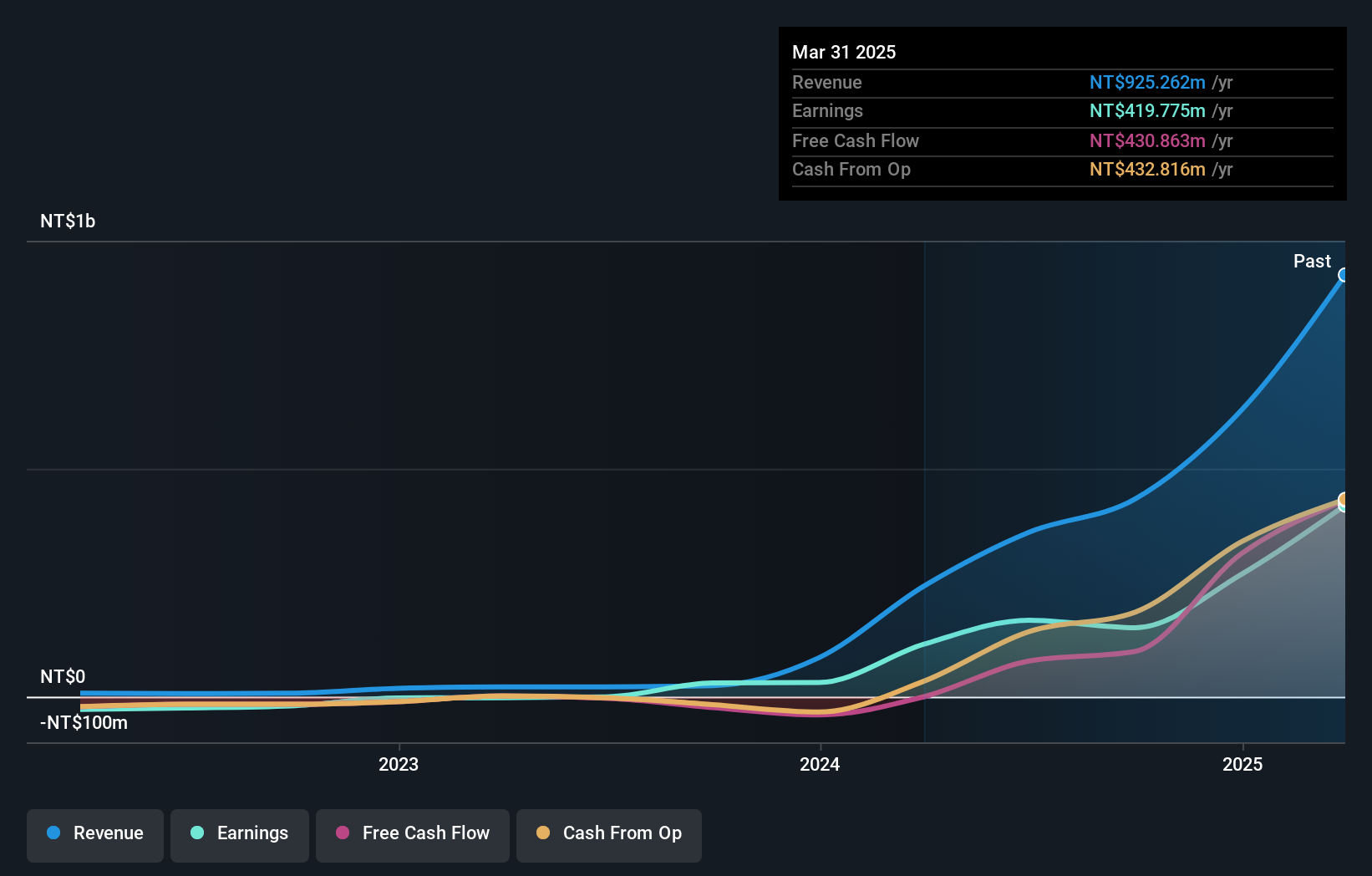

Myson Century (TPEX:5314)

Simply Wall St Value Rating: ★★★★★★

Overview: Myson Century, Inc. is involved in the research, development, manufacturing, and sale of integrated circuit system products across Taiwan, Mainland China, Europe, the United States, and other international markets with a market capitalization of NT$8.63 billion.

Operations: Myson Century generates revenue primarily from its subsidiary, Zavio Inc., contributing NT$127.78 million, with a segment adjustment of NT$305.82 million. The company's financial performance is influenced by these revenue streams and adjustments.

Myson Century, a nimble player in the semiconductor space, has demonstrated significant earnings growth of 405.1% over the past year, outpacing the industry's 5.9%. Despite its high volatility recently, it trades at a compelling 15.2% below fair value estimates. The company is debt-free with robust non-cash earnings quality and positive free cash flow. Recent reports show third-quarter sales skyrocketed to TWD 77.96 million from TWD 5.07 million last year, though net income dipped to TWD 12.77 million from TWD 29.21 million due to lower profit margins at 34.9%, down from previous levels.

- Take a closer look at Myson Century's potential here in our health report.

Understand Myson Century's track record by examining our Past report.

G-Tekt (TSE:5970)

Simply Wall St Value Rating: ★★★★★★

Overview: G-Tekt Corporation specializes in the manufacturing and sale of auto body components and transmission parts both in Japan and internationally, with a market capitalization of ¥72.54 billion.

Operations: G-Tekt generates revenue primarily through the sale of auto body components and transmission parts. The company operates both domestically in Japan and internationally, contributing to its market capitalization of ¥72.54 billion.

G-Tekt, a nimble player in the auto components sector, is making waves with its robust financial health. Over the past year, earnings surged by 20.7%, outpacing the industry average of 3.8%. Its debt-to-equity ratio impressively decreased from 35% to 18.7% over five years, showing prudent financial management. The company's price-to-earnings ratio stands at an attractive 6.5x compared to Japan's market average of 13.5x, indicating potential undervaluation relative to peers. With more cash than total debt and positive free cash flow, G-Tekt appears well-positioned for sustainable growth in a competitive landscape.

- Click to explore a detailed breakdown of our findings in G-Tekt's health report.

Explore historical data to track G-Tekt's performance over time in our Past section.

Next Steps

- Explore the 4625 names from our Undiscovered Gems With Strong Fundamentals screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:5314

Myson Century

Engages in the research, development, manufacturing, and sale of integrated circuit system products in Taiwan, Mainland China, Europe, the United States, and internationally.

Flawless balance sheet with proven track record.